Disclaimer: the content s of this practice case (scope, information, and data) has b een created solely for training purposes .

Practice Case

NEW CREDIT CARD LAUNCH

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

A large multinational credit card company has been considering launching its first store card, specifically within the grocery retail space.

Typology: Slides

1 / 18

This page cannot be seen from the preview

Don't miss anything!

A large multinational credit card company has been considering launching its first store card, specifically within the grocery retail space. For reference, store cards, also known as private-label cards, are credit cards that consumers can use only at the store associated with that card (i.e., a Lowe's card can only be used at Lowe's, but not any other merchant). Should this credit card company launch a store card within the US grocery retail market? Background information Before you structure your thoughts, what immediate questions come to mind that can support your understanding?

Size of grocery retail market Predicted growth of grocery retail market Competitive landscape – private label players and grocery retailers Customers – segments, behaviors and trends Externalities – tech trends (e.g., auto checkouts), data regs. Expected product revenue Expected product costs – initial, ongoing, opportunity Client capabilities/advantage (e.g., bundle, cross-sell, supply chain) Deprioritized dimensions 1 Market opportunity Primary factors Sub-factors Things to consider: Should our client launch a private-label grocery card? What market specifics would you like to have more information on? 2 Profitability 3 Go-to-market strategy 4 Strategic alignment

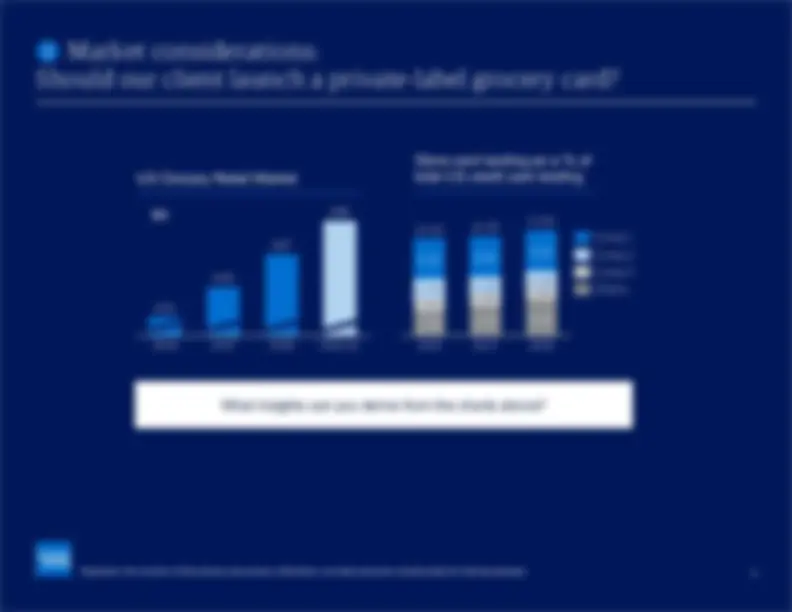

Market considerations: Should our client launch a private-label grocery card? What insights can you derive from the charts above? 1 2015 685 2017 649 2019 2021 (f) 633 667 $M US Grocery Retail Market Store card lending as a % of total US credit card lending 3.25 3.75^ 4. 2.75 2.^

5.00 5.^

2015 2017

2019

Comp 2 Comp 1 Others Comp 3

Store Card Revenue Drivers

Assume the credit card company would like to charge a $100 annual fee for this store card product Profitability considerations: Should our client launch a private-label grocery card? How would you estimate revenues from interchange fees? Take a moment to think about what are the primary drivers for interchange fee revenues. Non-exhaustive 2

How would you estimate this number? Profitability considerations: Should our client launch a private-label grocery card? Average amount paid via credit card to grocery retailer (i.e. "Average account balance") X Interchange fee percentage Interchange fees revenue estimate 2

Est. annual revenue per customer Annual fee $ Interchange fees $ Interest on balances? Total? $50k x 20% x 50% x 2% Profitability considerations: Should our client launch a private-label grocery card? What information do we need to estimate interest revenue from past-due credit card balances? 2

Interest on past-due credit card balance revenue estimate Average amount paid via credit card to grocery retailer (aka "Average account balance") x % of accounts projected to roll over (i.e. be past due) X Interest rate Reuse same assumption as before: $50K x 20% x 50% Assume 10% Profitability considerations: Should our client launch a private-label grocery card? Based on the assumptions above, what is the total revenue estimate? Assume 10% 2

Number of customers Fixed costs Product-related variable costs

Revenue Cost = Profit Year 1 Subsequent years $250 x 80k $105M + (80k x (10+20)) + (Revenue x 3%) $20M $105M + $2.4M + $600K $20M ~$108M^ =^ - $88M

Revenue Cost^ =^ Profit $250 x 80k $5M + (80k x (10+20)) + (Revenue x 3%) $20M $5M + $2.4M + $600K $20M

2

Headline Supporting Detail Next steps Investing in a store-brand grocery card is not recommended at this time given the company’s mandate to break even on its product investment by Year 3