Download Comparing Forecasting Performance of Macroeconomic Models: DSGE vs. Dynamic Factor Models and more Summaries Business Accounting in PDF only on Docsity!

MACROECONOMIC ANALYSIS AND

FORECASTING: AN EMPIRICAL

INVESTIGATION

Doctorando Carlos Cuerpo Caballero Directora Pilar Poncela Blanco Departamento de Análisis Económico: Economía Cuantitativa Facultad de Ciencias Económicas y Empresariales Universidad Autónoma de Madrid Junio 2017

AGRADECIMIENTOS

Me gustaría agradecer en primer lugar a mi directora, Pilar Poncela, que desde el principio entendió la dificultad de compaginar tesis y trabajo. Su apoyo ha sido un gran activo en todo este proceso. Su visión rigurosa y el grado de atención por el detalle son lecciones valiosas para alguien perdido en la vorágine del día a día. Su empuje en el tramo final ha supuesto un factor diferencial para llevar este proyecto a término. Mi agradecimiento también al Departamento de Análisis Económico: Economía Cuantitativa de la Facultad de Ciencias Económicas y Empresariales de la Universidad Autónoma de Madrid, y en especial a su directora, Aránzazu de Juan, porque desde el principio hasta el final todo han sido facilidades y ayuda, tanto en el ámbito académico como en el administrativo. Muchas personas han contribuido a hacer posible este proyecto, en especial compañeros de trabajo y amigos, como Luis González Calbet, Enrique Quilis, Ángel Cuevas, Jorge Prieto y Fernando Mateos, cuya colaboración y apoyo han hecho posible que no haya arrojado la toalla por el camino. Mi agradecimiento más sincero también a Luis Regino Murillo y Juan Vega, que supieron incentivarme y fomentar mis ganas por formarme en mi etapa en la Universidad de Extremadura y cuya influencia ha permanecido muy presente desde entonces. En el plano familiar, toda la gratitud del mundo a mis padres, Gregorio y Manoli. Su esfuerzo y sacrificios para que mi hermano y yo siempre dispusiéramos de los mejores medios y oportunidades han sido las llaves que nos han permitido abrir todas las puertas que nos hemos encontrado por el camino. Gracias a mi hermano, por ser un ejemplo a seguir, un referente, un apoyo y mi mejor amigo. Gracias a mi abuelo, por tener la suficiente visión como para mejorar la vida de todos los que hemos venido después. A mi tío, por creer en mí y estar siempre presente. A mi abuela, a mi tía Gloria y a mis primos Pablo y Enrique, por las risas, los abrazos y el apoyo incondicional. Por último, gracias a ti, Ana, por entender y apoyar todos mis proyectos, aun a costa de muchos sacrificios. Por saber animarme y evitar que todo el esfuerzo hubiera sido en vano. Gracias por traer a Cristina a nuestras vidas; “la loca” es la que le da sentido a todo.

RESUMEN

Esta tesis analiza temas de especial relevancia para los responsables de política económica a raíz de la crisis financiera. En un primer paso, el enfoque se centra en la estimación de la holgura o brecha de producción de la economía en función de la acumulación de distintos desequilibrios macroeconómicos. El análisis presenta un enfoque novedoso centrado en la especificación del modelo y no en la selección previa del método de estimación. Los métodos multivariantes, junto con el filtro de Kalman, se consideran una opción de modelización apta que consigue un compromiso adecuado entre criterios difíciles de conjugar a priori; ajuste estadístico, fundamentación económica y replicabilidad de los resultados. El enfoque se ilustra con una aplicación para la economía española, seleccionando el mejor modelo entre combinaciones bivariantes del Producto Interior Bruto y 52 variables de acompañamiento. En un segundo paso, esta disertación evalúa la capacidad predictiva fuera de muestra de modelos estructurales y no estructurales utilizando datos de frecuencia trimestral correspondientes a los últimos 37 años para siete agregados macroeconómicos: PIB, consumo privado, inversión privada, empleo, deflactor del PIB, salarios reales y tipo de interés nominal. La capacidad predictiva se evalúa mediante un procedimiento recursivo a través de cuatro dimensiones diferentes: una dimensión temporal (de uno a ocho trimestres), una dimensión contextual (período de crecimiento suave y fase de recesión), una dimensión específica del país (resultados para España, zona euro y Estados Unidos) y una dimensión específica del modelo (comparación de modelos estructurales de equilibrio general con los modelos de referencia tradicionales, como los Vectores autor regresivos o VAR y los VAR Bayesianos). Finalmente, el tercer paso tiene como objetivo calibrar la importancia relativa de los canales de transmisión internacional de las perturbaciones económicas. Con el fin de medir de manera óptima la fuerza relativa de las interconexiones existentes entre países, el análisis circunscribe primero la transmisión de los choques a tres canales relevantes; flujos comerciales, exposiciones bancarias y contagio a través de la percepción de los agentes (reflejada en el co-movimiento de los rendimientos de los bonos soberanos). A continuación, se obtiene el esquema de ponderación óptimo dentro de un modelo VAR Global (GVAR), minimizando el error de predicción del PIB a corto plazo del modelo. Una vez

que se calibran los pesos relativos óptimos de los canales, se utilizan conjuntamente con los flujos bilaterales para construir un indicador ponderado que refleje el potencial de efectos desbordamiento o spillover entre países. Dependiendo del país de referencia, este indicador arroja el potencial de desbordamiento interno (qué países son relativamente más importantes para una economía específica y en qué medida) así como el externo (qué países son más dependientes de la evolución de una economía seleccionada) un país.

the inward (which countries are relatively more important for a specific economy, and to what extent) as well as the outward (which countries are more dependent on the evolution of a selected economy) spillover potential for a country.

CONTENTS

RESUMEN ...................................................................................... VII

ABSTRACT....................................................................................... IX

LIST OF TABLES ........................................................................... XIII

- 1 INTRODUCTION LIST OF FIGURES XIV

- 1.1 MOTIVATION

- 1.2 IMBALANCES AND THE BUSINESS CYCLE...............................................

- 1.3 FORECASTING ALONG THE BUSINESS CYCLE..........................................

- 1.4 INTERNATIONAL TRANSMISSION OF SHOCKS

- 1.5 ORGANIZATION

- 1.6 REFERENCES

- 2 IMBALANCES AND THE BUSINESS CYCLE

- 2.1 INTRODUCTION

- 2.2 ECONOMETRIC METHODOLOGY

- 2.2.1 Univariate model

- 2.2.2 Multivariate model...............................................................

- 2.3 SELECTION CRITERIA

- 2.4 LET THE DATA SPEAK: AN APPLICATION TO SPAIN

- 2.4.1 Data set and data processing

- 2.4.2 Selection results

- 2.5 AN ESTIMATE FOR SPAIN

- 2.5.1 Robustness check: alternative combinations

- 2.6 CONCLUSION

- 2.7 REFERENCES

- 3 FORECASTING ALONG THE BUSINESS CYCLE

- 3.1 INTRODUCTION

- 3.2 METHODOLOGY

- 3.2.1 Non-Structural Models

- 3.2.2 Dynamic Factor Models

- 3.2.3 Structural Models

- 3.3 DATA AND ESTIMATION RESULTS

- 3.4 FORECASTING RESULTS

- 3.5 POST-CRISIS PERIOD: BACK TO NORMAL?

- 3.6 CONCLUDING REMARKS

- 3.7 REFERENCES

- 4 INTERNATIONAL TRANSMISSION OF SHOCKS

- 4.1 INTRODUCTION

- 4.2 GVAR THEORETICAL FRAMEWORK

- 4.2.1 Individual country models.....................................................

- 4.2.2 GVAR model

- 4.2.3 Estimating the country-specific VARX models

- 4.3 GVAR SPECIFICATION AND ESTIMATION

- 4.3.1 Data selection and properties

- 4.3.2 Testing of the individual, country-specific models

- 4.4 IMPACT OF THE CRISIS ON THE BILATERAL SYSTEMIC SPILLOVER POTENTIAL

- 4.4.1 Optimal weighting of the different transmission channels........

- 4.4.2 Bilateral Systemic Spillover (BSS) Index...............................

- 4.5 CONCLUSION

- 4.6 REFERENCES

- 5 SUMMARY AND FUTURE RESEARCH

- TABLE 1. DATA SET LIST OF TABLES

- TABLE 2. SELECTED VARIABLES ACCORDING TO CRITERIA 1 TO

- TABLE 3. US DATA, BASIC INFORMATION......................................................

- TABLE 4. EURO AREA DATA, BASIC INFORMATION

- TABLE 5. SPAIN DATA, BASIC INFORMATION

- TABLE 6. FACTOR LOADINGS

- TABLE 7: LIST OF COUNTRIES INCLUDED IN THE GVAR.....................................

- TABLE 8. ORDER SELECTION AND COINTEGRATION SPACE OF INDIVIDUAL MODELS

LIST OF FIGURES

FIGURE 1. OPTIMALITY NECESSARY REQUIREMENTS .......................................... 28

FIGURE 2. SELECTED OUTPUT GAP ESTIMATES ................................................ 42

FIGURE 3. BACKTEST, SELECTED VARIABLES .................................................. 43

FIGURE 4. OUTPUT GAP ESTIMATE AND SURROUNDING UNCERTAINTY ..................... 45

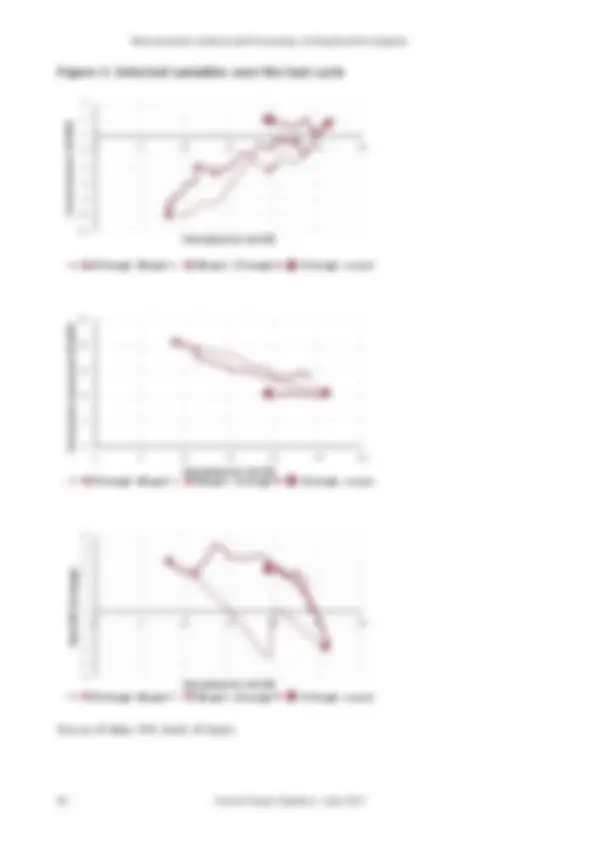

FIGURE 5. SELECTED VARIABLES OVER THE LAST CYCLE ..................................... 46

FIGURE 6. OUTPUT GAP ESTIMATES, ENHANCED MODELS ................................... 47

FIGURE 7. US SERIES ............................................................................. 66

FIGURE 8. EURO AREA SERIES ................................................................... 67

FIGURE 9. SPAIN SERIES ......................................................................... 68

FIGURE 10. DFM US IDENTIFICATION RESULTS ACCORDING TO THE CROSS-CORRELATION

MATRIX ........................................................................................ 70

FIGURE 11. US RMSE ANALYSIS, DIFFERENT FORECAST HORIZONS (1 TO 8 STEPS

AHEAD) ........................................................................................ 73

FIGURE 12. EURO AREA RMSE ANALYSIS, DIFFERENT FORECAST HORIZONS (1 TO 8 STEPS

AHEAD) ........................................................................................ 74

FIGURE 13. SPAIN RMSE ANALYSIS, DIFFERENT FORECAST HORIZONS (1 TO 8 STEPS

AHEAD) ........................................................................................ 75

FIGURE 14. RMSE GAP (%) WITH RESPECT TO THE DSGE-VAR, US (1 TO 8 STEPS

AHEAD) ........................................................................................ 77

FIGURE 15. RMSE GAP (%) WITH RESPECT TO THE DSGE-VAR, EURO AREA (1 TO 8

STEPS AHEAD) ................................................................................ 78

FIGURE 16. RMSE GAP (%) WITH RESPECT TO THE DSGE-VAR, SPAIN (1 TO 8 STEPS

AHEAD) ........................................................................................ 79

FIGURE 17. SPAIN RMSE ANALYSIS, DIFFERENT FORECAST HORIZONS (1 TO 8 STEPS

AHEAD) ........................................................................................ 81

FIGURE 18. RMSE GAP (%) WITH RESPECT TO THE DSGE-VAR, US (1 TO 8 STEPS

AHEAD) ........................................................................................ 82

FIGURE 19. GERMAN TRADE FLOWS (EXPORTS AND IMPORTS) AS A SHARE OF ITS

COUNTERPARTY TOTAL TRADE FLOWS, % ................................................ 93

Macroeconomic Analysis and Forecasting: An Empirical Investigation 16 Carlos Cuerpo Caballero – June 2017

Chapter 1 : Introduction Carlos Cuerpo Caballero – June 2017 17

1 INTRODUCTION

1.1 Motivation

Policy-makers and academics live in very different worlds and face different constraints Benoît Cœuré, 2014 The coming of a generation of young and brilliant economists in the late 70s (including E. Phelps, F. Kydland, E. Prescott, T.J. Sargent and N. Wallace amongst others) led by Robert Lucas started a scientific revolution à la Kuhn in the field of macroeconomics (see de Vroey and Malgrange, 2011). The business cycle took a dominant role as a research field. Cyclical fluctuations were originated by optimizing agents making optimal use of imperfect information in the face of economic shocks (Lucas and Rapping, 1969). Kydland and Prescott (1982) went a step further, bringing these models closer to the empirical evidence by assigning realistic values to the parameters (calibration techniques) and providing numerical solutions to the resulting systems of simultaneous equations (real business cycle models).^1 The contributions by Lucas and the other leading New Classical economists inaugurated the Dynamic Stochastic General Equilibrium (DSGE) era, defined by dynamic economic relationships (with optimizing agents) and stochastic shocks affecting the economy, in a general equilibrium framework. This framework was flexible enough to overcome its initial weaknesses with progressive improvements on the margin. A decade after and ever since, New Keynesian prominent economists (e.g. G. Akerloff, Y. Yellen, O. Blanchard, G. Mankiw, B. Bernanke, M. Woodford, J. Gali or N. Kiyotaki) would keep the Real Business Cycle core of optimizing agents with microfounded decision problems in a dynamic general equilibrium context, but challenge some more (^1) Undoubtedly taking advantage of the on-goingcomputational advances and data availability.

Chapter 1 : Introduction Carlos Cuerpo Caballero – June 2017 19

- International Transmission of Shocks : Calibration of the international transmission channels according to weighted trade, financial and contagion flows.

1.2 Imbalances and the Business Cycle

Policymakers strive to understand the dynamics of the business cycle and determine its specific location as a policy-relevant variable. The slack in the economy or output gap is, however, not observable and surrounded by considerable uncertainty. Along the quest for the best output gap estimate, the literature has developed a myriad of estimation techniques over the last decades, ranging from data- driven univariate filters to structural general equilibrium models.^3 However, the horse race in search of an optimal output gap estimation methodology seems far from settled. The uncertainty surrounding the output gap estimates has proven a challenging task, leading to unreliable estimates in real time, which is the policy-relevant time frame. Moreover, there is a lack of a well-defined metric or comparable benchmark for the different estimates. This analysis presents an empirical approach overcoming these two limitations, based on a structural multivariate time series model and Kalman filtering, with an application to the Spanish economy. This chapter defines a new selection algorithm based on a set of selection criteria defined along three dimensions: (i) statistical goodness (e.g. minimizing the end-point problem); (ii), economic soundness (e.g. “smell test” and consistency with selected stylized facts); and (iii) transparency or replicability. The focus for the selection of a specific output gap estimate is thus diverted from the traditional comparison between different methodologies along the selected criteria. As a novelty, different specifications of the multivariate (^3) See for example Álvarez and Gómez-Loscos (2017), Alichi (2015) and Murray (2014) for a review of different estimation techniques.

Macroeconomic Analysis and Forecasting: An Empirical Investigation 20 Carlos Cuerpo Caballero – June 2017 unobserved components model are tested by combining output series with potential candidate variables sharing information about the business cycle. These include domestic (e.g. construction investment, capacity utilization, unemployment) open-economy (e.g. current account, exchange rate), financial (credit to non-financial corporations, M3) and price (e.g. GDP deflator, CPI, house prices) candidates. The selected approach allows for country-specific cycle definitions, generalizing the work in Borio et al. (2017) and Alberola et al. (2013). Multivariate filters and the unobserved components multivariate Kalman filter technique represent a good compromise between these criteria. The multivariate framework allows for a country-specific approximation as it could accommodate specific cycles (financial, external, investment, fiscal, etc.) by considering additional variables related to the cycle.

1.3 Forecasting Along the Business Cycle

The ability of economists to forecast the main aggregate macroeconomic variables has undergone a complete revolution in the last 40 years. However, the absence of an agreed model to forecast the main economic aggregates at different time horizons remains an important challenge for econometric analysis, especially considering the recent financial crisis. Initially, multivariate vector autoregressive (VAR) models became the workhorse in macroeconomic forecasting, following the work by Box and Jenkins (1970) and Sims (1980). These non-structural models had two main advantages. On the one hand, they were not subject to the Lucas (1976) critique, as their forecasts were not tied to a specific path of the policy variables. On the other hand, Unrestricted VAR (UVAR) models did not impose excessive identification restrictions, leading to a better in-sample fit. However, good in-sample fit did not grant a good out-of-sample forecasting performance, as indicated in Stock and Watson (1996) work. Increasing the number of variables could generate inaccurate estimates and bad predictive results due to over-fitting. These limitations led to the development of two important lines of research. First, Bayesian VAR (BVAR) models (Doan, Litterman and Sims, 1984),