Download Understanding Cost Classification & Income Statement in Marginal & Absorption Costing and more Study notes Accounting in PDF only on Docsity!

BAFS Learning and Teaching Example

Learning Objectives:

1. To distinguish the difference between marginal and absorption costing;

2. To explain the profit impacts between marginal and absorption costing in profit

calculations; and

3. To state the advantages and disadvantages of a marginal and absorption costing

systems.

Overview of Contents:

Lesson 1 Marginal and Absorption Costing

Lesson 2 Arguments for and against Marginal and Absorption Costing

Prior Knowledge:

Student should know:

1. how to create a manufacturing account and income statement in financial

accounting;

2. the differences between prime / direct cost, factory overhead / indirect cost, and

non-production cost / administrative and selling overheads;

3. the allocation of cost / expenses to production cost and non-production cost; and

4. the calculation of production costs under an absorption costing system.

Resources:

Topic Overview, Teaching Plan and Answers to Student Worksheet

PowerPoint Presentation

Student Worksheet

Suggested Activities

Case Study

Group Debate

Crossword Puzzle

Topic Overview

Topic BAFS Elective Part – Accounting Module – Cost Accounting

A08: Marginal and Absorption Costing

Level S5 / S

Duration 2 lessons (40 minutes per lesson)

BAFS Learning and Teaching Example

Lesson 1

Theme Marginal and Absorption Costing

Duration 40 minutes

Expected Learning Outcomes:

Upon completion of this lesson, students will be able to:

1. Define marginal and absorption costing;

2. Distinguish differences between marginal and absorption costing;

3. Prepare profit statements based on a marginal costing and an absorption costing

system; and

4. Explain the difference in profits between marginal and absorption costing profit

calculations.

Teaching Sequence and Time Allocation:

Activities Reference

Time

Allocation

Part I: Introduction

Teacher reviews the definition of fixed and variable

costs and asks students to give examples in relation to

their family’s monthly expenses.

Activity 1 – Case Study

Teacher asks students to identify fixed and variable

costs, production and non-production costs in a

manufacturing account and income statement of

Pattie Company and calculate the unit product

costs for the month of June Year 8 (Task 1 and 2).

Teacher informs students of two main accounting

streams: financial accounting and cost accounting.

Financial accounting is concerned with the

provision of information to external parties. Cost

accounting is concerned with the provision of

information to internal parties. A number of

costing systems are being applied by organisations

PPT#1-

Student

Worksheet

pp.1-

15 minutes

BAFS Learning and Teaching Example

Lesson 2

Theme Arguments for and against Marginal and Absorption Costing

Duration 40 minutes

Expected Learning Outcomes:

Upon completion of this lesson, students will be able to:

1. Explain the advantages and disadvantages of marginal costing;

2. Explain the advantages and disadvantages of absorption costing; and

3. Explain circumstances when suitable to use marginal or absorption costing.

Teaching Sequence and Time Allocation:

Activities Reference

Time

Allocation

Part I: Introduction

Teacher starts the lesson by introducing the problem

faced by Alice, the Managing Director of Bullet

Manufacturing Company and asks students to set up a

debate on the adoption of a marginal costing system in

the company.

PPT #36 4 minutes

Part II: Content

Activity 3 – Preparation for the debate

Students are divided into two groups; one is the

affirmative side and the other is the negative side.

Students are required to discuss within their groups

and to develop arguments.

Each group nominates one representative to take

part in the debate.

PPT

Student

Worksheet

pp.17-

15 minutes

Activity 3 – Debate

Each representative has 4 minutes to present their

group’s views and arguments.

Teacher decides winner, concludes the debate and

introduces suitable circumstances for using

marginal and absorption costing.

PPT #38-45 12 minutes

BAFS Learning and Teaching Example

Part III: Conclusion

Teacher concludes session by highlighting the

advantages of marginal and absorption costing and asks

students to choose the preferred costing methods under

different circumstances.

Teacher asks students to complete the crossword puzzle

at home to check their understanding on the concepts of

marginal and absorption costing. The answers will be

distributed during next lesson.

PPT #46 – 48

Student

Worksheets

pp.20-

9 minutes

BAFS Learning and Teaching Example

Task 2: Cost Computation

Total Production Cost: $76,

Unit Produced: 2,

Unit Product Cost = Total Production Cost ÷ Unit Produced

= $76,200 ÷ 2,540 units

= $

Task 3: Income Statement

(a)Unit Selling Price = Sales Revenue ÷ No of units sold

= $191,475 ÷ (57 + 2,540 – 44)

= $191,475 ÷ 2,

= $

Variable Production Cost = $(30,600 + 20,800 + 5,000 + 1,800)

= $58,

Closing Stock Value (44 units) = $58,200 ÷ 2,540 x 44

= $1,

Variable Non-production Cost = $(195 + 445)

= $

Fixed Production Cost = $(9,000 + 500 + 7,000 + 600 + 900)

= $18,

Fixed Non-production Cost = $(750 + 250 + 159 + 12,643 + 190 + 7,905)

= $21,

BAFS Learning and Teaching Example

Income Statement for the month ending 30 June Year 8 (Marginal Costing) HK$ HK$ Sales 191, Less: Variable Production Cost of Goods Sold Finished Goods Opening Stock 1, Add: Variable Production Cost 58, 59, Less: Finished Goods Closing Stock 1,008 58, 133, Less: Variable non-production cost 640 Contribution 132, Less: Fixed cost Production 18, Non-production 21,897 39, Net profit 92,

(b)

Major Effect:

Profit calculated under Marginal Costing is higher than that

of Absorption Costing.

Reason:

The closing inventory value calculated under the Absorption

Costing method is higher than Marginal Costing, as fixed

production costs are treated as product and costs will be carried

forward to the next accounting period if unsold. Therefore, a

decrease in the stock levels mean a larger portion of the fixed

costs will be charged to the current accounting period under

Absorption Costing and the profit calculated will be lower than

that of Marginal Costing.

BAFS Learning and Teaching Example

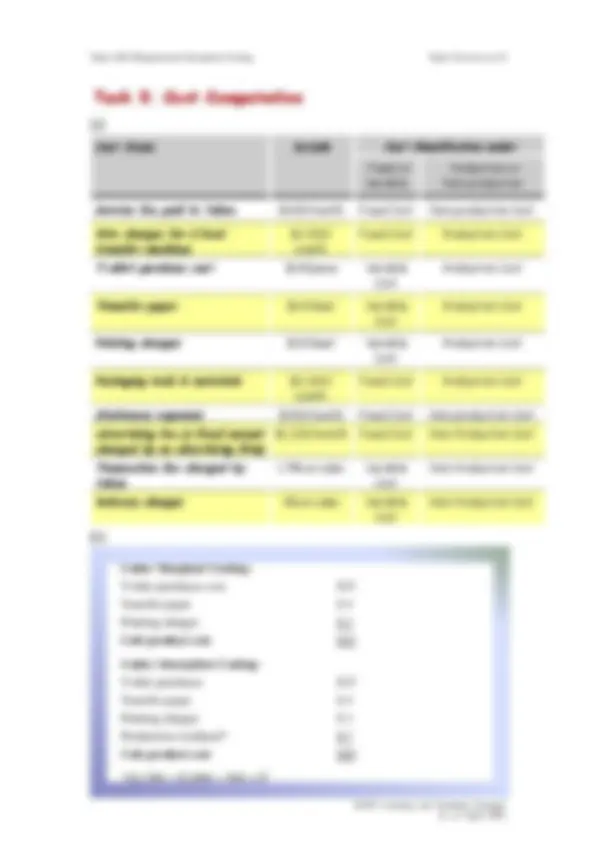

Task 3: Cost Computation

(a)

Cost Items Details Cost Classification under

Fixed or Variable

Production or Non-production

Service fee paid to Yahoo $400/month Fixed Cost Non-production Cost

Hire charges for 2 heat

transfer machines

month

Fixed Cost Production Cost

T-shirt purchase cost $15/piece Variable

Cost

Production Cost

Transfer paper $4/sheet Variable

Cost

Production Cost

Printing charges $3/sheet Variable

Cost

Production Cost

Packaging tools & materials $2,000/

month

Fixed Cost Production Cost

Stationery expenses $300/month Fixed Cost Non-production Cost

Advertising fee (a fixed amount

charged by an advertising firm)

$1,000/month Fixed Cost Non-Production Cost

Transaction fee charged by

Yahoo

1.5% on sales Variable Cost

Non-Production Cost

Delivery charges 1% on sales Variable

Cost

Non-Production Cost

(b)

Under Marginal Costing:

T-shirt purchases cost $

Transfer paper $ 4

Printing charges $ 3

Unit product cost $

Under Absorption Costing:

T-shirt purchases $

Transfer paper $ 4

Printing charges $ 3

Production overhead* $ 7

Unit product cost $

*($1,500 + $2,000) ÷ 500 = $

BAFS Learning and Teaching Example

Task 4: Profit Computation

(a) Absorption Costing

1 st^ month 2 nd^ month 3 rd^ month Total

HK$ HK$ HK$ HK$

Sales 21,750.00 17,400.00 23,925.00 63,075. Less: Production cost of sales Opening stock - - 2,900.00 - Production cost 14,500.00 14,500.00 14,500.00 43,500. Closing stock - (2,900.00) (1,450.00) (1,450.00) 14,500.00 11,600.00 15,950.00 42,050. Gross profit 7,250.00 5,800.00 7,975.00 21,025. Less: Non-production cost Fixed 1,700.00 1,700.00 1,700.00 5,100. Variable 543.75 435.00 598.13 1,576. Net profit 5,006.25 3,665.00 5676.87 14,348.

(b) Marginal Costing

1 st^ month 2 nd^ month 3 rd^ month Total

HK$ HK$ HK$ HK$

Sales 21,750.00 17,400.00 23,925.00 63,075. Less: Variable production cost of sales Opening stock - - 2,200.00 - Variable production cost 11,000.00 11,000.00 11,000.00 33,000. Closing stock - (2,200.00) (1,100.00) (1,100.00) 11,000.00 8,800.00 12,100.00 31,900. Variable non-production cost

Contribution 10,206.25 8,165.00 11,226.87 29,598. Less: Fixed cost Production 3,500.00 3,500.00 3,500.00 10,500. Non-production 1,700.00 1,700.00 1,700.00 5,100. Net profit 5,006.25 2,965.00 6,026.87 13,998.

BAFS Learning and Teaching Example

Arguments for the proposition (hints: students are required to emphasise the advantages of Marginal Costing and disadvantages of Absorption Costing )

Advantages of Marginal Costing z Easy to understand – avoids arbitrary allocation of fixed overheads. z Fixed overhead is excluded from inventory costs – avoids the varying charges per unit and hence distortion in stock valuations. z Fixed overheads are NOT carried forward in stock valuations – avoids the effect of changes in closing inventory level on profits. z Contribution and profits are directly driven by sales – shows clearly the effect of sales on cash flows and relationships between cost, price and volume. z Focuses on controllable business aspects – facilities execution of cost controls.

Disadvantages of Absorption Costing z More complicated – have to make arbitrary assumptions on apportionment of fixed overheads. z Fixed overheads are charged to production – unit inventory costs may vary according to production. z Part of the current year’s fixed overhead is carried forward in closing stock to the following year – management may manipulate profits by building up inventories and hence deferring the fixed overheads to the following years. z Profit is not a direct function of sales. There’s a possibility that profit may drop even though sales are up. z Relationships between cost, price and volume are ignored since the focus is on total cost.

Answer to Activity 3

BAFS Learning and Teaching Example

Arguments against the proposition (hints: students are required to emphasise the advantages of Absorption Costing and disadvantages of Marginal Costing )

Advantages of Absorption Costing z Fixed costs are absorbed in inventory – ensures all fixed costs will be recovered and met in the long run. z Recognition of the importance of fixed overheads in production – finished goods and work in progress stock will not be understated, giving a true and fair view of the firm’s financial affairs. z Compliance with Accounting Standards – is useful for external reporting. z All costs are variable in the long run – recognises all “long run variable” costs. z Less profit fluctuations when production remains constant but sales fluctuate.

Disadvantages of Marginal Costing z It ignores that fixed costs must be recovered in the long run, so if selling price is based only on marginal costs, it’s possible that a positive contribution might NOT be sufficient to cover all fixed costs in the long run. z Finished goods and work in progress stock will be understated. z Exclusion of fixed costs from stock valuations does not conform to acceptable accounting practices. z It fails to recognise that all costs are variable in the long run. z For firms that have a seasonal sales pattern, profits tend to fluctuate greatly. Losses are reported during the slack season while huge profits are reported during the peak session. z It’s not easy to establish the variability of costs, as variable costs are rarely completely variable and fixed cost are rarely completely fixed.

BAFS Learning and Teaching Example

(^3) V 1 A R I A B L E (^4) C O N T R I B U T I O N 8 C

S O O 7 C N (^1) M A R G I N A 5 L T (^2) P P S O R 3 F (^6) G R E A T E R H W 6 S O I O I 7 E Q U A L 4 O X D O R M P E U 5 U N D E R 2 O V E R H E A D C N T I (^8) P R O D U C T I O N G

Answer to Activity 4

1

BAFS Elective Part

Accounting Module –

Cost Accounting

Marginal and Absorption Costing Topic A08:

Education Bureau, HKSARGCurriculum Development InstituteTechnology Education Section

April 2009

Lesson 2 – Arguments for and against Marginal and Absorption CostingLesson 1 – Marginal and Absorption CostingContentsTwo 40-minute lessonsDurationstudy.build a solid understanding through active participation in debate and caseabsorption costing and their impact on profit calculations. Students willThis session aims to help students distinguish between marginal andIntroduction

2

2

Marginal and Absorption CostingTopic A

BAFS Elective Part

Learning and Teaching Example

Fixed Costs

- Teacher provides examples of fixed costs. They includefluctuations in the level of activity. (CIMA Official Terminology)within certain output and turnover limits, tends to be unaffected byDefinition of fixed cost: A cost which is incurred for a period, and which, Teacher starts the lesson by introducing the definition of fixed cost. Lesson 1 Business registration fee

Factory/office rent

Factory/office rates

Factory/office management fee

Supervisors’/executives’ salaries

Depreciation of factory building/equipment/machinery

Fire insurance of factory building/equipment/machinery

5

5

Marginal and Absorption CostingTopic A

BAFS Elective Part

Learning and Teaching Example

to your family’s monthly expenses Examples of variable cost in relation

Examples are:family’s monthly expenses. Teacher asks students to give examples of variable costs in relation to their Traveling expenses

Food

Electricity charges

Gas fee

Clothing

Entertainment expenses

Water charges

Motor vehicle running expenses

6

6

Marginal and Absorption CostingTopic A

BAFS Elective Part

Learning and Teaching Example

AActivity 1

ctivity 1:

PattiePattie Company

Company

(Refer to Student Worksheet Page 1 to 3)

questions raised by the owner, Pattie. Teacher asks students to read the case and pay special attention on the

7

Marginal and Absorption CostingTopic A

BAFS Elective Part

Learning and Teaching Example

z Pattie Company

Manufacturing Account

z

Income Statement

are given for information. The manufacturing account and income statement of the Pattie Company

8

Marginal and Absorption CostingTopic A

BAFS Elective Part

Learning and Teaching Example

z Pattie Company

and variable cost?Except direct, indirect cost, what are fixed

z

production cost?Are there any other ways to calculate the

- Highlights of the case: friends and wants to know their meanings.The owner, Pattie, has heard about fixed and variable costs from her

the production costs and the unit product costsPattie asks the accountant to propose an alternative method to calculate