Optimal policies with heterogeneous agents

Jes´us Fern´andez-Villaverde1and Galo Nu˜no2

October 15, 2021

1University of Pennsylvania

2Banco de Espa˜na

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Optimal policies with heterogeneous agents and their impact on infinite dimensional control, infinite dimensional optimization, constrained optimization, and constrained-efficient allocation. It also provides an example of the Aiyagari model with finite lifetimes and its solution using the first-best method. The document concludes with an application of optimal monetary policy with heterogeneous agents. It cites related literature on constrained-efficient problems in discrete-time models, optimal control problems in continuous time, and mean field control.

Typology: Exercises

1 / 60

This page cannot be seen from the preview

Don't miss anything!

Jes´us Fern´andez-Villaverde^1 and Galo Nu˜no^2 October 15, 2021 (^1) University of Pennsylvania

(^2) Banco de Espa˜na

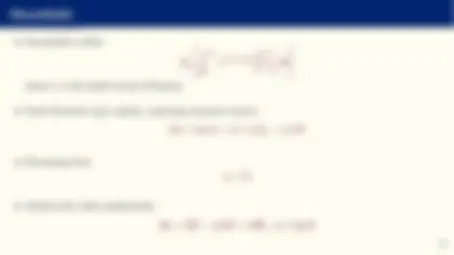

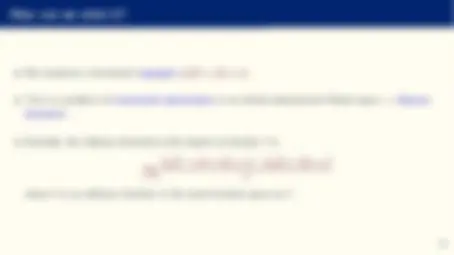

δJ (g ; h) = lim α→ 0

J (g + αh) − J (g ) α exists, it is called the Gˆateaux derivative of J at g in the direction h.

lim ‖h‖L (^2) (Φ)→ 0

|J (g + h) − J (g ) − δJ (g ; h)| ‖h‖L (^2) (Φ)

then, J is said to be Fr´echet differentiable at g and δJ (g ; h) is theFr´echet differential of J at g with increment h.

L(g ) = J(g ) + 〈λ, H(g )〉Φ

is stationary in g , i.e., δL (g ; h) = 0.

0

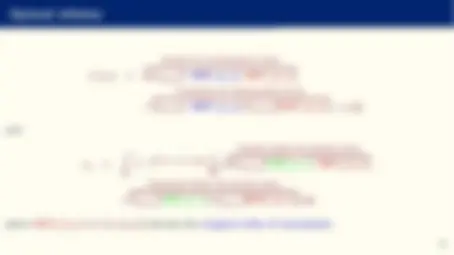

e−(ρ+η)t^ c t^1 −χ 1 − χ dt

where η is the death arrival (Poisson).

∂g ∂t

∂a (s (a, z, wt , rt , c) g )

−

∂z (θ(ˆz^ −^ z)g^ ) +

∂z^2

σ^2 g

−ηg + ηδa 0 ,z 0 ,

where −ηgt (a, z) is the outflow of agents due to death and ηδa 0 ,z 0 = ηδ (a) δ (z − z ¯ ) is the inflow of newborn agents with zero assets and productivity z ¯

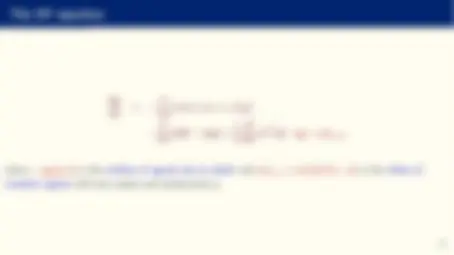

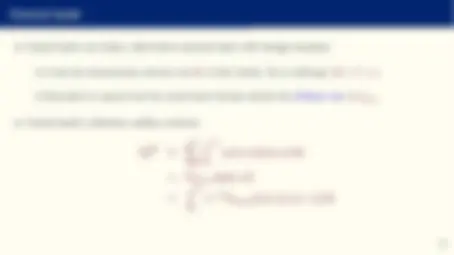

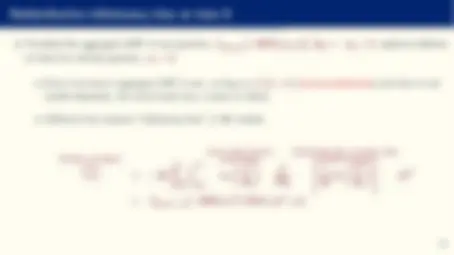

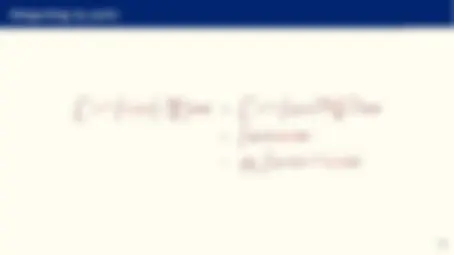

J (g (0, ·)) = max c(·)∈C(t,a,z)

0

e−ρt

∫ ∫ (^) ¯z

¯^ z

u (c) gt (a, z) dadzdt

subject to the law of motion of the aggregate density, to the factor prices and to the market clearing condition.

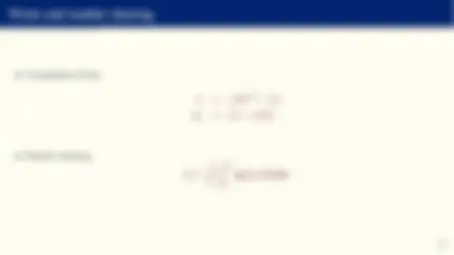

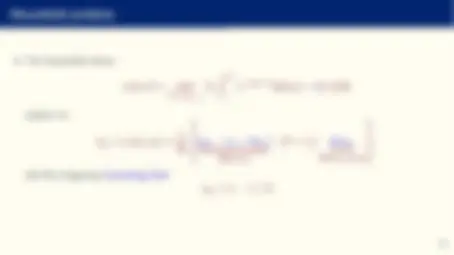

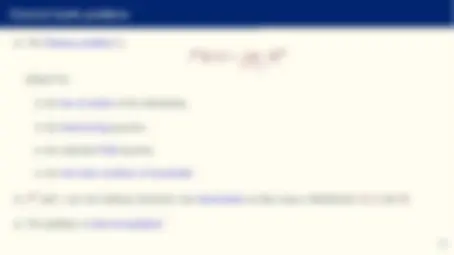

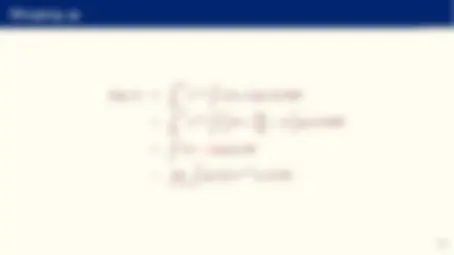

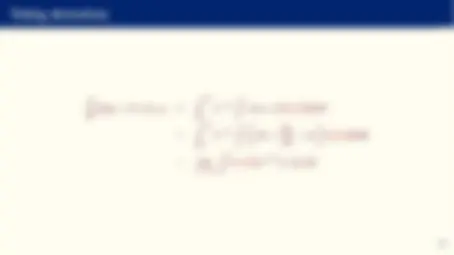

Lce (g , τ, c, j, λ) =

0

e−ρt

u (ct (a, z)) gt (a, z) dadzdt

0

e−ρt

∫ ∫ (^) z¯

¯^ z

jt (a, z)

− ∂g ∂t

dadzdt

0

e−ρt^ λt

−kt +

0

∫ (^) ¯z

¯^ z

agt (a, z)dadz

dt

dat = (wt zt + (rt + η) at − ct + τt ) dt,

where τt are transfers across agents.

¯^ z

τt (a, z)gt (a, z)dzda = 0

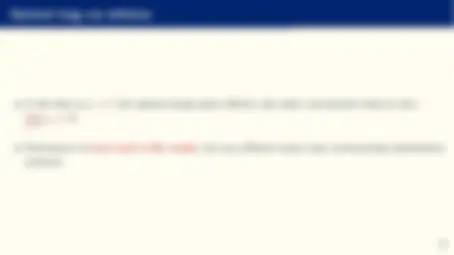

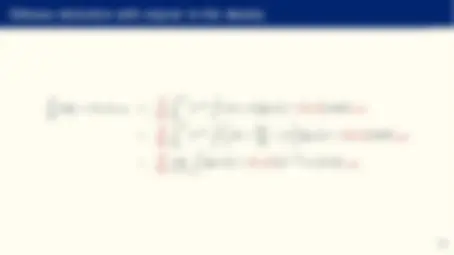

Lfb (g , τ, c, j, λ) =

0

e−ρt

u (ct (a, z)) gt (a, z) dadzdt

0

e−ρt

∫ ∫ (^) ¯z

¯^ z

jt (a, z)

− ∂g ∂t

dadzdt

0

e−ρt^ λt

−kt +

0

∫ (^) z¯

¯^ z

agt (a, z)dadz

dt

0

e−ρt^ ϕt

0

∫ (^) ¯z

¯^ z

τt (a, z)gt (a, z)dadz

dt