¡Descarga Understanding Cost Classification and Income Statement in Manufacturing and Merchandising y más Apuntes en PDF de Contabilidad Analítica solo en Docsity!

Chapter 3 The General

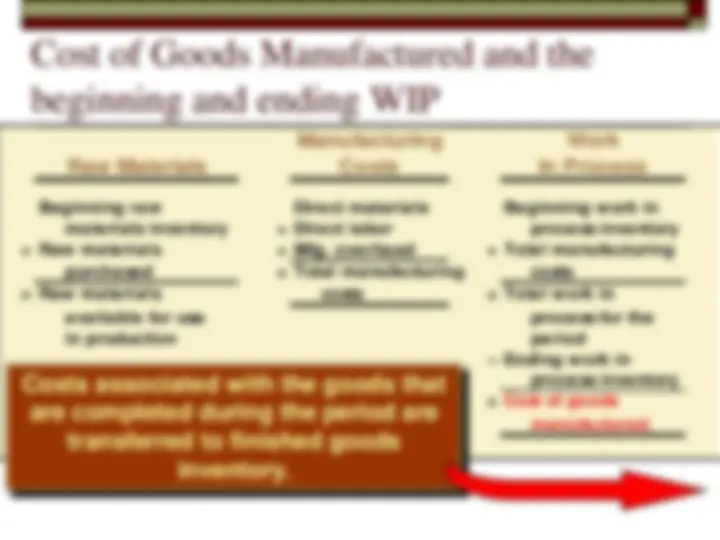

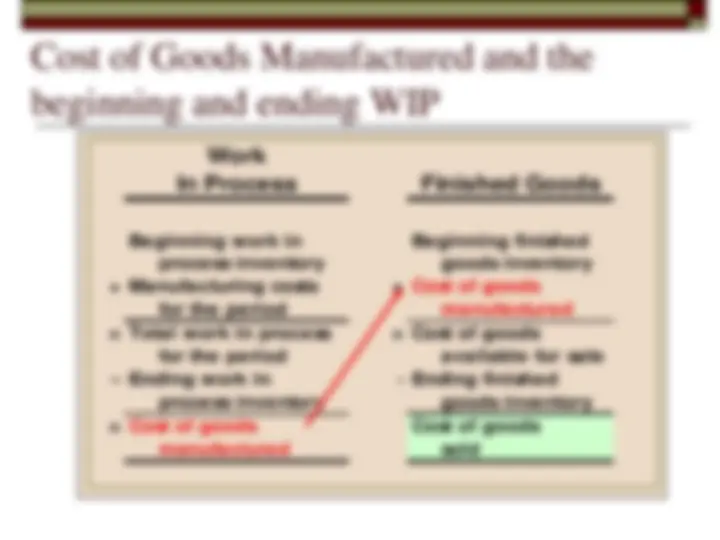

Schedule of costs

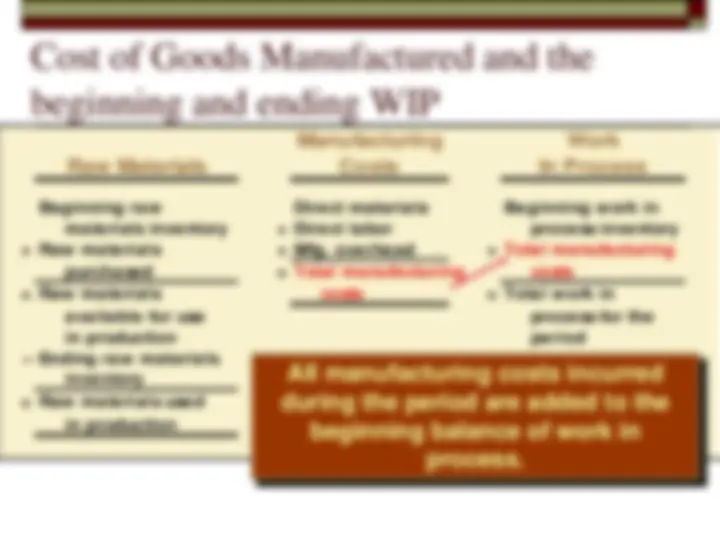

Cost classification according to business functions Manufacturing and non manufacturing costs The Income Statement The Schedule of cost of goods manufactured The begining and ending work in process The equivalent units of production

VALUE CHAIN:

To identify the major business functions that add value a company’s products or services.

These activities are generic. Each activity includes specific activities that vary by industry.

Cost classification according to business

functions.

Inbound logistics

Operations Outbound logistics

Marketing (^) Service

Administration, Procurement Reseach and Development

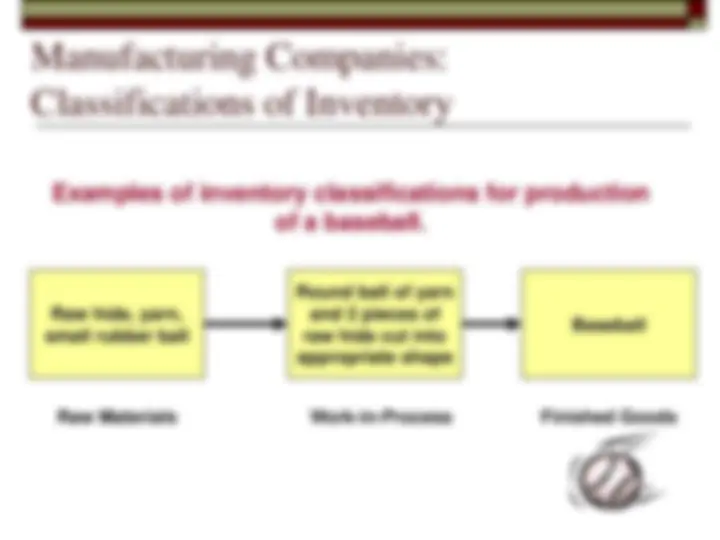

MANUFACTURING COMPANIES:

Convert raw materials into a product. The company sells the producto either to other companies or to users. Manufacturing includes restaurants and other “service type” companies, as well as automobile or clothes prodution.

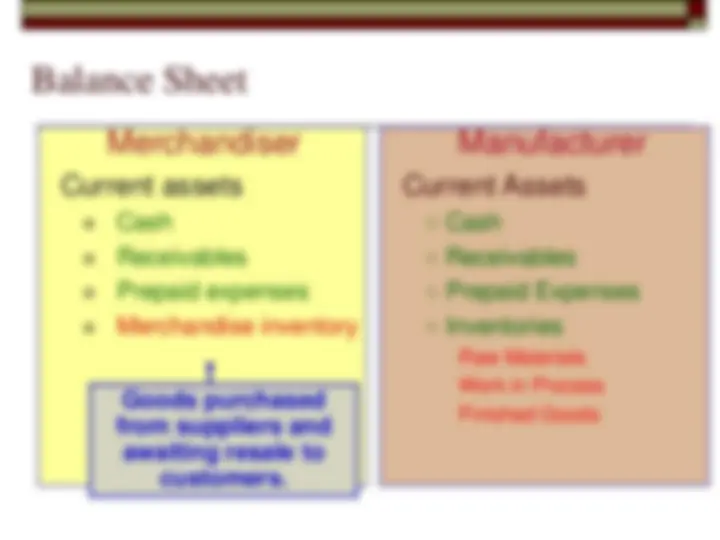

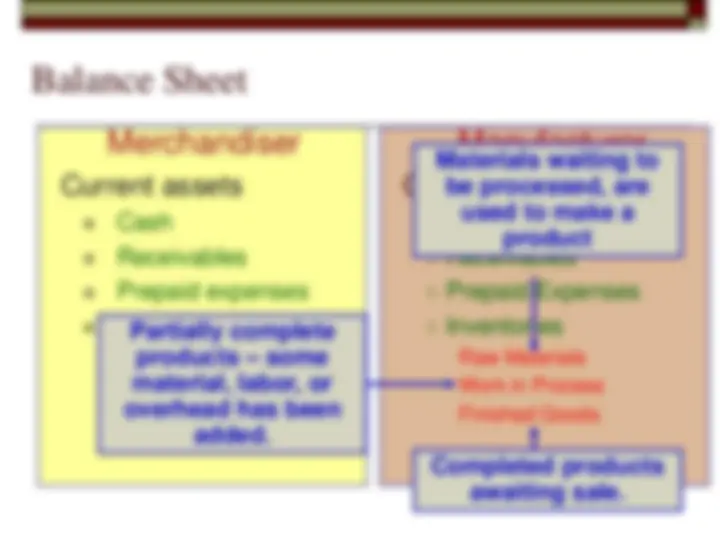

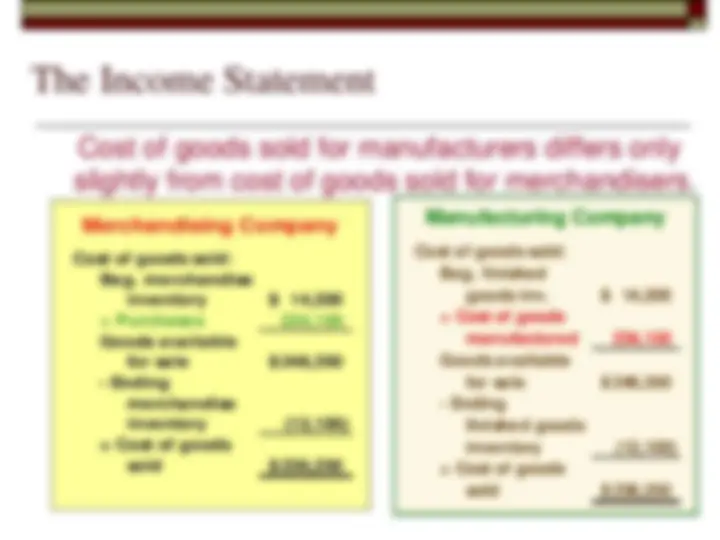

MERCHANDISING COMPANIES:

Buy finished productos and resell the products to customers. Valuing inventories is easier in a merch. Company

Cost classification according to business

functions.

• MANUFACTURING COSTS

- Inbound logistics

- Operations

• NON MANUFACTURING COSTS

- Selling costs

- Marketing costs

- Administrative costs

- Research and Development costs

Cost classification according to business

functions.

Direct Materials

Those raw materials that become an integral part of

the product and that can be conveniently traced to it.

It does not imply unprocessed natural resources.

The finished product of one company can be the raw

material of another.

Example: A radio installed in an automobile

Direct Labour

Those labour costs that can be easily traced to

individual units of product.

In some industries, sophisticated equipment is

replacing direct labor.

Example: Wages paid to automobile assembly workers

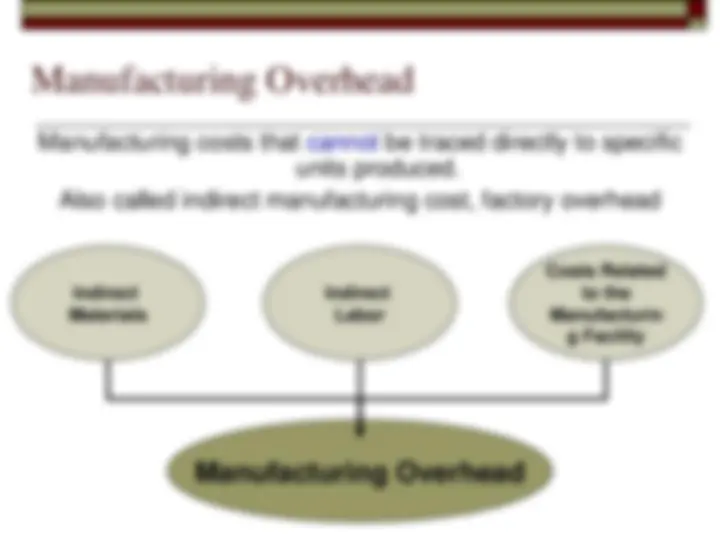

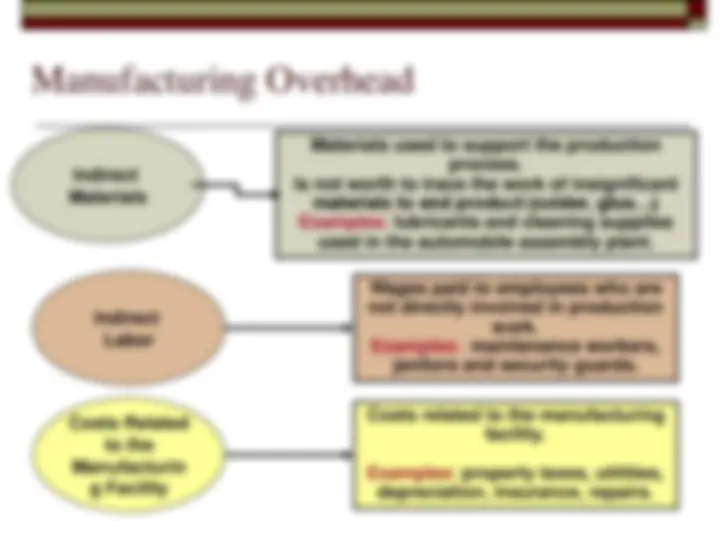

Manufacturing Overhead

Materials used to support the production process. Is not worth to trace the work of insignificant materials to end product (solder, glue…) Examples: lubricants and cleaning supplies used in the automobile assembly plant.

Indirect Materials

Wages paid to employees who are not directly involved in production work. Examples: maintenance workers, janitors and security guards.

Indirect Labor

Costs related to the manufacturing facility. Examples: property taxes, utilities, depreciation, insurance, repairs.

Costs Related to the Manufacturin g Facility

Classifications of Manufacturing Costs

Direct Material

Direct Labor

Manufacturing Overhead

Prime Cost

Conversion Cost

Manufacturing costs are often

classified as follows:

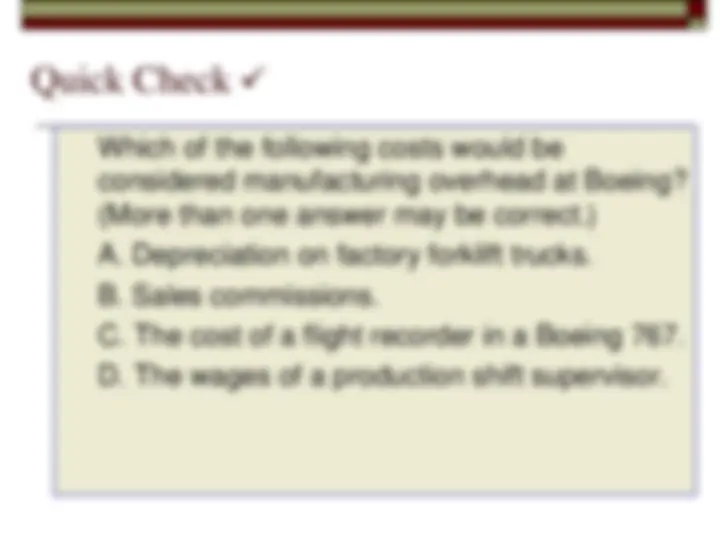

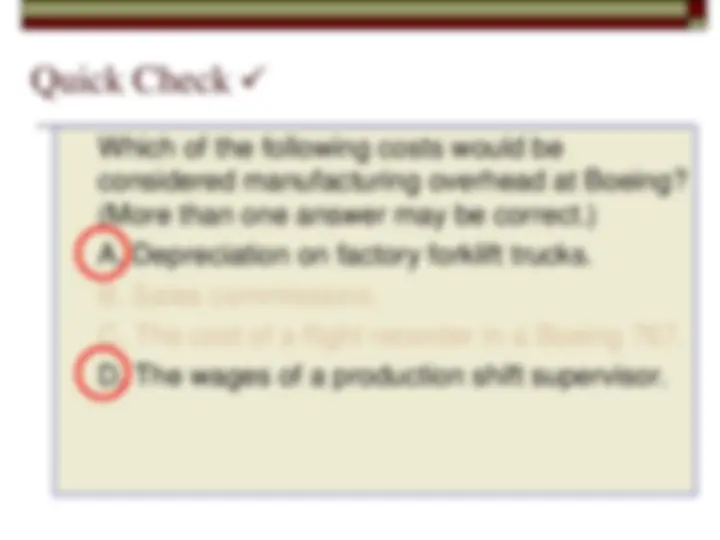

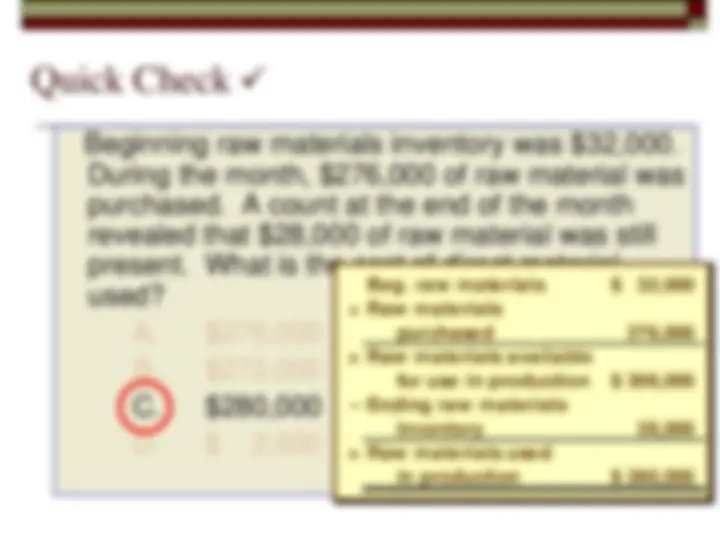

Quick Check

Which of the following costs would be

considered manufacturing overhead at Boeing?

(More than one answer may be correct.)

A. Depreciation on factory forklift trucks.

B. Sales commissions.

C. The cost of a flight recorder in a Boeing 767.

D. The wages of a production shift supervisor.

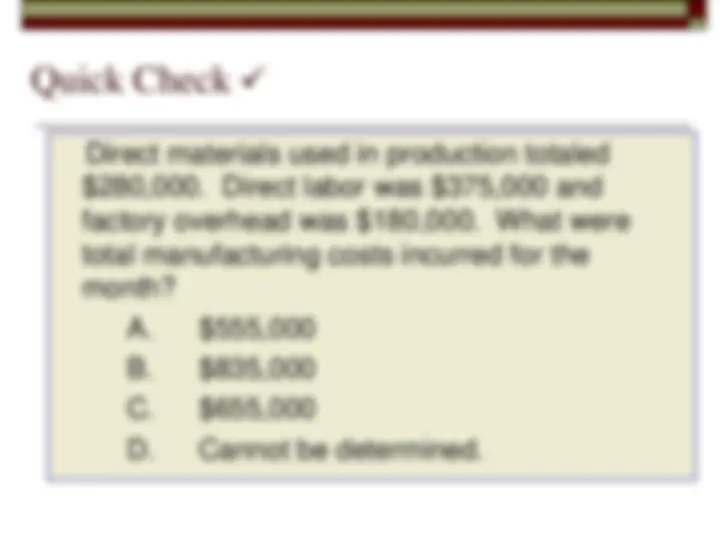

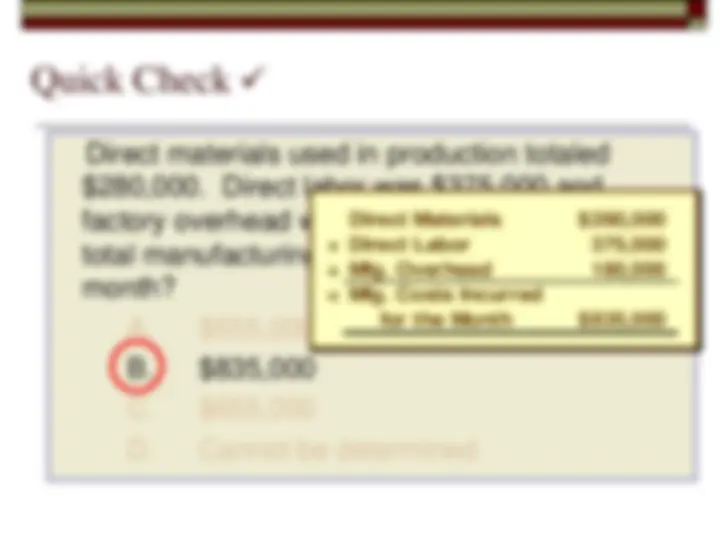

Quick Check

Which of the following costs would be

considered manufacturing overhead at Boeing?

(More than one answer may be correct.)

A. Depreciation on factory forklift trucks.

B. Sales commissions.

C. The cost of a flight recorder in a Boeing 767.

D. The wages of a production shift supervisor.

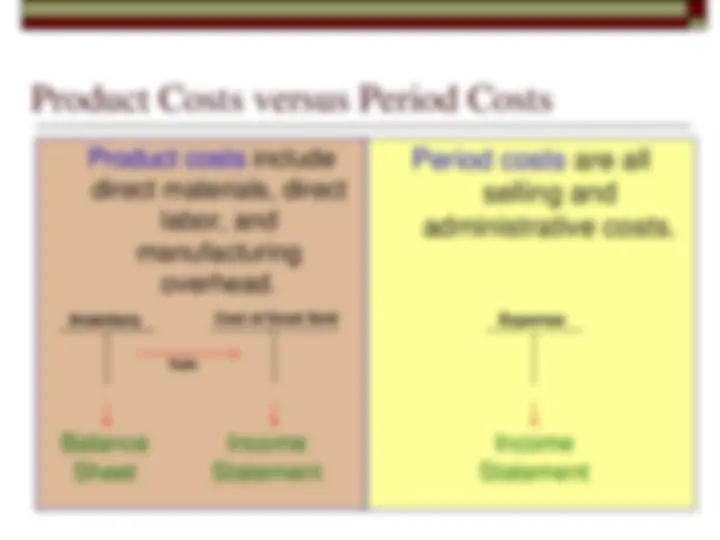

Product Costs versus Period Costs

Product costs Period costs

To understand this difference we must go to the matching principle. Based on the accrual concept, it states that costs incurred to generate a particular revenue should be recognized as expensed in the same period that the revenue is recognized.

As products will be sold, then the costs should be recognised as expense only when the sale takes place.

Product Costs versus Period Costs

Product costs are added

to units of product.

They are incurred and

not treated as expenses

until de units are sold.

Period costs are not

included in product

costs. They are

expensed on the

income statement.

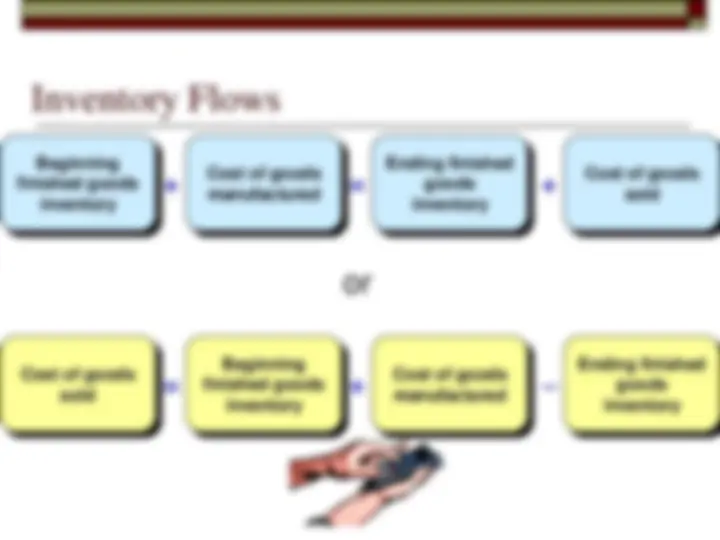

Inventory Cost of Good Sold

Balance Sheet

Income Statement

Sale

Expense

Income Statement

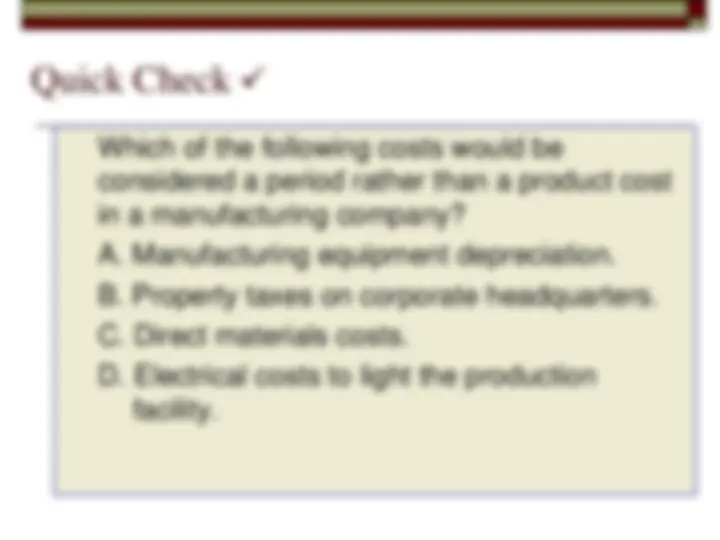

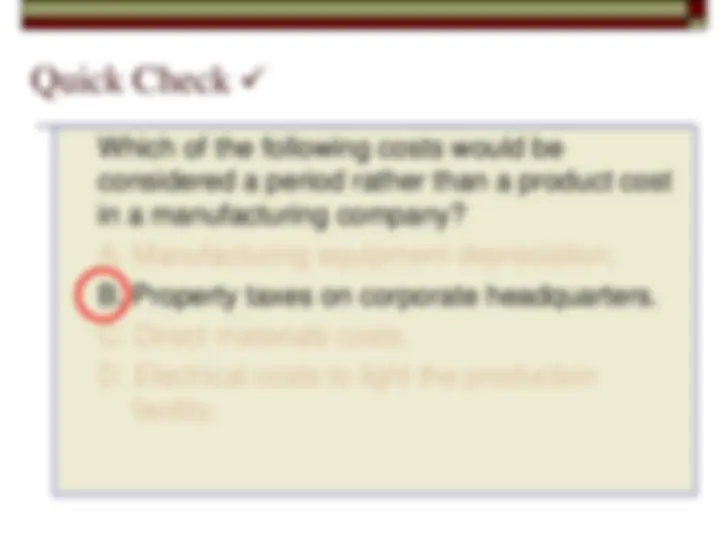

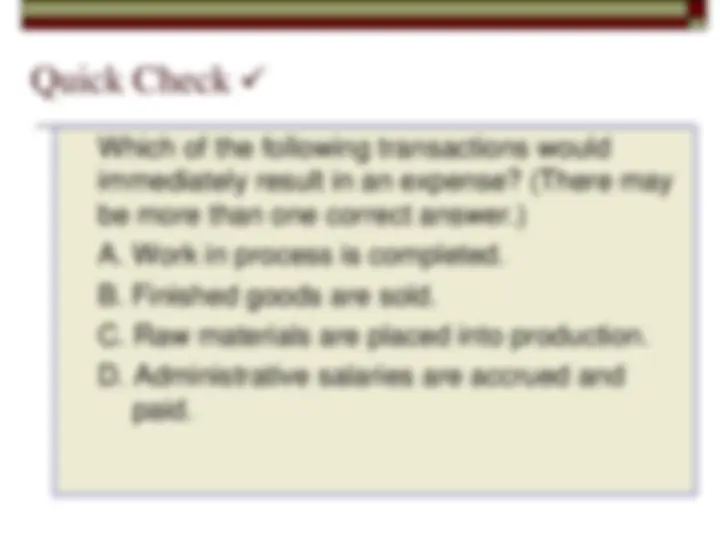

Quick Check

Which of the following costs would be

considered a period rather than a product cost

in a manufacturing company?

A. Manufacturing equipment depreciation.

B. Property taxes on corporate headquarters.

C. Direct materials costs.

D. Electrical costs to light the production

facility.

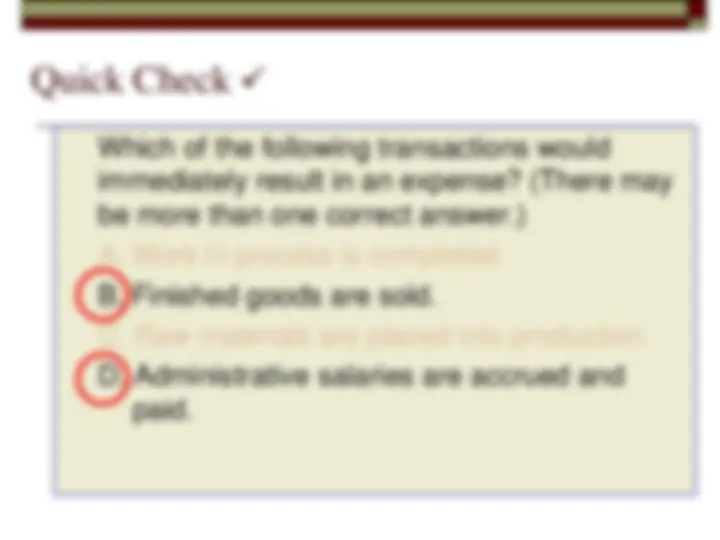

Quick Check

Which of the following costs would be

considered a period rather than a product cost

in a manufacturing company?

A. Manufacturing equipment depreciation.

B. Property taxes on corporate headquarters.

C. Direct materials costs.

D. Electrical costs to light the production

facility.