Download Telecommunications in Australia: Statistics and Trends and more Slides Voice in PDF only on Docsity!

Australian Infrastructure Audit 2019

556

Telecommunications

Telecommunications infrastructure covers the networks that carry voice and data between users across Australia, and our connections with the rest of the world, impacting on our liveability and productivity.

This includes wires, fibre, towers, sensors, satellites, radio spectrum and physical infrastructure such as data centres and cable landing stations, which come together as networks to deliver communications to and from our devices, whether we live and work in fast-growing cities or remote communities.

The inclusion of a federal regulatory power over ‘telephonic, and other like services’ in Australia’s Constitution in 1901 means that, since Federation, telecommunications is the only broad public infrastructure sector with an overarching national character.^1 Australia’s first telephone call was made just over 20 years earlier in 1879. 2 Telecommunications have since grown, with the help of significant technological advancements, to support the entire economy, and influence how we live our lives.

557

8. Telecommunications – Heading

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

559

- Telecommunications – Introduction

Telecommunications is more central to our

lives than it has ever been

Telecommunications is increasingly central to our personal lives and to the way we work and do business. It is becoming ubiquitous. Business and government are rapidly moving services online. As almost all of us rely on these services, access to networks that keep us connected is becoming essential.

Almost 90% of Australians accessed the internet through their mobile phone in 2018. 3 Some 59% of Australians now use four or more devices to access the internet.^4 On average, Australian adults spent over two full days per month accessing content on their smartphones in 2018. 5

Telecommunications networks are

constantly evolving

Of all infrastructure sectors, telecommunications is today the least recognisable sector from a generation before. Change is set to continue, as we are in the midst of the construction of Australia’s fixed line broadband network, and on the cusp of investment in a new generation of mobile networks.

Most of the telecommunications infrastructure in Australia is privately owned. The notable exception is the publicly-owned National Broadband Network (nbn), which is still under construction but has begun delivering services to users. The nbn network was designed to ultimately become the predominant wholesale provider of fixed line access services.

nbn’s governing legislation contemplates a change of ownership, from public to private hands, after it is built. With the nbn rollout due to be completed in 2020, how this major investment is utilised, upgraded and ultimately integrated with services from the private sector will significantly impact Australia’s telecommunications accessibility, quality and affordability.

nbn is solely a wholesale provider of broadband services, and sells access to its network to over 150 large and small retail service providers nationally,^6 including major players such as Telstra and Optus, and smaller retailers such as Bendigo Telco, Central Coast Internet and Telecom West.

In the mobile service area, the three major mobile network operators (MNOs) are Telstra, Optus and Vodafone. These operators sell access to their networks to a range of over 50 other mobile service operators.^7 These retailers are often active in particular parts of the country.

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

Australian Infrastructure Audit 2019

560

The nbn network rollout continues and

we are on the cusp of building new 5G

networks

Australians’ use of fixed broadband and mobile data has increased by 175% and almost 250% respectively, since 2015, but with 93% of the data delivered via fixed broadband. 8 These are growth rates many times faster than our economy overall.

The 2015 Audit indicated the transformative role the nbn would play in Australia’s future telecommunications landscape, and this promise holds true. In 2015, the Audit noted that 818, premises were nbn ready (about 7% of all premises), and that 346,000 had connected to the service by February 2015 (3% of premises). Today, the nbn is over half way to its target of delivering peak wholesale download data rates of at least 25 megabits per second to all premises, and 50 megabits per second to 90% of fixed line premises by 2020. 9 By March 2019, 8.8 million premises (around three quarters of all premises) were ready to connect to the network, and 5.1 million were already connected.^10

In 2015 we focused on 3G and 4G mobile services. In 2019, 2G and 3G mobile networks are largely obsolete, while there is significant ongoing private investment in 4G network upgrades. The arrival of 5G networks is on the horizon, with trials having begun already, and the likely step change is substantial.

Australians are positive about quality and

access to networks but are concerned

about paying more

Consumers are generally positive about the quality of their telecommunications services.^11 However, significant issues remain in rural and remote areas for mobile and broadband services.

There is a stronger positive view about the ease of access to telecommunications services, although once again, rural and remote Australians are less positive about their experience.^12

Consumers broadly see their telecommunications services as more costly than affordable, and there is resistance to paying more,^13 even as providers of broadband and mobile data services are increasing data quotas.

Australian Infrastructure Audit 2019

562

Performance of the sector

Access

Access

73% of businesses are already using cloud computing for data storage 23

Access Access

1 in 10 adults did not access the internet at least once in the six months leading to May 2018 17

Quality

Quality

Australia ranks

4th on mobile broadband speeds in June 2019 15

9 points Gap between cities over rural areas in performance on Australian Digital Inclusion Index 19

Quality

88% Average percentage of maximum plan speed delivered to customers using nbn fi xed broadband services 20

Quality

Cost

6.2% vs 2.2% Proportion of income spent on telecommunications by lowest earning 20% of the households versus highest 20%^21

Cost

44% Proportion of consumers that rate fixed broadband as costly 25

Cost

Telecommunications comprises

14% of average household infrastructure costs 24

80% Proportion of adults concerned about how their data is used by companies 22

15% vs 32% Change in proportion of users with monthly mobile data allowances over 10GB in one year to 2018 18

91%

of all data that is consumed is on fixed broadband^16

563

- Telecommunications – Introduction

Scale of the sector

867 Mobile black spot base stations part-funded by government 35

Asset

99.4% of the population are able to access mobile services at home 36

Asset

11.7 million

premises will be ready to connect to nbn by mid-2020 28

nbn

Asset

50

Customer

26.

million mobile handset subscribers in Australia 26

Customer

340% Estimated growth in household data usage between 2016 and 2026 29

Customer

5.5 million Estimated premises connected via the nbn network by mid-2019 34

nbn

Industry

Telstra’s shares in 2016

41% of mobile phone market

51% fi xed broadband 37

Industry

$1.78 billion

Industry

Annual community service obligation subsidy in telecommunications 32

Australia ranks fi rst for key enablers of mobile internet takeup 31

# 1

of regional households will have access to a fi xed broadband connection at the end of the nbn rollout^33

14% Estimated proportion of nbn- ready households using fibre to the premises at the end of the rollout 30

connected devices in an average household by 2026 27

70%

Access

Access

Access

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

565

- Telecommunications – Telecommunications enable productivity and innovation

Figure 2: Businesses rate telecommunications backbone services very highly

0% 20% 40% 60% 80% 100% Importance of digital technology services (% of survey respondents)

Mobile internet

Access to high-speed broadband

Cloud technology

Social media

Cybersecurity

E-commerce capability Intelligent software systems Internet of Things

Data analytics

Radio frequency identification devices

52.9% 8.8% 48.1% 12.5% 21.5% 42.7% 16.3% 42.3% 14.0% 53.1% 10.5% 59.3%

70.0%

6.7%

65.2%

6.4%

73.1%

4.5%

84.8%

2.2%

Rated very important Rated not important

Source: Australian Bureau of Statistics (2017) 39

Telecommunications infrastructure

supports economic growth

Telecommunications infrastructure networks play a critical role in supporting Australia’s economic productivity. This role is increasing as our economy becomes more reliant on digital technology and connectivity.

The nbn alone was estimated to generate $1.2 billion per annum in additional GDP in 2017 through new jobs, new businesses and increased productivity.^40 This is expected to grow to over $10 billion by 2021.^41 5G technology is also likely to improve Australia’s economic productivity by enabling fast signal speeds (lower latency), which underpin responsive technologies and applications, such as robotics. Conservative estimates calculate the contribution of 5G technology to GDP at $1,300 to $2,000 per capita after the first decade of rollout.^42 These estimates do not take into account the full consumer and non-market benefits, or potential benefits from distributional effects within and between industries.

There are also significant potential gains from 5G uptake in industries with low existing telecommunications technology intensity. IoT technologies and services are estimated to provide an annual boost to five key industries (construction, manufacturing, healthcare, mining and agriculture, fishing and forestry – representing around one- quarter of our economy today) of between $ billion and $300 billion.^43 The largest gains are expected in the construction industry, where a large amount of technical equipment is used, but adoption has been slowest to date.^44

Governments, businesses and households

are already embracing new technology

Evolving telecommunications infrastructure is already enabling governments, businesses and households to leverage new technologies to increase access to information, improve efficiency in service delivery, boost economic productivity and improve liveability. For example:

- Governments are using new technologies in health, education, smart cities and public safety applications. Online platforms are increasingly used to deliver services to citizens – examples are the Australian Government’s MyGov and Western Australia’s ServiceWA. At local government level, waste contractors have been using Radio Frequency Identification (known as RFID) technology for a decade, improving route management and allowing weighing of waste by household and to identify out of location bins.^45

- Businesses are embracing cloud computing, IoT, artificial intelligence and advanced robotics. Cloud storage and computing are reducing business costs. Businesses and governments are rapidly embracing cloud-based solutions to garner benefits including reduced hardware costs, mobile accessibility, and savings on security and redundancy. In 2017-18, Telstra reported an increase in cloud revenue of 14.4%.^46

- Households are becoming smarter as they embrace new technologies aimed at improving convenience and automating processes. This includes IoT technologies such as virtual assistants, smart lights, heating, air conditioning and security systems.

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

Australian Infrastructure Audit 2019

566

The Internet of Things

The IoT is a collection of internet-connected devices that are added to things – objects, infrastructure, places or worn by people.

These devices communicate with one another quickly and reliably, sending and receiving information, and in some instances controlling aspects of objects. This enables automation of a wide range of household and business processes, from smart watches and smart home applications such as virtual assistants, to autonomous vehicles, to sensors tracking hospital bed use, and autonomous drones carrying out predictive maintenance on remote infrastructure assets.

The Australian Communications and Media Authority (ACMA) quotes industry estimates that 29 billion devices will be connected worldwide by 2022, over 60% of which will relate to the IoT.^47

While many IoT devices already operate today, the introduction of 5G networks in Australia will accelerate the growth of the IoT in Australia. 5G networks will provide greater speed and higher data rates to increase the capacity of IoT technology, which will drive its uptake across a range of industries. The Bureau of Communications and Arts Research (BCAR) has estimated that the average Australian household will have at least 50 IoT devices by 2026. Other estimates anticipate double that amount.^48

Supporting the Internet of Things in cities and regions

Telstra is deploying two technologies to significantly expand its IoT coverage in buildings and wide areas.

Cat-M1 operates on the 4G network and enables IoT devices to have greater reach in distance and depth into buildings. Cat-M1 supports devices that by their nature are low complexity which makes it suitable for a variety of uses across agriculture as well as utilities, healthcare and supply chains. Coupled with range extension capability, Telstra provides customers with a Cat-M1 enabled device with a network footprint that is around three million square kilometres in area and penetrates far deeper into city buildings than 4G coverage has previously.

Narrow Band IoT (NB-IoT) targets both outdoor and deep indoor coverage, supporting long battery life. Uses include livestock and crop monitoring. In 2018, Telstra tested a long-range NB-IoT connection, a step towards increasing Telstra’s mobile footprint in rural and regional Australia. With this new capability, enabled with a software upgrade, Telstra’s NB-IoT coverage will increase to more than 3.5 million square kilometres (about 45% of Australia’s landmass).^49

152. Opportunity

Digital technologies are using telecommunications networks to enhance Australia’s economic productivity. Embracing these new technologies can be a source of competitive advantage for Australia and can improve outcomes for users.

When this

will impact:

0-5 5-10 10-15 15+

Where this

will impact:

Australian Infrastructure Audit 2019

568

Focusing on users is critical

Reflecting strong competition in the market, mobile service providers continually strive to understand and meet user needs in terms of network coverage and quality, price, data allowances and customer service. The ‘use case’ focus (that is, a focus on specific applications where a product could be used) of 5G development suggests this will continue for the new generation technology and its associated applications.

The vertical separation of the majority of fixed broadband supply – wholesale nbn and separate retail service providers – risks less effective customer focus and service differentiation, as nbn operates at a distance from users, and retail services providers are restricted in their service offerings to the speed tiers and wholesale products that nbn delivers.

While most Australian consumers and businesses enjoy access to the range of telecommunications services, this is not the case for all. Rural and remote areas, and certain demographic groups, risk being left behind digitally.

While Australia’s mobile footprint includes over 99% of the population (at their premises), it covers only one-third of total landmass, meaning little or no service for those working and travelling in rural and remote areas. IoT networks are likely to have more extensive coverage than mobile data due to longer signal ranges, but still leave large parts of the continent uncovered.

Securing networks requires protecting data

and balancing privacy

Cybersecurity is the practice of defending networks from malicious attacks. It involves commitment and action across sector regulators and participants, and requires proper governance, capacity building and cooperation. Australia has a strong international standing on cybersecurity. In 2017, the International Telecommunications Union placed Australia in the top ten for preparedness of the 162 countries surveyed, ahead of Canada and France but below the leaders Singapore and the United States. 54

Data governance is management of the integrity, use, availability, useability, and security of digital data owned or controlled by individuals, companies and governments. Australia’s data privacy regulation and enforcement has been rated as “heavy”. 55 The Privacy Commissioner has the power to initiate and conduct investigations, ensure compliance with the Privacy Act, and seek civil penalties for serious or repeated breaches of the Privacy Principles where remediation has not been implemented. 56 There is also sector-specific consumer data right regulations being implemented to empower consumers on use of their data, initially being implemented for banking. 57

Nonetheless, in a 2018 survey, Deloitte found over 80% of Australian adults surveyed expressed concern about how their personal data is used, stored and shared as a result of their online interactions with companies. 58 In 2016, Deloitte surveyed industry use of the latest regulatory compliance approach. 59 The best-ranked sectors were banking, finance, government, energy and telecommunications. Lower-rated sectors were retail, social media, media and real estate.

While Australia ranks highly on cybersecurity and data governance, community concern is high and cybercriminal techniques are constantly improving. As such, cyber-related policy and regulation need to continually stay ahead of new threats and reflect escalating data prevalence and importance.

154. Challenge

Cybersecurity risks, such as data privacy and system resilience, are growing as more Australians use more interconnected digital services. Failure to manage these risks could affect user engagement with new services, and reduce the potential benefits of these services. Network efficiency could also suffer.

When this

will impact:

0-5 5-10 10-15 15+

Where this

will impact:

569

- Telecommunications – The mobile coverage dilemma

8.3 The mobile coverage dilemma

At a glance While Australia’s mobile footprint includes over 99% of the population, it covers only one-third of total landmass, meaning there is limited service in particular rural and remote areas, for example along transport corridors.

5G mobile technology provides a potential step change in mobile telecommunications infrastructure for Australia, offering huge benefits including faster mobile data, minimal delays and the ability to separate services on the same network. However, the cost of rolling out 5G is high, and without a change in prioritisation, existing issues may be exacerbated in rural and remote areas.

This section also looks at how we allocate mobile spectrum. This is a finite resource that underpins mobile telecommunications, and affects service quality and cost.

Mobile coverage prioritisation creates

challenges in rural and remote Australia

While Australia has among the fastest mobile networks speeds in the world, coverage across the country is a challenge. This is because, while Australia’s mobile footprint includes over 99% of the population, it covers only one-third of total landmass. Mobile network coverage, quality and choice of providers therefore remain significant issues in parts of rural and remote Australia.

Delivery of new and upgraded mobile coverage is prioritised where population densities are highest – places where people live and businesses are located. While coverage in these places is essential and contributes to improved liveability and productivity, this prioritisation results in limited coverage in other crucial areas with lower population densities, such as along transport corridors, or in large landholdings away from homes and businesses, such as farms and stations.

A 2017 study led by CSIRO showed that more farm respondents (43%) reported ‘poor to no coverage’ across their farm, than those who reported ‘good to full coverage’ across their farm (34%) (Figure 4).^60 This difference is likely to reflect the combination of size of farms and proximity to urban centres (where mobile base stations are typically located).

Figure 4: Farmers have varying levels of coverage across their properties

1 (No coverage anywhere on the farm)

2 3 4 5 (Full coverage across entire farm)

0%

5%

10%

15%

20%

25%

30%

% of farmers 14%

17% 17%

23%

29%

Note: Respondents were asked “How do you describe your mobile coverage across your entire farm?” Source: Zhang et al. (2018) 61

Mobile network coverage, quality and choice of providers remain significant issues in rural and remote Australia. Australian major cities and inner regional areas account for 88.6% of the population yet only cover 3.5% of the total landmass.^62 BCAR has observed that for approximately one million square kilometres (around 13% of Australia’s total land area), Telstra is the only available mobile network, although this area includes less than 1% of the Australian population (Table 1).^63

Table 1: 3G and 4G population coverage is high, but the last 1%-2% of population have no service or lack choice

Provider 3G coverage 4G coverage Area covered by network

% of population % of population km^2 (millions) % of Australia area

Telstra 99.3% 98% 2.4 31%

Optus 98.5% 95% 1.0 13%

VHA (Vodafone) 97% 96.9% 0.9 12%

Note: VHA coverage includes roaming agreement with Optus.

Source: Australian Competition and Consumer Commission (2016) 64

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

571

- Telecommunications – The mobile coverage dilemma

Australia is well positioned as an early

adopter for 5G technology

Australia is well positioned as an early mover in the rollout of 5G networks. We rank as the overall world leader in key enablers of mobile internet adoption according to the GSM Association (GSMA), a leading global industry body in the mobile sector.

The 2017 Mobile Connectivity Index, a leading measure compiled by the GSMA, compares Australia

against 162 other countries.^70 We rank at the top of G20 nations overall, in terms of infrastructure, affordability and consumer readiness (Figure 5). Australia has led the overall index every year since

- This suggests there is potential for 5G adoption to be stronger and faster than previous mobile generations in Australia.

Telstra, Optus and Vodafone have announced plans to build national 5G mobile networks, with launches expected from all three in 2019.

Figure 5: Australia leads key competitors on readiness for mobile adoption

Australia New Zealand

Singapore Canada United Kingdom

South Korea

United States

Germany Japan China

0

20

40

60

80

100

Mobile connectivity index score

88.9 87.8 86.5 84.3 84.2 83.4 81.8 81.8 80.0 74.

Source: GSM Association (2017) 71

156. Opportunity

5G technology presents an opportunity for Australia and we are well positioned to embrace it ahead of other nations. Delivering 5G networks will help to accelerate Australia’s digital transformation, providing significant benefits to people, businesses and governments.

When this

will impact:

0-5 5-10 10-15 15+

Where this

will impact:

Mobile telecommunications is a highly

competitive market

There is a significant amount of competition in the mobile industry. There are three major players (Telstra, Optus and Vodafone) as well as smaller operators who utilise these networks. Mobile products are increasingly commoditised and show little variation between providers. Price is the main decision factor for consumers as there is less differentiation arising from their mobile networks, coverage and customer experience. Unlimited plans are becoming more common, reducing differentiation on capacity.

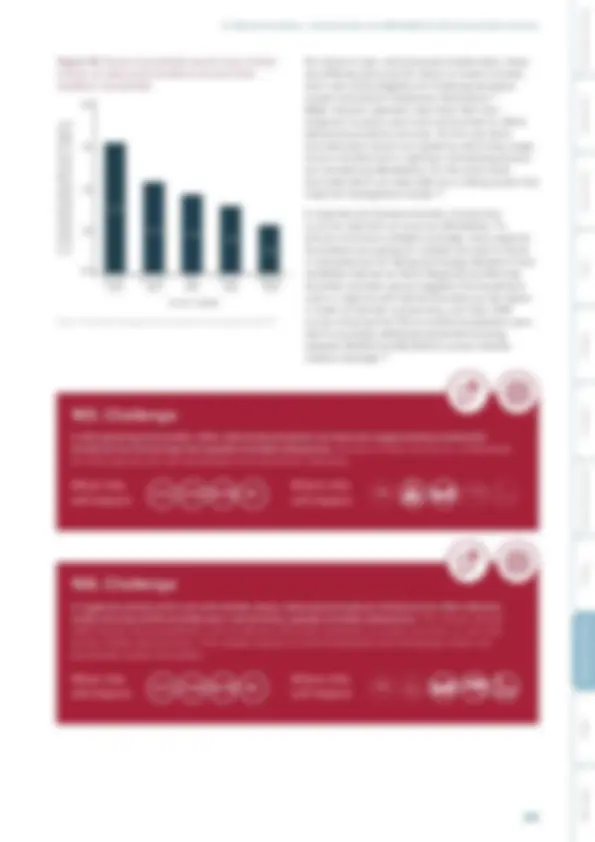

Complicating the competitive landscape, average revenue per user is falling for mobile network operators (Figure 6). This may be associated with new applications, such as internet based services that act as substitutes (for example, Skype and WhatsApp), displacing revenue-generating voice and mobile message services. The decline in traditional revenue sources incentivises mobile operators to move into new markets.

Figure 6: Mobile industry revenue per user is falling (including handset)

2010 2011 2012 2013 2014 2015 2016 2017 2018

30

40

50

60

Average mobile industry revenue ($/user/month)

$50.

$38.

Source: Venture Insights (2018) 72

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications

Australian Infrastructure Audit 2019

572

Major operators are expanding free Wi-Fi in

large and small cities

Traditional mobile services are also being displaced by expanding use of free Wi-Fi. Governments and MNOs are implementing Wi-Fi hotspots in public places across Australia, often for free, to maximise the potential of their network assets. Free Wi-Fi frequently offered to patrons in bars, cafes, and libraries complements mobile network coverage areas. For example, free Wi-Fi can now be found in shopping centres and in some CBD areas in cities.^73 TPG has provided backhaul to VicFreeWiFi in the Melbourne CBD, Bendigo and Ballarat, while Telstra’s Wi-Fi network provides its customers with access to over one million hotspots across Australia.^74

These public networks are more readily available in our cities and regional centres and where existing infrastructure is prevalent and covers dense populations, lowering the cost of additional expenditure to improve capabilities. Lower teledensities outside of cities and towns means that there are areas with no mobile coverage, or only one provider (usually Telstra). This is reflected in Telstra’s significantly higher market share in regional areas – particularly high in the non-urban parts of Tasmania and Western Australia.^75 However, new generation low Earth orbit satellites and high altitude platform stations (or high-altitude pseudo-satellites) may present opportunities to expand mobile coverage across much wider geographical areas, making these networks more economical in rural and remote areas.

Rolling out 5G could create cost and

planning challenges

The advent of 5G will require a new wave of infrastructure investment. While forecasts suggest that network costs could double as investors upgrade 4G and manage the evolution to 5G,^76 it is likely that MNOs will largely absorb and manage the additional required capital investment.

A major contributor to this cost is the need for more physical infrastructure than 3G and 4G. 5G requires

higher densities of towers and cells to address higher traffic loads and enable the use of higher radio frequencies. This will necessitate a shift towards using smaller cells in closer proximity to one another, and the deployment of a deep-fibre network. This creates challenges in retrofitting cities and in creating sufficient densities in more remote areas. However, analysis suggests that upgrading mobile tower sites, delivering small cells in high-density areas and moving towards nationwide rollout could be achieved within existing capital expenditure envelopes if carefully staged over the next five to seven years.^77

Though MNOs have some existing powers relating to telecommunications infrastructure deployment and installation,^78 there has been recent public opposition to the rollout of more cells without community consultation, particularly in cities.^79 Concerns around security and health are most commonly cited oppositions to these small cells, though experts have maintained that these concerns are no greater than those presented by larger telecommunications towers that already exist. 80

Currently, under the Telecommunications Act 1997 (Commonwealth), necessary equipment can be installed on public infrastructure such as light poles without the need to gain council approval. 81 The denser 5G rollout may increase operator focus on consultation with the community around use of these powers. The ACCC expects MNOs to be interested in sharing 5G cell infrastructure, particularly in fast- growing cities. 82 The use of other street objects and furniture, such as public transport signage and structures may help to reduce both the capital costs of rollout and allow smaller players to still maintain a presence in the market.

In rural and remote areas, it is likely that existing challenges faced with 3G and 4G coverage will be exacerbated with the rollout of 5G. This is because 5G services require higher densities of cells, and therefore higher costs to network owners. It is likely that rollouts will prioritise more densely populated areas, where the number of users is higher and the fixed costs can be met by a higher number of users.

157. Challenge

5G networks will require substantial new infrastructure, creating both cost, planning and security challenges. In cities, this means retrofitting new cells into existing streetscapes, and in rural and remote areas, this means creating adequate densities and improving coverage beyond that of 3G and 4G. Adequately balancing shared and competing tower and cell sites will affect the scale of investment, and ultimate costs users pay.

When this

will impact:

0-5 5-10 10-15 15+

Where this

will impact:

Australian Infrastructure Audit 2019

574

8.4 Maximising the benefits of nbn investment

At a glance With the nbn rollout almost complete, we must look at how to harness its benefits. This section covers:

- Tensions between nbn user outcomes and the need to provide a return on the capital investment from taxpayers

- Technological changes during the rollout that have affected quality - The need for comprehensive national coverage and associated funding challenges - Possible privatisation once the nbn is fully operational and the impact on market structure.

There is an inherent tension between

user outcomes and return on investment

for the nbn

The government-owned nbn was announced in April 2009 as a replacement for Telstra’s copper access network. The central aim was that every person and business in Australia, no matter where they were located, would have access to affordable, fast broadband.

It was structured off-budget and is required to eventually pay its way, including providing a return to the Australian Government, as owner. nbn provides wholesale services to commercial network operators, and other retail service providers.

The sole shareholder, the Australian Government, states the core objective for nbn as:

“….ensuring that all Australians have access to very fast broadband as soon as possible, at affordable prices, and at least cost to taxpayers. The Government expects the network will provide peak wholesale download data rates (and proportionate upload rates) of at least 25 megabits per second to all premises, and at least 50 megabits per second to 90 per cent of fixed line premises as soon as possible. nbn should ensure that its wholesale services enable retail service providers to supply services that meet the needs of end users”. 83

In effect, the nbn needs to achieve four goals:

- Supply technology to support defined minimum speeds (quality of service)

- Provide access to all premises no matter where they are located (accessibility)

- Sell wholesale access to retailers at prices that enable end user take up (affordability)

- Make a return on taxpayer investment (profitability). 84

The first three of these goals are focused on direct user outcomes, and over time may compete with the fourth goal, to make a return on the taxpayer capital investment.

For example, with consumer resistance to paying more for telecommunications services, there is pressure on nbn to reduce its wholesale prices. nbn implemented some changes to its wholesale prices in 2018, and there is evidence that this has increased take up, and improved speeds. 85 To the extent wholesale price reductions are passed on to consumers, this should increase retail take-up of nbn services at higher speeds. To the extent that wholesale prices are too high, this will reduce nbn take up, subdue the economic benefits of the infrastructure network, and encourage network duplication from the private sector.

Including the proposed Regional Broadband Scheme, nbn has forecast it will achieve an internal rate of return of 3.2% from:

- Steeply rising average revenue per user

- Users opting for higher speed tiers and downloading more data

- Limited market share loss to competing fixed and mobile networks. 86 However, there are concerns around the realisation of these assumptions given users’ apparent unwillingness to pay more for additional services, challenges in achieving fast speeds across all technologies, and the imminent rollout of competing 5G fixed wireless and mobile networks.

nbn has been structured as an off-budget entity, meaning that there is an expectation that shareholder equity will be repaid, with a return, from its growing operations. There are early budget impacts from the government’s cost of borrowing to make equity injections, and it has contingent liabilities noted in the budget. However, the ultimate outcome for taxpayers and the budget may not be known until the nbn is valued by the private sector in a sale process, including if prior write-downs were to occur. 87

The ACCC has expressed a concern that the nbn may not meet its financial targets. It has raised the possibility of taxpayer price relief via a range of means such as debt payment concessions or direct budget funding of non-commercial services, to better promote the efficient use of the network and the long-term interests of end users. 88

575

- Telecommunications – Maximising the benefits of nbn investment

159. Challenge

There is an inherent tension between the nbn’s strategic goals, requiring potential trade-offs between achieving user outcomes and delivering a return on the capital investment made by taxpayers. If all goals cannot be achieved, the ability for Australians to access affordable and high- quality nbn services may be negatively affected.

When this

will impact:

0-5 5-10 10-15 15+

Where this

will impact:

Changes to nbn technology will affect

service quality

The nbn was primarily designed for residential and small business users. The original (2010) plan was for fixed line Fibre to the Premises (FTTP) for the approximately 93% of users in readily-accessible locations in our fast-growing cities, regional centres and towns. The remaining 7% of the population would receive fixed wireless (fringes of our cities and towns, and close-by rural hinterland) and satellite (rural communities and remote areas, and other hard to access locations).

The FTTP focus has moved to what is now called a multi-technology mix. This different mix has altered projected infrastructure costs. For example, the need for upgrades to Hybrid Fibre Coaxial (HFC) connections under the current plan drives up capital costs and operating expenses. Figure 7 shows the different nbn technology mixes for the two approaches based on end of rollout forecasts for premises that are passed and connected (original plan) and ready to connect (current plan).

Figure 7: The nbn technology mix has changed since 2010

2010 Plan – at June 2021 Current Plan – at June 2020

93%

7%

22%

12% 41%

16%

9%

Fibre to the Premises

Fibre to the Node/Basement

Fibre to the Curb

Hybrid Fibre Coaxial

Fixed wireless and satellite

Source: nbn (2010, 2018) 89

Introduction

Future trends

Users

Industry

Transport

Social infrastructure

Energy

Water

Next steps

Executive summary

Telecommunications