Contemporary Financial Management

Chapter 8:

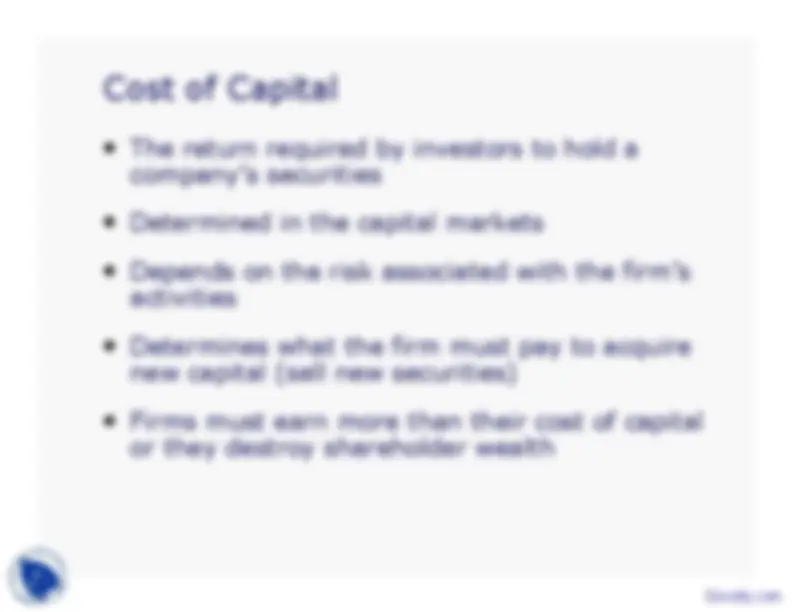

The Cost of Capital

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Students of Communication, study E-Commerce as an auxiliary subject. these are the key points discussed in these Lecture Slides of E-Commerce :Capital Structure, Weighted Average, Cost, Return Trade, Capital Markets, Risk Associated, Firm, New Securities, Shareholder Wealth, Destroy

Typology: Slides

1 / 11

This page cannot be seen from the preview

Don't miss anything!

Introduction •^

-^

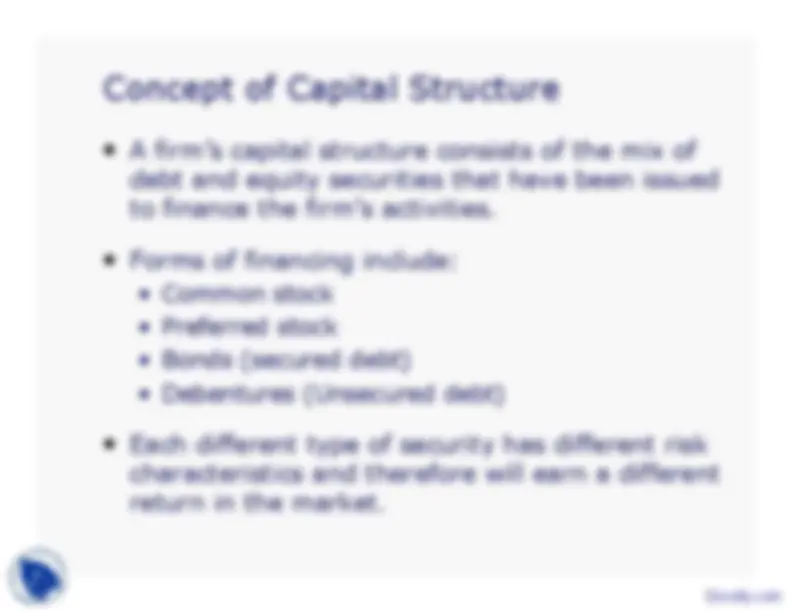

Concept of Capital Structure •^

-^

-^

Weighted Ave. Cost of Capital (WACC) •^

-^

-^

Weighted Average Cost of Capital

(^

)^

(^

) (

)^

(^

)^

(^

) (

)^

(^

)

^

^

^

^

^

=^

+^

−^

^

^

^

^

^

+^

+^

+^

+^

+^

^

^

^

^

^

^

^

^

^

^

=^

+^

−^

^

^

^

^

^

+^

+^

+^

+^

+^

^

^

^

^

^

=

f

a^

e^

d^

p

f^

f^

f

E^

D

P

k^

k^

k^

1

T^

k

E^

D

P^

E^

D

P^

E^

D

P

6

3

1

.

.

1

.

6

3

1

6

3

1

6

3

1

11.2%

Docsity.com

Required Rate of Return •^

-^

-^

i^

d

Cost of Preferreds •^

net

p

p

D^ net

k

=

P