Why Heterogeneous Agents Models?

Jes´us Fern´andez-Villaverde1

April 12, 2022

1University of Pennsylvania

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The importance of modeling economic agents as heterogeneous along various dimensions such as age, location, productivity, wealth, information, beliefs, and expectations. It explores the correlation between financial wealth and realized returns, trends in top marginal tax rates, household finance, and questions about aggregation bias. The document also highlights the implications of these models for empirical micro, labor economics, industrial organization, and international trade. The document warns that not every question requires a model with heterogeneous agents.

Typology: Summaries

1 / 21

This page cannot be seen from the preview

Don't miss anything!

Jes´us Fern´andez-Villaverde^1 April 12, 2022 (^1) University of Pennsylvania

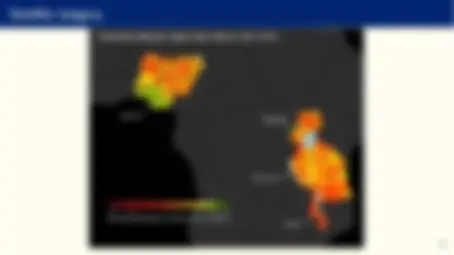

from Kuhn et al. (2018)historical data. The observed long-run trends are clearly statistically significant. America is considerably more unequal today than it was in the 1970s, with respect to both income and wealth. Figure 5: Gini coefficients with confidence bands

.

.

.

.

.

.

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

90% confidence intervals Gini coefficient

(a) Income

.

.

.

.

.

.

.

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

90% confidence intervals Gini coefficient

(b) Wealth

Notes: Gini coefficient of income (panel (a)) and wealth (panel (b)) with 90% confidence bands. Confidence bands are shown as gray areas, and point estimates are connected by lines. Confidence bands are boot- strapped using 999 different replicate weights constructed from a geographically stratified sample of the final dataset. 3

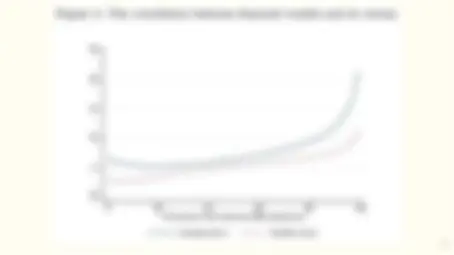

-.

0

.

.

.

.

0 20 40 60 80 100 Percentile of the financial wealth distribution Average return Median return

0

10

20

30

40

50

60

70

80

90

100

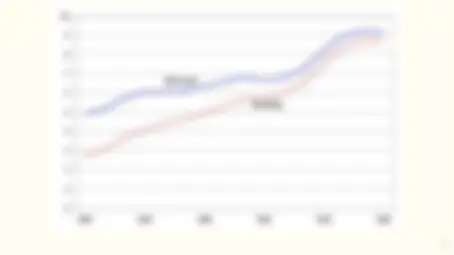

110

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004

T ot al^ De b t

M or tgage

C on s u m er R (^) e volvin g

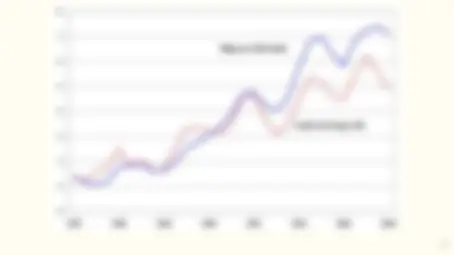

0

1

2

3

4

5

6

7

8

9

10

1983 1986 1989 1992 1995 1998

Un s e cu r e d

R evolvin g