Topic 5 . Technical investments &

Investment property

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: contabilidad, Profesor: Maria Rosa Rovira, Carrera: Administració i Direcció d'Empreses, Universidad: UAB

Tipo: Apuntes

1 / 31

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Spanish General Accounting Plan, Part two, RECOGNITION AND MEASUREMENT STANDARDS

2nd Property, plant and equipment

3rd Specific standards on property, plan and equipment

4th Investment property

5th Intangible assets

6th Specific standards on intangible assets

Balance sheet classification :

Non Current Assets

Current Assets

NON-CURRENT ASSETS

I. Intangible assets II. Property, plant and equipment

III. Investment property

requirements for recognition in the balance sheet:

IV. Non-current investments in group companies and associates V. Non-current investments VI. Deferred tax assets

Key definitions

Intangible asset: an identifiable asset without physical substance.

An asset is a resource that is controlled by the entity as a result of past events (for example, purchase or self-creation) and from which future economic benefits (inflows of cash or other assets) are expected.

Thus, the three critical attributes of an intangible asset are:

Identifiability: an intangible asset is identifiable when it:

is separable (capable of being separated and sold, transferred, licensed, rented, or exchanged, either individually or together with a related contract) or

arises from contractual or other legal rights, regardless of whether those rights are transferable or separable from the entity or from other rights and obligations.

If an intangible item does not meet the above requirements will be recorded as an expense.

RECOGNITION AND MEASUREMENT STANDARDS

5th Intangible assets The criteria set out in the standards on property, plant and equipment shall be applied to intangible assets. Nonetheless, the specific standards on intangible assets set out below and the criteria applicable to goodwill in the standard on business combinations shall also apply.

6th Specific standards on intangible assets

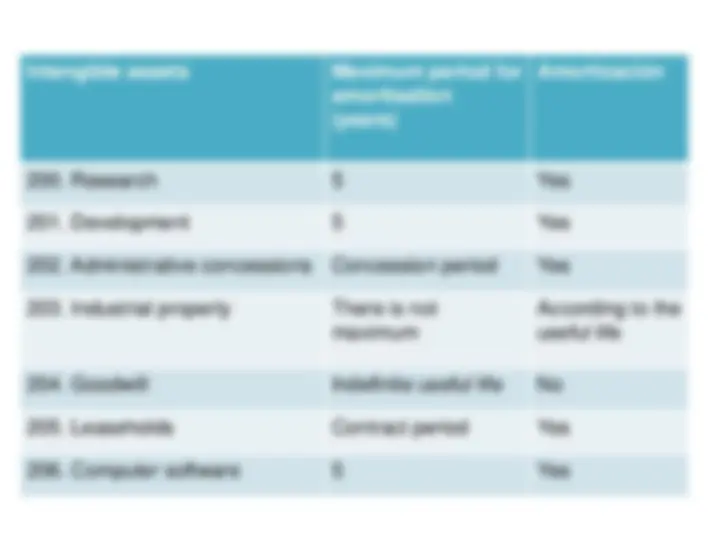

Research Value applied in the original and planned research that seeks to discover new knowledge, skills or improve existing ones.

Research costs shall be recognised as an expense in the reporting period in which they are incurred.

However, they may be capitalised as intangible assets provided that they meet the following conditions:

Capitalised research costs shall be amortised over their useful life and, in any event, within a five-year period. Where there is reasonable doubt as to the technical success and economic and commercial feasibility of the project, any amounts capitalised shall be recognised directly in losses for the reporting period.

Administrative concessions Expenditure made to obtain research or operating rights extended by the Spanish government or by other public entities, or the price of acquiring transferrable concessions.

Industrial property Amount paid for ownership or the right to use or the concession to use different types of industrial property, in cases where, on the basis of the contract conditions, they are to be included in assets of the acquiring company. This includes, among others, invention patents, certificates protecting public utility models and patents of importation.

This account shall also include expenditure on development when the projects undertaken by the company have yielded positive results and, in compliance with the pertinent legal provisions, these results have been filed at the corresponding registry.

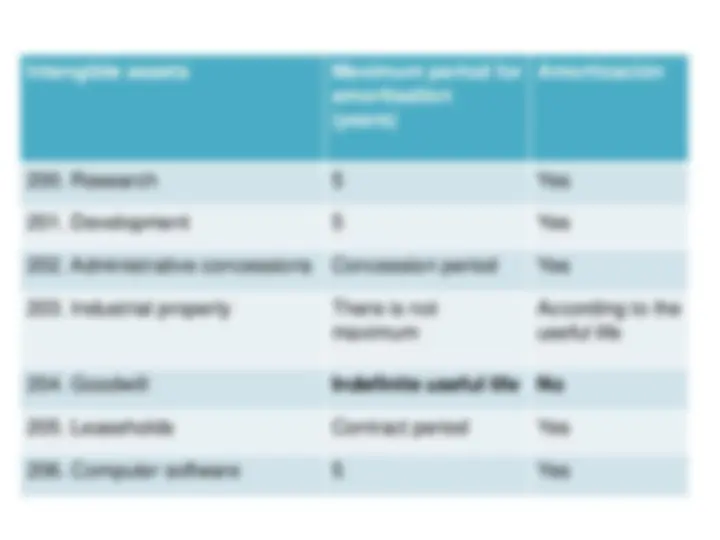

Goodwill The excess, at the acquisition date, of the cost of a business combination over the value of the identifiable assets acquired less the value of the identifiable liabilities assumed.

Consequently, goodwill shall only be recognised when it has been acquired onerously and when it represents future economic benefits that will flow from assets that cannot be identified individually and recognised separately.

Goodwill shall not be amortised. It’s supposed to have no finite (or infinite) useful live

Leaseholds Amount paid for rights to lease premises, whereby the acquiree/new lessee assumes the rights and obligations of the transferor/former lessee that are set out in an earlier contract.

Useful life of an intangible asset

The company shall assess whether the useful life of an intangible asset is finite or indefinite.

An intangible asset shall be considered to have an indefinite useful life when, based on an analysis of all of the relevant factors, there is no foreseeable limit to the period over which the asset is expected to generate net cash inflows for the company.

An intangible asset with an indefinite useful life shall not be amortised. Rather, it shall be tested for impairment when there is an indication that the asset might be impaired, and at least annually.

The useful life of an intangible asset that is not being amortised shall be reviewed in each reporting period to determine whether events and circumstances continue to support an indefinite useful life assessment for that asset. If this is not the case, the change in the assessment of the useful life from indefinite to finite shall be accounted for as a change in accounting estimate, except where the change is due to error.

Intangible assets Maximum period for amortisation (years)

Amortización

According to the useful life

can be acquired :

RECOGNITION AND MEASUREMENT STANDARDS

2nd Property, plant and equipment

3rd Specific standards on property, plan and equipment

4th Investment property The criteria set out in the standards on property, plant and equipment shall be applied to investment property.

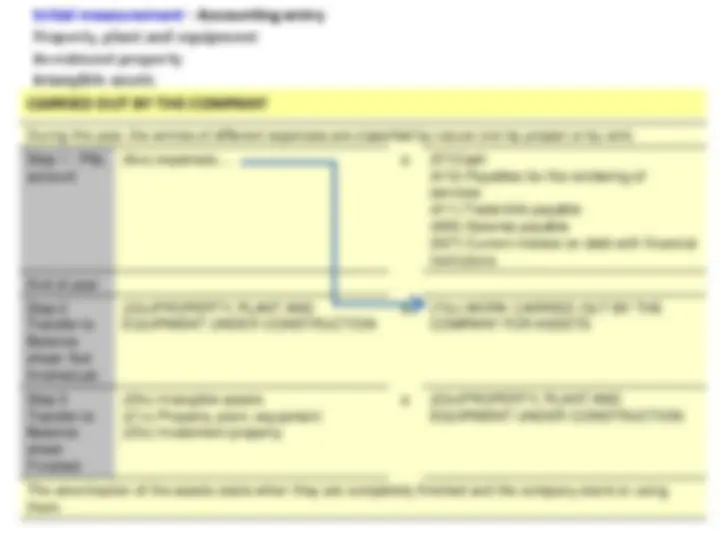

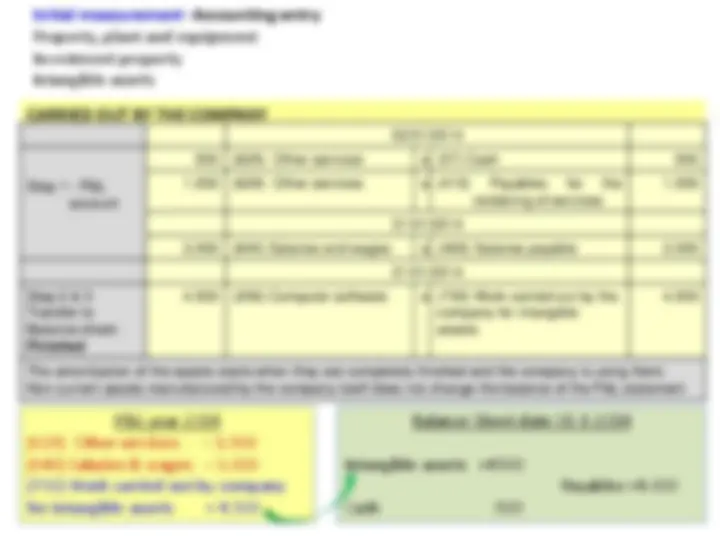

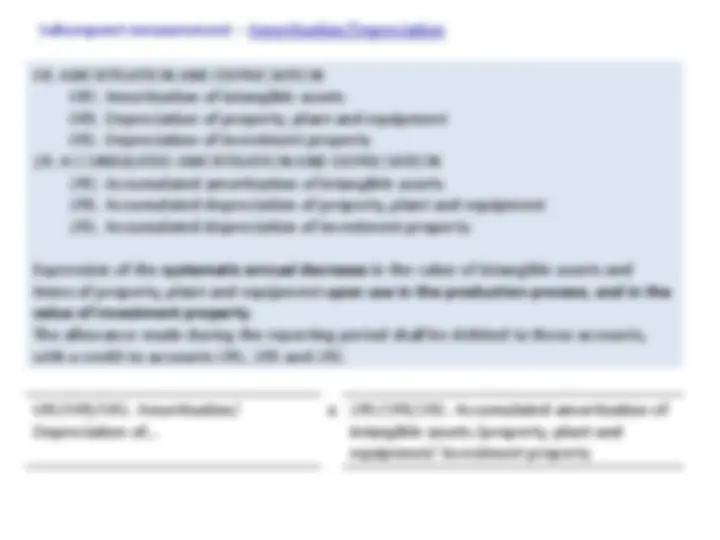

Initial measurement - Accounting entry Property, plant and equipment Investment property Intangible assets

(20x) Intangible assets

(21x) Property, plant, equipment

(22x) Investment property

a (57)Cash

(170) Non-current payables with financial entities (520) Current payables with financial entities

(173) Non-current payables to suppliers of fixed assets (523) Current payables to suppliers of fixed assets

(175) Non-current bills payable (525) Current bills payable

(527) Current interest on debt with financial institutions (528) Current interest on payables

EXTERNALLY BOUGHT

RECOGNITION AND MEASUREMENT STANDARDS

1. Initial measurement: cost Cost: externally bought: purchase price or carried out by the company: production cost

Production cost

the purchase price of raw materials and consumables,

other directly related costs

the proportional amount of costs indirectly attributable to the items in question, insofar as these relate to the production, construction or manufacturing period and are required to bring the asset into operating condition.

the cost of inventories shall be determined using the applicable general criteria.