Download Management Accounting - ABC method and more Summaries Management Accounting in PDF only on Docsity!

Chapter 2

System Design:

Activity Based Costing

Learning Objectives

1. Understand the basic approach in activity-based

costing and how it differs from conventional costing.

2. Compute activity rates for an activity-based costing

system.

3. Compute product costs using activity-based costing.

4. Contrast the product costs computed under activity-

based costing and conventional costing methods.

5. Understand benefits and limitations of activity-

based costing.

6. Record the flow of costs in an activity-based costing

system.

Learning Objective 1

Understand the basic approach in activity-based

costing and how it differs from conventional costing.

3 - 3

When cost systems were developed in the 1800s, the emphasis was on simplicity because:

- Cost and activity data had to be collected by hand and all calculations were done with paper and pencil.

- Most companies produced a limited variety of similar products, so there was little difference in the overhead costs consumed by each product.

Assigning Overhead Costs to

Products

3 - 4

Departmental Overhead Rates

Machining Department

Shipping Department

Assembly Department

Many companies have a system in which each department has its own overhead rate.

The allocation base depends on the nature of the work performed in each department. In the machining department, overhead may be based on machine-hours, but in the assembly department, overhead may be based on labor-hours.

3 - 7

Activity-base costing is required to account for these

other factors.

The departmental approach relies

exclusively on volume-related allocation bases while

some overhead costs may be caused by factors

that are not related to the volume of production.

Departmental rates will not correctly assign overhead

in situations where a company has a range of

products and complex overhead costs.

Departmental Overhead Rates

3 - 8

A number of allocation bases are

used for assigning costs to products.

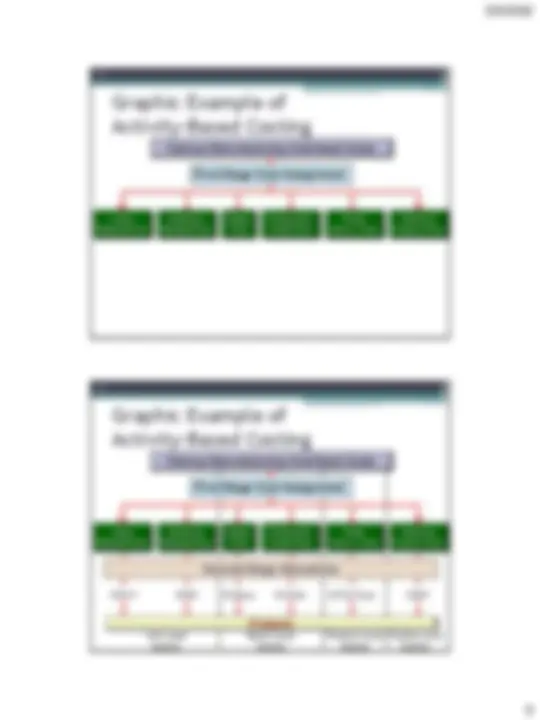

Activity-Based Costing (ABC)

3 - 9

Cost

Activity-Based Costing (ABC)

Consumption of Resources

Activities

Cost Objects (e.g., products and customers)

3 - 10

Activity-Based Costing (ABC)

For each activity in isolation, this system works exactly like the job-order costing system

A predetermined overhead rate is computed for each activity and then applied to jobs and products based on the amount of activity consumed by the job or product.

3 - 13

Designing an Activity-Based

Costing System

The challenge is to select a reasonably small number of activities that explain the bulk of the variation in overhead costs.

Activities are usually chosen by interviewing a broad range of managers to find out what activities they think consume most of the organization’s resources.

3 - 14

Related activities are

frequently combined to reduce

the amount of detail and

record-keeping costs.

An activity dictionary defines each of the activities that will be included in the activity-based costing system and how the activities will be measured.

For example, several activities may

be involved in handling and moving

raw materials, but these may be

combined into a single activity

entitled material handling.

Designing an Activity-Based

Costing System

3 - 15

Hierarchy of Activities

Level Activities Activity Measure Unit-level Processing units on machines Machine-hours Processing units by hand Direct labor-hours Consuming factory supplies Units produced Batch-level Processing purchase orders Purchase orders processed Processing production orders Production orders processed Setting up equipment Number of setups Handling materials Pounds of material handled Product-level Testing new products Hours of testing time Administering parts inventories Number of part types Designing products Hours of design time Facility-level General factory administration Direct labor-hours Plant building and grounds Direct labor-hours

3 - 16

Using Activity-Based Costing

Comtek Sound, Inc.

Comtek Sound, Inc. makes two products: CD

players and DVD players.

The company has been losing bids to supply CD

players, its main product, to lower priced

competitors.

The company has been winning all bids to

supply DVD players, its secondary product.

3 - 19

Using Activity-Based Costing

Comtek Sound, Inc.

For the current year, Comtek has budgeted sales

of 50,000 DVD units and 200,000 CD units.

Comtek’s traditional cost system applies

manufacturing overhead to products based on

direct labor hours.

Both products require two direct labor-hours to

complete, for a total of 500,000 direct labor

hours.

Hours DVDs: 50,000 units @ 2 hours per unit = 100, CDs: 200,000 units @ 2 hours per unit = 400, Total direct labor-hours 500,

3 - 20

Using Activity-Based Costing

Comtek Sound, Inc.

Unit costs for materials and labor are:

DVD CD Units Units Direct materials $ 90 $ 50 Direct Labor $ 20 $ 20

3 - 21

Total manufacturing overhead costs for the current year are estimated to be $10,000,000. The company develops the following overhead rate based upon labor-hours:

Predetermined overhead rate

= = $20 per DLH

$10,000, 500,000 DLHs

Direct Labor-Hours as a Base

3 - 22

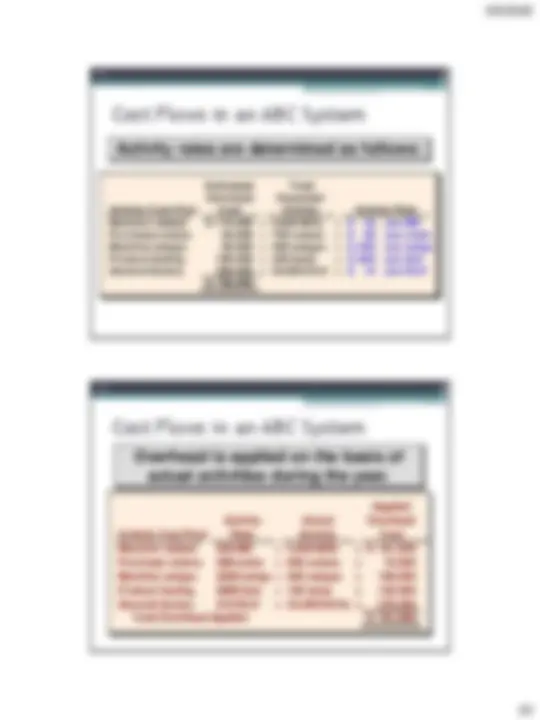

The ABC project team at Comtek has developed the following basic information.

Activity and Activity Measures

Estimated Overhead Cost Total DVD CD Labor related (DLH) $ 800,000 500,000 100,000 400, Machine related (MH) 2,100,000 1,000,000 300,000 700, Machine setups (setups) 1,600,000 4,000 3,000 1, Production orders (orders) 3,150,000 1,200 800 400 Parts administration (part types) 350,000 700 400 300 General factory (MH) 2,000,000 1,000,000 300,000 700, $10,000,

Expected Activity

Computing Activity Rates

3 - 25

We can calculate the following activity rates:

Activity and Activity Measures

Estimated Overhead Cost

Total Expected Activity Labor related (DLHs) $ 800,000 ÷ 500,000 = $ 1.60 per DLH Machine related (MHs) 2,100,000 ÷ 1,000,000 = 2.10 per MH Machine setups (setups) 1,600,000 ÷ 4,000 = 400.00 per setup Production orders (orders) 3,150,000 ÷ 1,200 = 2,625.00 per order Parts administration (part types) 350,000 ÷ 700 = 500.00 per part type General factory (MHs) 2,000,000 ÷ 1,000,000 = 2.00 per MH $10,000,

Activity Rate

Using the new activity rates, let’s assign overhead

to the two products based upon expected activity.

Computing Activity Rates

3 - 26

Learning Objective 3

Compute product costs using activity-based costing.

3 - 27

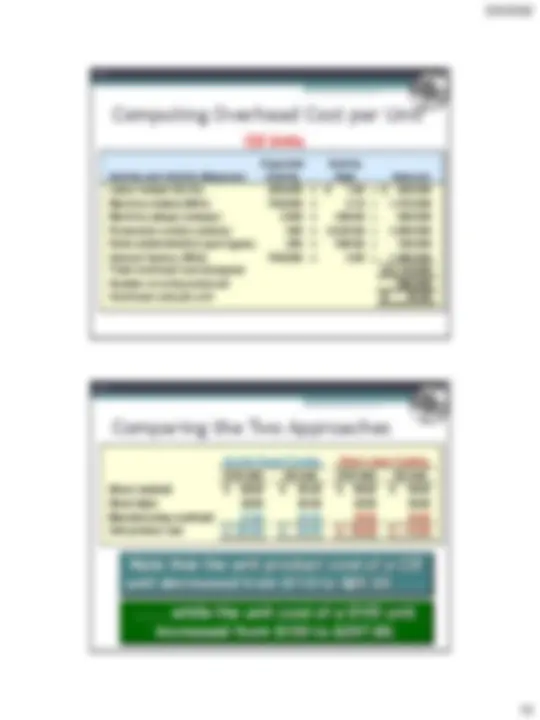

Computing Overhead Cost per Unit

Activity and Activity Measures

Expected Activity

Activity Rate Labor related (DLHs) 100,000 × $ 1.60 = $ 160, Machine related (MHs) 300,000 × 2.10 = 630, Machine setups (setups) 3,000 × 400.00 = 1,200, Production orders (orders) 800 × 2,625.00 = 2,100, Parts administration (part types) 400 × 500.00 = 200, General factory (MHs) 300,000 × 2.00 = 600, Total overhead cost assigned $4,890, Number of units produced 50, Overhead cost per unit $ 97.

Amount

DVD Units

3 - 28

Learning Objective 4

Contrast the product costs computed under activity-

based costing and

conventional costing methods.

3 - 31

DVD Unit CD Unit DVD Unit CD Unit Direct material $ 90.00 $ 50.00 $ 90.00 $ 50. Direct labor 20.00 20.00 20.00 20. Manufacturing overhead 97.80 25.55 40.00 40. Unit product cost $ 207.80 $ 95.55 $ 150.00 $ 110.

Activity-Based Costing Direct-Labor Costing

Comparing the Two Approaches

The ABC system assigns $14.

less overhead than the traditional

system to each CD player.

3 - 32

DVD Unit CD Unit DVD Unit CD Unit Direct material $ 90.00 $ 50.00 $ 90.00 $ 50. Direct labor 20.00 20.00 20.00 20. Manufacturing overhead 97.80 25.55 40.00 40. Unit product cost $ 207.80 $ 95.55 $ 150.00 $ 110.

Activity-Based Costing Direct-Labor Costing

Comparing the Two Approaches

The ABC system assigns $57.

more overhead than the traditional

system to each DVD player.

3 - 33

DVD Unit CD Unit DVD Unit CD Unit Direct material $ 90.00 $ 50.00 $ 90.00 $ 50. Direct labor 20.00 20.00 20.00 20. Manufacturing overhead 97.80 25.55 40.00 40. Unit product cost $ 207.80 $ 95.55 $ 150.00 $ 110.

Activity-Based Costing Direct-Labor Costing

When a company implements activity-based costing,

overhead cost often shifts from high-volume to low- volume products with a higher unit product cost resulting for the low-volume products.

Low-volume product

Shifting of Overhead Cost

3 - 34

Benefits of Activity-Based Costing

ABC improves the accuracy of product costing by:

- Increasing the number of cost pools used to accumulate

overhead costs.

- Using activity cost pools that are more homogeneous than

departmental cost pools.

- Assigning overhead costs using activity measures that

cause those costs, rather than relying solely on direct

labor hours.

3 - 37

Costs of implementing an ABC system may outweigh

the benefits. However, the benefits are more likely to be

worth the costs when:

1. Products differ substantially in volume, batch size, and in

activities required.

2. Conditions have changed substantially since the existing

cost system was established.

3. Overhead costs are high and increasing and no one seems

to understand why.

4. Management does not trust the existing cost system and it

ignores data from it when making decisions.

Limitations of Activity-Based Costing

3 - 38

The cost in each activity pool is strictly proportional to its activity measure. When this assumption is violated, the accuracy of ABC data can be called into question.

Activity-Based Costing

Critical Assumption

For example, managers should be particularly alert to product costs that contain allocated facility-level costs.

3 - 39

Modifying the ABC Model

The illustrations in the chapter assume that ABC is being used for external reporting purposes. If the system is used for internal decision-making purposes, two important modifications should be made:

- Selling and administrative costs should be assigned to products, where appropriate.

- Facility-level costs should be removed from product costs.

3 - 40