Download Activity-Based Costing: Understanding the Steps and Benefits and more Schemes and Mind Maps Business in PDF only on Docsity!

IMPLEMENTING AN ACTIVITY-BASED COSTING MODEL

by

HOWARD COHEN

Submitted in partial fulfilment of the requirements for the degree of Masters in Cost and Management Accounting at Nelson Mandela Metropolitan University

Date of Submission: December 2004

Promoter: Dr S Krause

View metadata, citation and similar papers at core.ac.uk provided by South East Academic Libraries System (SEALS) brought to you by CORE

i DECLARATION

This work has not been previously accepted in substance for any degree and is not being concurrently submitted in candidature for any degree.

Signed: __________________________

Date: __________________________

STATEMENT 1

This dissertation is being submitted in partial fulfilment of the requirements for the degree of Masters in Cost and Management Accounting.

Signed: __________________________

Date: __________________________

STATEMENT 2

The dissertation is the result of my own independent work/investigation, except where otherwise stated. Other sources are acknowledged by giving explicit references. A bibliography is appended.

Signed: __________________________

Date: __________________________

iii ACKNOWLEDGEMENTS

Grateful thanks are extended to all those individuals and organisations that contributed to the successful completion of this study. In particular, the assistance of the following are acknowledged:

I would like to direct my sincere gratitude to Dr S Krause, my promoter and mentor, for his valuable and patient assistance, advice and encouragement – without which this master’s thesis would never have seen the light of day.

The staff of the Management Unit at the Port Elizabeth Technikon who were at all times helpful.

The respondents of the study who made the effort to complete the questionnaires as well as those who sacrificed their time in order for me to interview them so as to gain valuable knowledge that assisted with my research.

My wife, Gail, and daughter, Romy, who sacrificed a great deal, thus enabling me to successfully complete my studies. Without their patience and support I would not have been able to achieve this.

Renée van der Merwe for her language editing and Sharon van Eeden for editing and formatting the thesis.

iv ABSTRACT

Activity-based costing (ABC) is a forward-looking product costing method. Unlike traditional volume-based approaches, which are historically oriented, ABC concepts guide managers in seeking the best strategies to pursue in the future. This product costing method can be a valuable tool in planning and managing costs not only in the manufacturing area, but also in all aspects of business operations, from product design to distribution. Although its main advantage is its ability to provide more realistic product cost information for financial reporting purposes, use of ABC can lead to a better understanding of the strategic linkages existing between the various cost areas in the organisation. It enables managers to have a holistic view of cost management.

ABC was developed to better understand, manage and control the overheads. The brief fundamental of ABC is: Products consume activities, activities consume resources, and resources consume costs. Based upon this fundamental principle, ABC can trace the cost from resources to activities that are consumed by product manufacturing processes as well as from activities to products. ABC investigates the transactions that trigger cost instead of concentrating solely on measures of physical volume or a certain amount of labour hours. Compared to the traditional costing systems, ABC can not only answer how much product cost is but also tell executives the factors triggering costs and the way to manage costs. ABC helps managers make better decisions about product design, pricing, marketing, and mix and encourages continual improvement.

Unlike the traditional method, instead of using the single pre-determined overhead rate to absorb the indirect cost to products, ABC uses actual incurred cost to

vi TABLE OF CONTENTS Page

DECLARATION (i)

STATEMENT 1 (i)

STATEMENT 2 (i)

STATEMENT 3 (ii)

ACKNOWLEDGEMENTS (iii)

ABSTRACT (iv)

TABLE OF CONTENTS (vi)

LIST OF TABLES (xiv)

LIST OF FIGURES (xv)

LIST OF FORMULAS (xvi)

CHAPTER 1: INTRODUCTION TO THE STUDY

1.1 INTRODUCTION AND BACKGROUND TO THE PROBLEM 1

1.2 PROBLEM STATEMENT 10 1.2.1 Sub-problems 10

1.3 DEFINITION OF KEY CONCEPTS 10

vii

ix

xii

5.3 GENERAL PROCEDURES 105

5.4 RESULTS OF THE QUESTIONNAIRE 106

5.5 ANALYSIS OF THE RESULTS 107

5.6 SUMMARY 108

CHAPTER 6: FINAL SUMMARY, CONCLUSIONS AND RECOMMENDATIONS FOR FURTHER RESEARCH

6.1 INTRODUCTION 109

6.2 BACKGROUND AND OBJECTIVES OF THE STUDY 109

6.3 IS PRODUCT COSTING MORE ACCURATE THAN TRADITIONAL WITH ACTIVITY-BASED COSTING AS OPPOSED TO TRADITIONAL COSTING METHODS? 111

6.4 IDENTIFYING THE COST OF THE ACTIVITIES AND ESTABLISHING A COST POOL FOR EACH ACTIVITY 112

6.5 DEVELOPING A MODEL TO OVERCOME THE DIFFICULTIES WHEN IMPLEMENTING AN ACTIVITY-BASED COSTING SYSTEM 112

xiii

xv

xvi

- 1.4 ABBREVIATIONS

- 1.5 THE NEED FOR RESEARCH

- 1.6 DELIMITATION OF THE RESEARCH

- 1.6.1 Demarcation of organisations to be researched

- 1.6.2 Geographic demarcation

- 1.7 ASSUMPTIONS

- 1.8 SIGNIFICANCE OF THE RESEARCH

- 1.9 OUTLINE OF THE STUDY

- 2.1 EVOLUTION OF ACTIVITY- BASED COSTING CHAPTER 2: UNDERSTANDING ABC

- 2.2 TRADITIONAL PRODUCT COSTING

- 2.3 ACTIVITY- BASED COSTING PRINCIPLES

- 2.4 THE MAJOR ADVANTAGES OF ABC

- 2.5 WHY ABC IS NEEDED

- 2.6 HOW ABC WORKS viii

- 2.7 COMPONENTS OF ACTIVITY-BASED COSTING

- 2.8 IDENTIFYING COST DRIVERS

- 2.8.1 Categories of cost drivers

- 2.9 ACTIVITY HIERARCHY

- 2.10 SIMPLE ACTIVITY COST MODELS

- 2.11 STEPS INVOLVED IN ACTIVITY-BASED COSTING DESIGN

- 2.11.1 Aggregating the different activities

- 2.11.2 Report the cost of activities

- 2.11.3 Identify activity centres

- 2.11.4 Select first-stage cost drivers

- 2.11.5 Select second-stage cost drivers

- 2.12 ACTIVITY CENTRES

- 2.13 DETERMINING ACTIVITY COSTS

- 2.13.1 ANALYSE ACTIVITIES

- 2.13.2 GATHER COSTS

- 2.13.3 TRACE COSTS TO ACTIVITIES

- 2.13.4 ESTABLISH OUTPUT MEASURES

- 2.13.5 ANALYSE COSTS

- BASED COSTING 2.14 AN EXAMPLE OF ABSORPTION-BASED COSTING VS ACTIVITY-

- 2.15 WHY ABC IS IMPORTANT

- 2.16 LIMITATIONS OF ABC

- 2.17 SUMMARY

- 3.1 THE RATIONALE TO IMPLEMENT ABC CHAPTER 3: IMPLEMENTING AN ACTIVITY- BASED COSTING SYSTEM

- 3.2 IMPLEMENTATION

- 3.2.1 Identify and analyse activities performed

- these activities 3.2.2 Trace the usage of organisational resources to

- 3.2.3 Define the outputs produced

- 3.2.4 Link the activity costs to the outputs

- 3.3 IMPROVED FINANCIAL PERFORMANCE

- 3.4 EFFECTIVE SPONSORSHIP

- 3.5 COSMETIC CHANGES OR CULTURAL EVOLUTION

- 3.6 PRACTICAL DETERMINATIONS OF THE ABC MODEL x

- 3.7 IMPLEMENTATION STEPS

- 3.7.1 Department interviews

- 3.7.2 Cost accounting

- 3.7.3 Time tracking system

- 3.7.4 Activity costing

- 3.7.5 Volumetrics

- 3.7.6 ABC model system

- 3.7.7 Ensuring consistency with other ABC models

- 3.7.8 Costing transactions

- 3.8 ACTIVITY- BASED COSTING SOFTWARE

- 3.9 DECISION ANALYTICS

- 3.9.1 The S-curve

- 3.9.2 Customer segmentation analysis

- 3.9.3 Insource versus outsource decisions

- 3.10 CARE AND MAINTENANCE

- 3.11 SUMMARY

- 4.1 INTRODUCTION CHAPTER 4: RESEARCH METHODOLOGY AND PRESENTATION OF RESULTS

- 4.2 WHAT IS RESEARCH DESIGN? xi

- 4.2.1 The concept of research

- 4.2.2 The concept of design

- 4.3 RESEARCH APPROACH

- 4.4 QUANTITATIVE RESEARCH

- 4.5 QUALITATIVE RESEARCH

- 4.6 TRIANGULATION

- 4.7 CHOOSING THE MOST APPROPRIATE RESEARCH METHOD

- 4.8 RESEARCH GOALS AND STRATEGIES

- 4.8.1 Research goals

- 4.8.2 Research strategy

- 4.9 SUMMARY

- 5.1 INTRODUCTION CHAPTER 5: QUESTIONNAIRE DESIGN AND PRESENTATION OF RESULTS

- 5.2 QUESTIONNAIRE DESIGN AND STRUCTURE

- 6.6 STEPS INVOLVED IN ACTIVITY-BASED COSTING

- 6.7 BENEFITS OF ACTIVITY-BASED COSTING

- 6.8 CONCLUSIONS

- 6.9 RECOMMENDATIONS FOR FURTHER RESEARCH

- REFERENCES

- ANNEXURE A: QUESTIONNAIRE

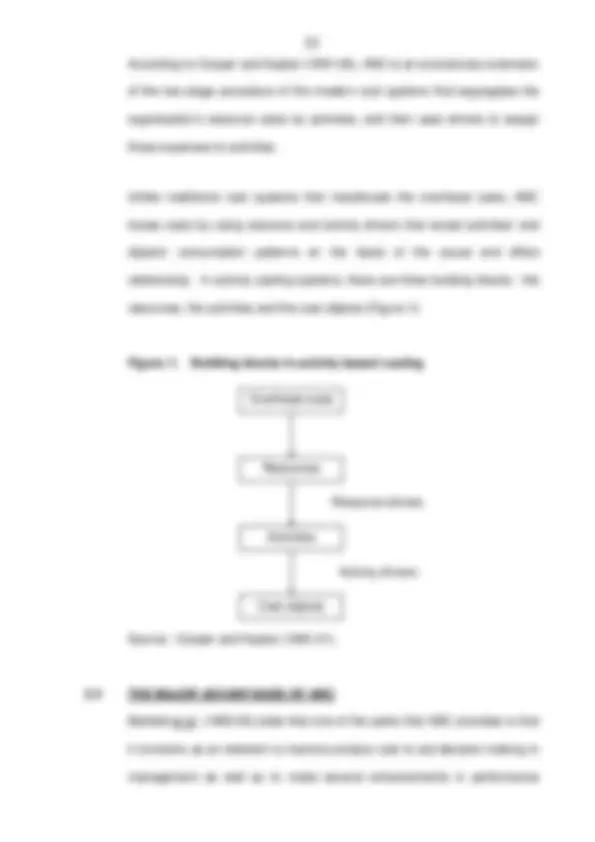

- Figure 1: Building blocks in activity based costing LIST OF FIGURES

- World Figure 2: The proportion of material, direct labour and overheads in today’s

- Figure 3: Where traditional cost systems focus their attention

- Figure 4: An overview of ABC mechanics

- Figure 5: The hierarchy of factory operating expenses

- Figure 6: ABC Model

- Figure 7: Activity-based costing philosophy

- Figure 8: Multifaceted view of business

- Figure 9: Framework for ABC implementation

- Figure 10: Business views relevant in equity brokerage business

- Figure 11: Research design

- Figure 12: Interaction between quantitative and qualitative research

- 1 Total unit direct cost LIST OF FORMULAS

- 2 Predetermined overheads rate

- 3 Total cost of product

- 4 ABC cost change

- 5 Direct labour

- 6 Total number of hours

- 7 Direct labour or machine hour

- 8 Overhead costs per product

costs to be incurred. Organisations are using ABC to support major decisions on product lines, market segments and customer relationships, as well as to simulate the impact of process improvements. Organisations involved in Total Quality Management (TQM) processes are using both the financial and non-financial information of ABC as a measurement system (AICPA, 2004:1).

In the 1980’s a number of companies such as Boeing, TRW, Texas Instruments and Corning became dissatisfied with how overheads were being allocated. For the most part they were still using direct labour hours as the basis for making allocations to products. This was despite the fact that there were very few direct labour hours being worked and that the overheads being allocated were many times greater than the costs of labour. Rather than simply moving to a different basis of allocation, they developed a new and more complex method. This has come to be known as ABC (Anderson & Nix, 1994:109).

According to Anderson and Nix (1994:109), overhead costs are incurred for many different reasons. ABC identifies the cost of all the activities being carried out. It then finds a suitable base for allocating those costs to products. ABC is a technique to more accurately assign the indirect and direct resources of an organisation to the activities performed based on consumption. ABC uses a two-stage cost assignment approach. In the first stage, resource costs are assigned to activities based on the amount of resources consumed in performing the activity. An activity cost would equal the sum of all the resources consumed in performing the activity. In the

second stage, activity costs are traced to the products, services, or customers based on how frequently the activity is performed in support of these cost objects (La Londe & Ginter, 2000:1).

According to AICPA (2004:2), the basic distinction between traditional cost accounting and ABC is as follows: traditional cost accounting techniques allocate costs to products based on attributes of a single unit. Typical attributes include the number of direct labour hours required to manufacture a unit, purchase cost of merchandise resold or the number of days occupied. Allocations, therefore, vary directly according to the volume of units produced, the cost of merchandise sold or the days occupied by the customer. In contrast, ABC systems focus on activities required to produce each product or provide each service based on each product or service’s consumption of the activities. Using ABC, overhead costs are traced to products and services by identifying the resources, activities and their costs and quantities to produce output. A unit or output (a driver) is used to calculate the cost of each activity consumed during any given period of time. An ABC system can be viewed in two different ways. The cost assignment view provides information about resources, activities and cost objects. The process view provides operational (often non-financial) information about cost drivers, activities and performance.

Most ABC applications have focused initially on the manufacturing environment owing to the need to accurately determine product costs. However, many service industries, including logistics, have also begun to implement ABC with most cases being reported only within the last five