Download Investment Lecture Note and more Lecture notes Finance in PDF only on Docsity!

Investments (EF5052) Investments (EF5052) |^ Dr.^ Ferenc^ Horvath

Week^1 Dr.^ Ferenc^ Horvath September^ 8,^2018

Contents • Risk and Return Bodie, Kane, and Marcus, Chapter 5 • Highly suggested exercises: Bodie, Kane, and Marcus, Chapter 5, Problems5. a‐c, 6. a‐b, 7, 10, 11, 12, 13, 15. (Solutions areavailable on Canvas.) Bodie, Kane, and Marcus, Chapter 5, CFA Problems1‐7. (Solutions are available on Canvas.)Investments (EF5052) | Dr. Ferenc Horvath

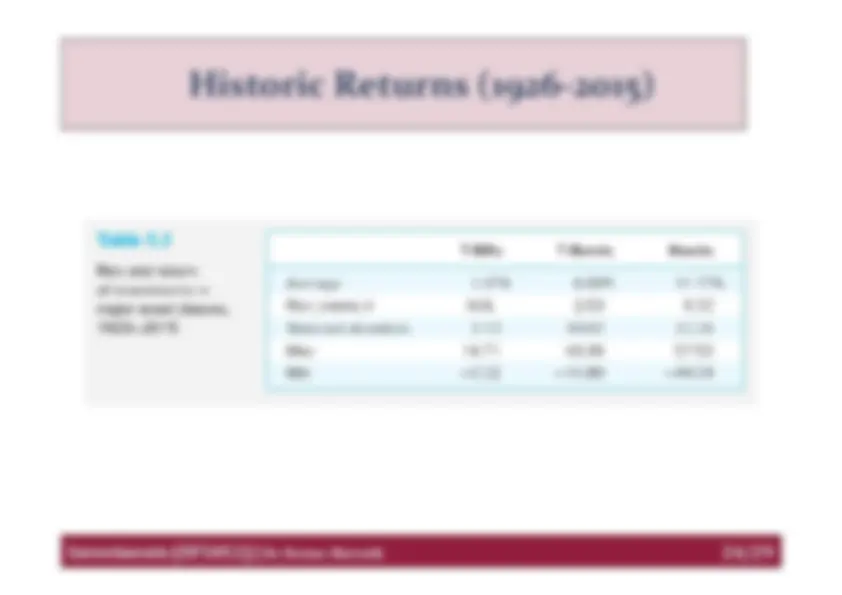

Nominal^ rates and^ •^ $1 in T‐bills from 1926–2015 grew to $20.25 but witha real value of only $1.55.Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

Inflation,^1926 ‐^2015

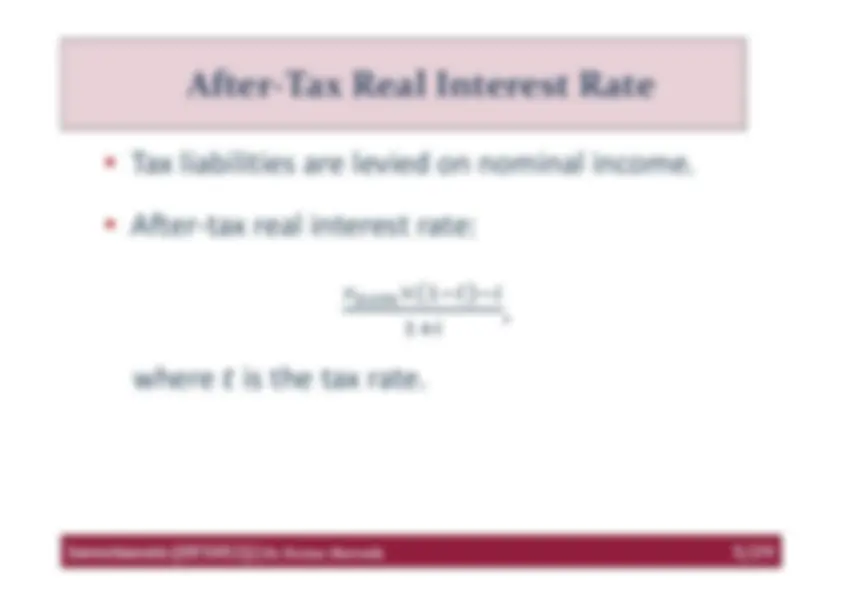

-^ Tax liabilities are levied on nominal income. •^ After‐tax real interest rate:^ Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

After‐Tax Real^ Interest^ Rate ൈ ଵି௧ି ^ , ଵା^ where^ is the tax rate.

-^ Example:^ A one‐year bank deposit pays 8% interest. The inflation will be 5%over the next one‐year period. The tax on interest is 15%.What is the before‐tax real interest rate? What is the after‐tax realinterest rate?^ Answer:^ The before‐tax real interest rate is Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

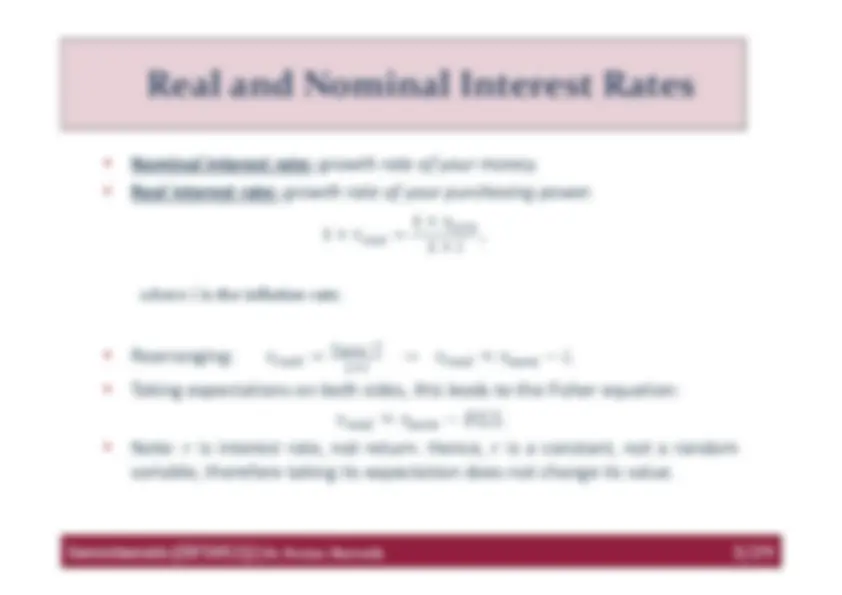

Real^ and Nominal^ Interest^ Rates .ଷ^ ൌ 0.0286.ଵ.ହ^ (The before‐tax real interest rate is approximately^ 0.08 െ 0.05 ൌ 0.03 ). .଼ൈ^ ଵି.ଵହି .ହ The after‐tax real interest rate is^ ൌ 0.0171. ଵା.ହ^

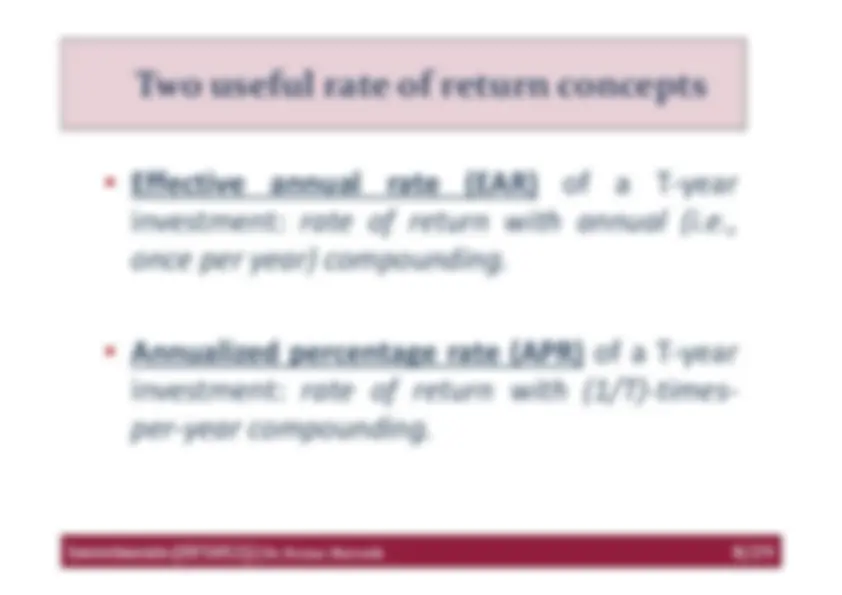

-^ Effective^ annual^ rate Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

(EAR)^ of^ a^ T‐yearinvestment: rate of return with annual (i.e.,once per year) compounding.

-^ Annualized percentage rate (APR)

of a T‐year

Two^ useful^ rate^ of^ return investment:^ rate of return with (1/T)‐times‐per‐year compounding.

concepts

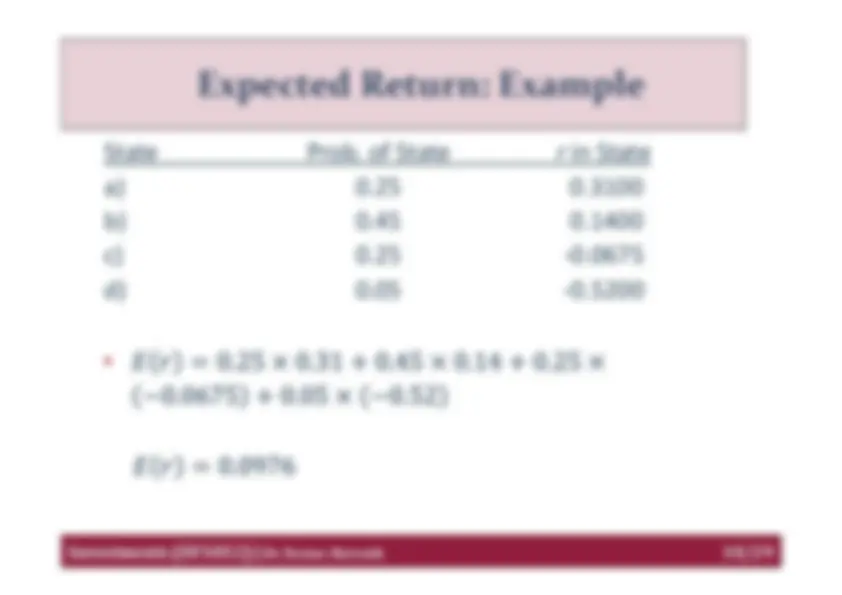

State^ Prob. of State Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

r^ in State

a)^ 0.^

b)^ 0.^

c)^ 0.^

d)^ 0.^

Expected Return: •

Example

Variance^ and^ Standard • Variance (VAR): • Standard Deviation (STD):Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

Deviationof Return^2 ^2 S T D

2 p^ s^ r^ s^ s

E^ r

^ ^ ^

Time^ Series^ Analysis of • True means and variances are unobservable. • Thus, they must be estimated.Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

Past^ Returns

-^ Estimated expected return: Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

-^ Note: the geometric mean^ ଵ^ ଶ^

leads to a^ biased^ estimated expected return! • Thus, do^ not^ use geometric mean for estimation! • The arithmetic^ mean^ (see^ above)

is^ an^ unbiased

Estimating^ the^ Expected estimator.

Return

Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

where^ •^ is^ the^ excess^ return^

(i.e.,^ the^ difference

Sharpe^ Ratio between the investment’s return and the risk‐freereturn), • and is the standard deviation of the excess return. • The Sharpe ratio tells us how much excess returnwe can expect per volatility of excess return.

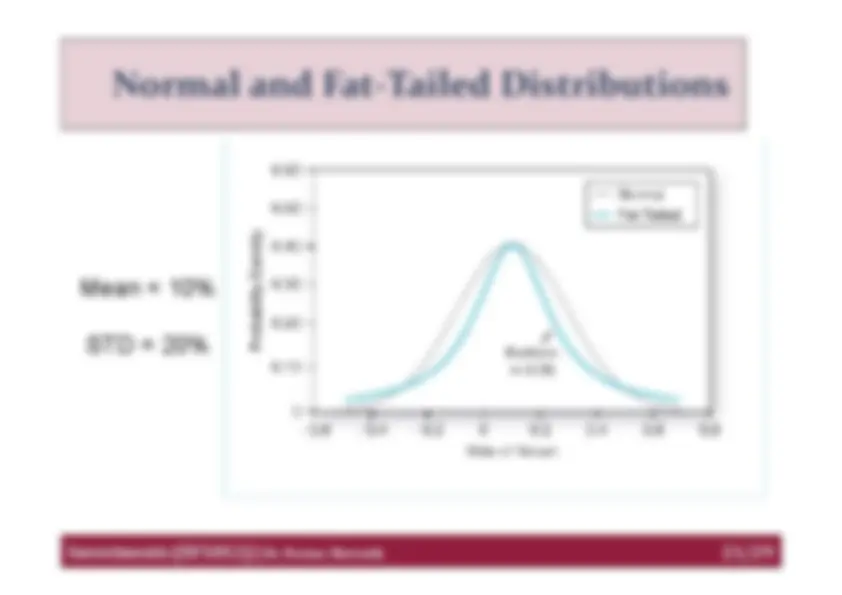

The^ Normal Investments (EF5052) |^ Dr.^ Ferenc^ Horvath

Distribution Mean = 10%, SD = 20%

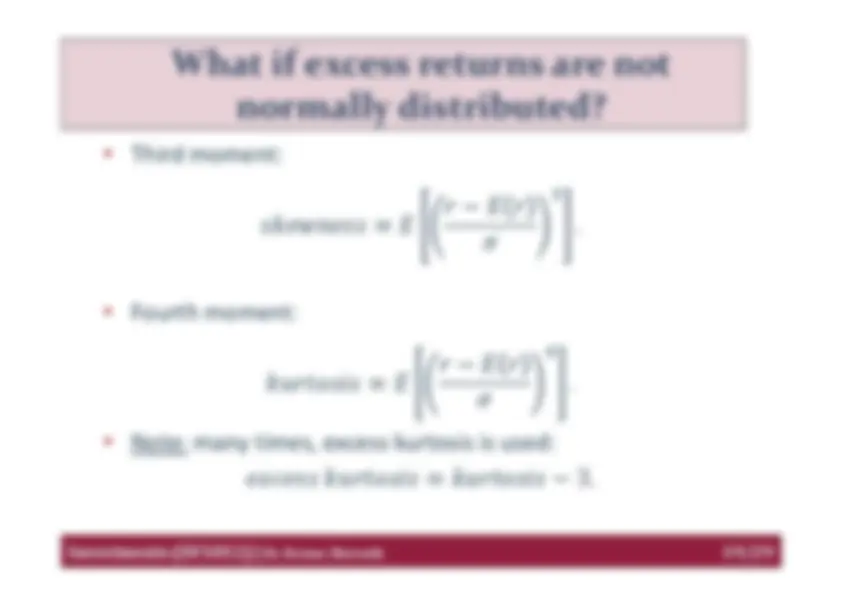

-^ Third moment:^ 𝑠𝑘𝑒𝑤𝑛𝑒𝑠𝑠 ൌ 𝐸 Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

What^ if^ excess^ returns^ are^ not^ normally^ distributed? ଷ𝑟 െ 𝐸 𝑟^. 𝜎 • Fourth moment:ସ𝑟 െ 𝐸 𝑟^ 𝑘𝑢𝑟𝑡𝑜𝑠𝑖𝑠 ൌ 𝐸^. 𝜎 • Note: many times, excess kurtosis is used:^ 𝑒𝑥𝑐𝑒𝑠𝑠 𝑘𝑢𝑟𝑡𝑜𝑠𝑖𝑠 ൌ 𝑘𝑢𝑟𝑡𝑜𝑠𝑖𝑠 െ 3.

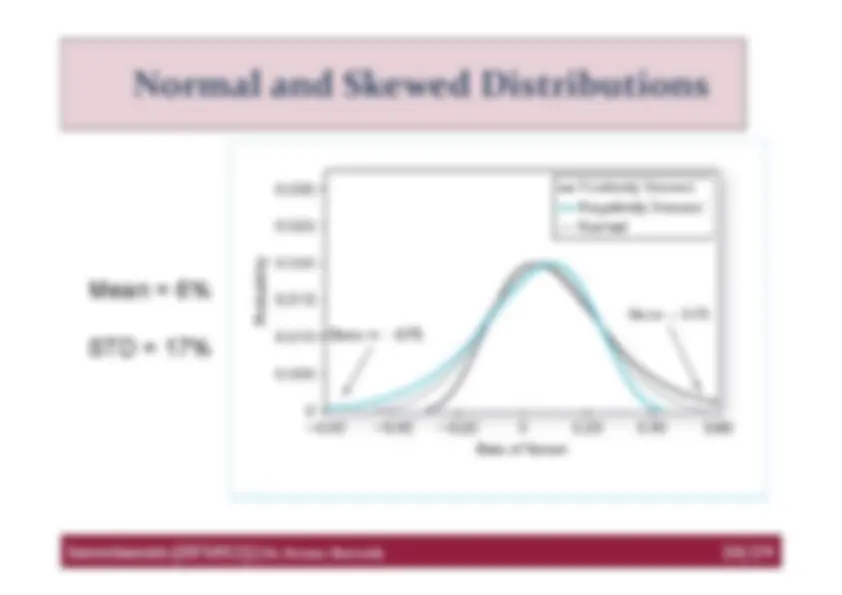

Normal^ and^ Skewed Investments^ (EF5052) |^ Dr.^ Ferenc^ Horvath

Distributions

Mean = 6%STD = 17%