Contemporary Financial

Management

Leasing

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Students of Computer Science, study E-Commerce as an auxiliary subject. these are the key points discussed in these Lecture Slides of E-Commerce : Leasing, Contemporary Financial, Management, Borrow, Maximize Shareholder, Costs, Benefits, Financing, The Lessor, The Lessee

Typology: Slides

1 / 15

This page cannot be seen from the preview

Don't miss anything!

Leasing

This chapter explores the reasons a firm mightchoose to lease rather than borrow and buysome of their assets.

It examines the type of analysis that should gointo a lease versus borrow-and-purchasedecision to maximize shareholder wealth. - It examines the costs and benefits to leasingcompanies offering this type of financing.

Leases are most effective when done betweena high marginal tax lessor and a low marginaltax lessee.

The lessee passes to the lessor tax deductions thatthe lessee cannot use. - In return, the lessor passes some of the benefitback to the lessee in the form of lower leasepayments.

Leases

An alternative to term financing - A mechanism to transfer tax benefits - Lessee - Obtains use of an asset - For a specific period of time - In return for a series of payments to the lessor

Financial Lease - Sometimes called a capital lease - Initial term usually equal to the expected economiclife of the asset - Not cancelable by the lessee - Lessee responsible for maintenance, insurance andproperty taxes - May originate as a: - Direct lease - Sale and leaseback

The lessee acquires the use of an asset it doesnot own.

The lessor may be the manufacturer or afinancial institution. - If the lessor is a financial institution (F.I.), thelessee provides all specifications to the F.I.,which then purchases the asset and leases itto the lessee.

Leveraged Lease

Three-party lease involving a lessee, a lessor and afinancial institution (F.I.) or lender. - The lessor and the F.I. jointly provide the fundsrequired to purchase the asset. - All other terms are similar to a financial lease.

Flexible – fewer restrictive covenants

Convenient - Source of financing to the risky firm (sinceownership remains with the lessor) - May avoid some risk of obsolescence - Smoother earnings and earnings per share - 100% financing (but lease payments usually occur at the beginning of the period)

Annual lease payments are tax deductible forthe lessee if the CRA (Canada RevenueAgency) agrees that the contract is truly alease and not just an installment loan called alease.

Reasons why CRA might disallow a lease - Lessee has the right to acquire the asset at lessthan fair market value - Lessee required to buy the asset at the end ofthe lease - Lessee automatically obtains ownership at the

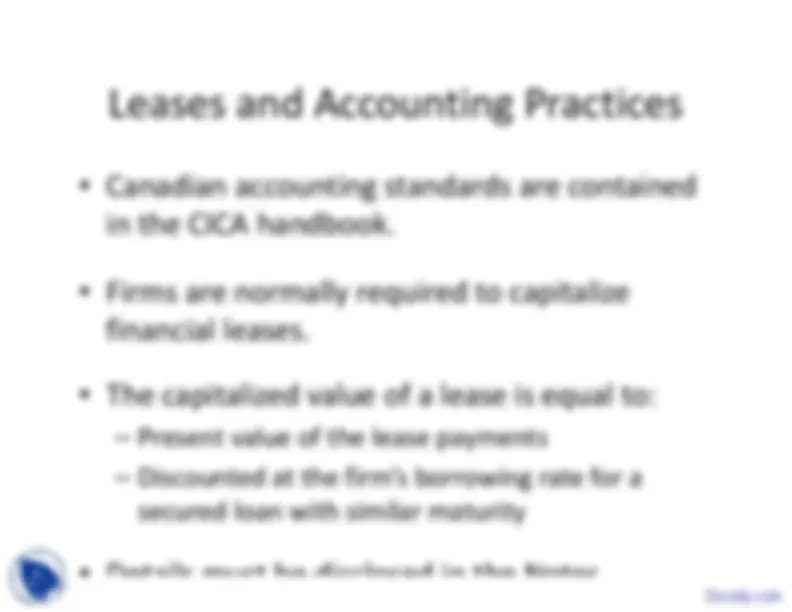

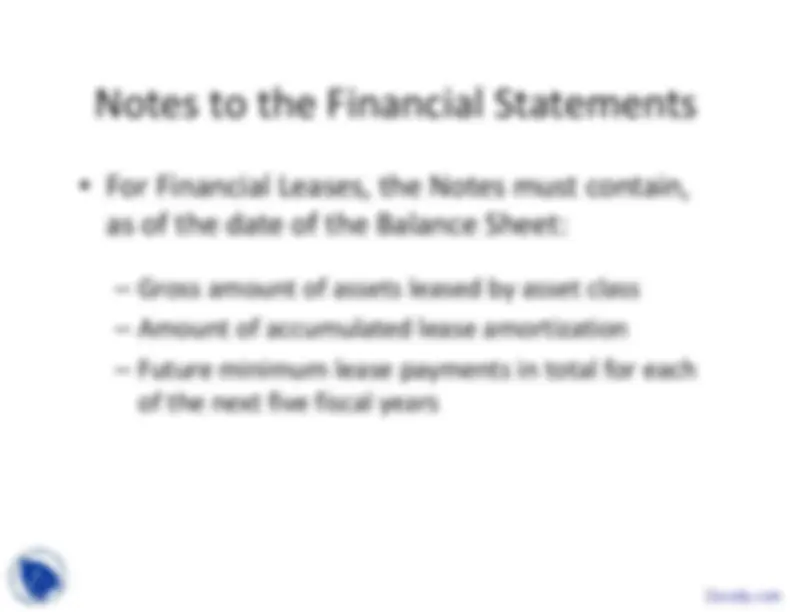

Canadian accounting standards are containedin the CICA handbook.

Firms are normally required to capitalizefinancial leases. - The capitalized value of a lease is equal to: - Present value of the lease payments - Discounted at the firm’s borrowing rate for asecured loan with similar maturity - Details must be disclosed in the Notes.