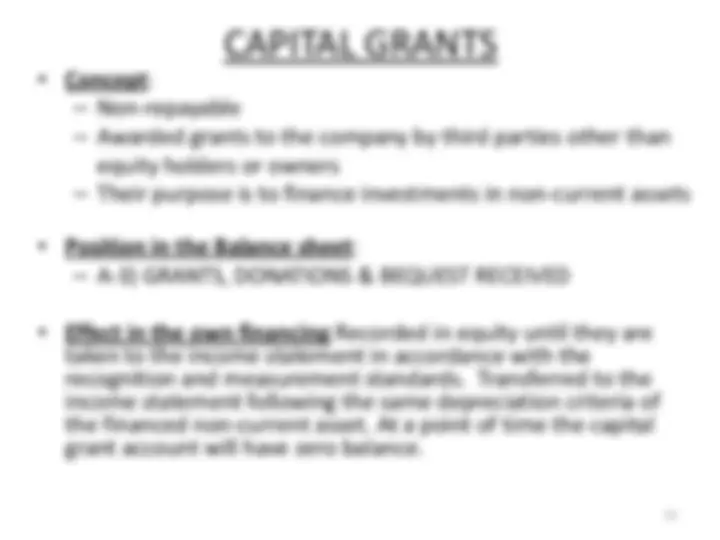

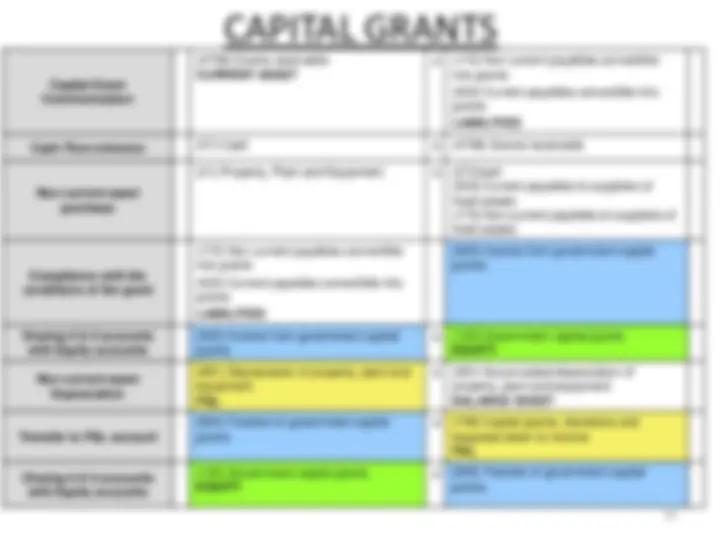

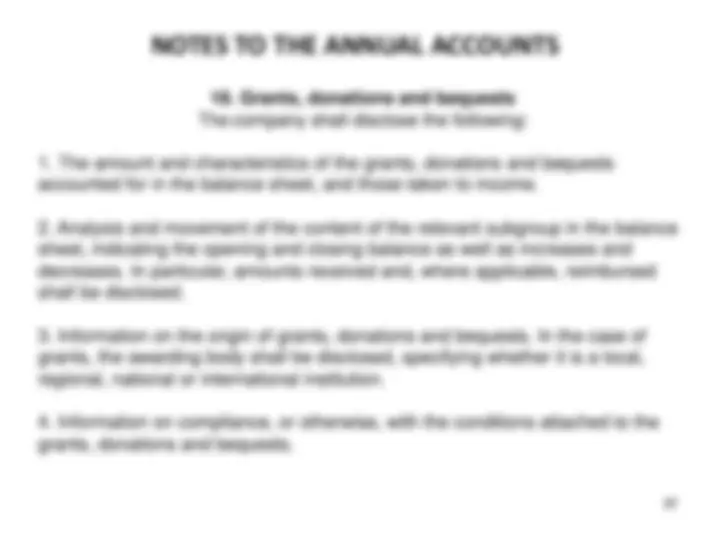

Topic 2. OWN FUNDING

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Financial Accounting, Profesor: Maria Rosa Rovira, Carrera: Administració i Direcció d'Empreses - Anglès, Universidad: UAB

Tipo: Apuntes

1 / 38

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

They have no fixed repayment date, so the owners

contributions are considered indefinite.

They are considered the guarantee of payment of

the debts of the company.

5

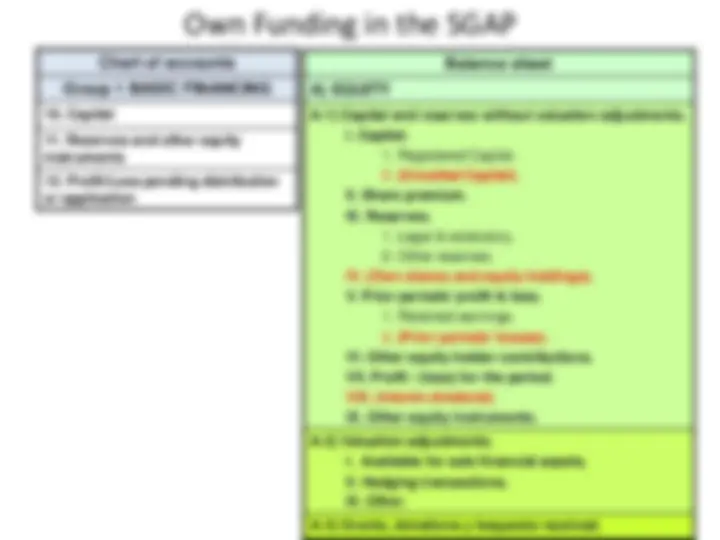

Own Funding in the SGAP

A-1) Capital and reserves without valuation adjustments. I. Capital.

**10. Capital

CAPITAL

Accounts:

100. Share capital: for profit companies 101. Assigned capital: not for profit entities 102. Capital: individual firms

(Number of shares x nominal value)

THE SHARE CAPITAL

Chart of accounts:

100 Share capital (number of shares x nominal value)

190 Shares issued

192 Subscribed shares

194 Issued capital pending regstration

103 Uncalled capital

1030 Uncalled capital

1034 Uncalled capital, pending registration

104 Uncalled non-monetary contributions

1040 Uncalled non-monetary contributions, capital

1044 Uncalled non-monetary contributions, capital pending registration

558 Receivable on called-up-capital

THE SHARE CAPITAL

Types of foundation of the Spanish Sociedad anónima S.A .:

time) take place the issuing shares, subscription and payment (at

least 25% of the nominal value of the shares).

THE SHARE CAPITAL

Initial contribution in the company’s creation

THE SHARE CAPITAL

SIMULTANEOUS FOUNDATION

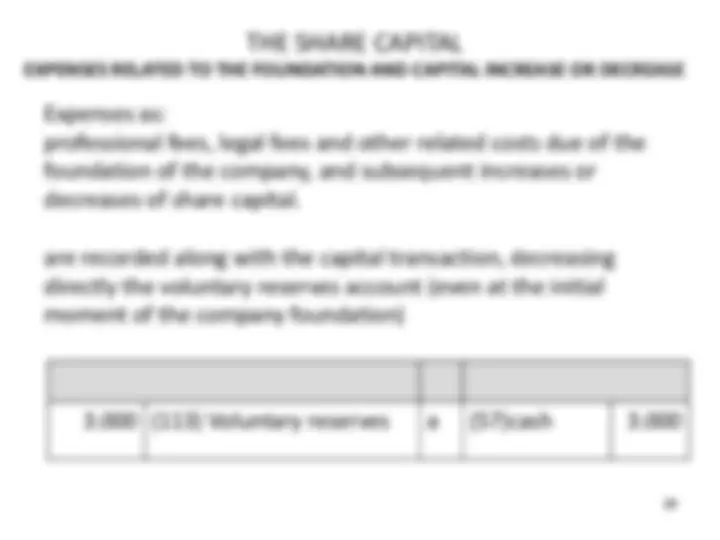

Expenses as:

professional fees, legal fees and other related costs due of the

foundation of the company, and subsequent increases or

decreases of share capital.

are recorded along with the capital transaction, decreasing

directly the voluntary reserves account (even at the initial

moment of the company foundation)

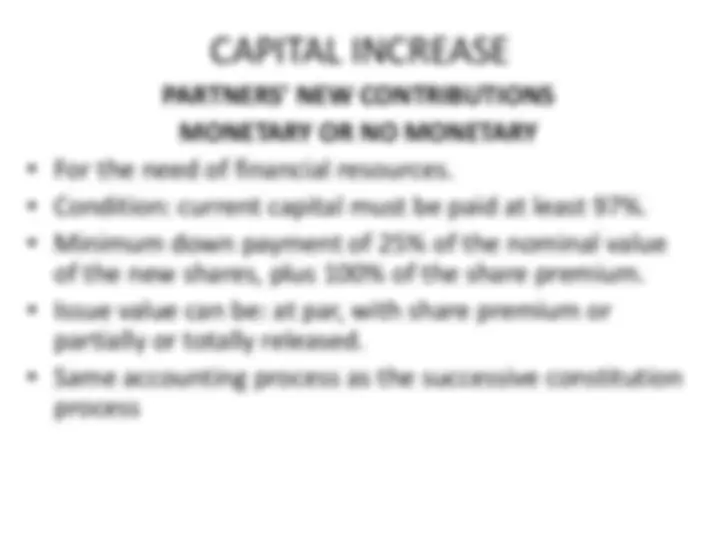

THE SHARE CAPITAL

EXPENSES RELATED TO THE FOUNDATION AND CAPITAL INCREASE OR DECREASE

3.000 (113) Voluntary reserves a (57)cash 3.

THE SHARE CAPITAL

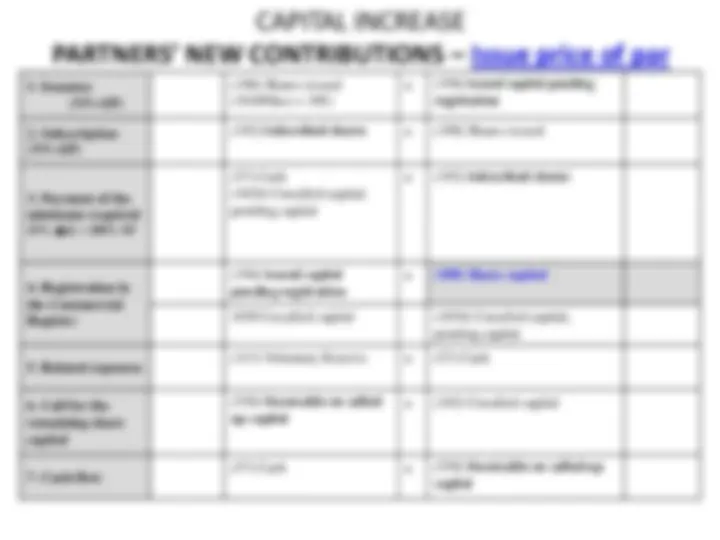

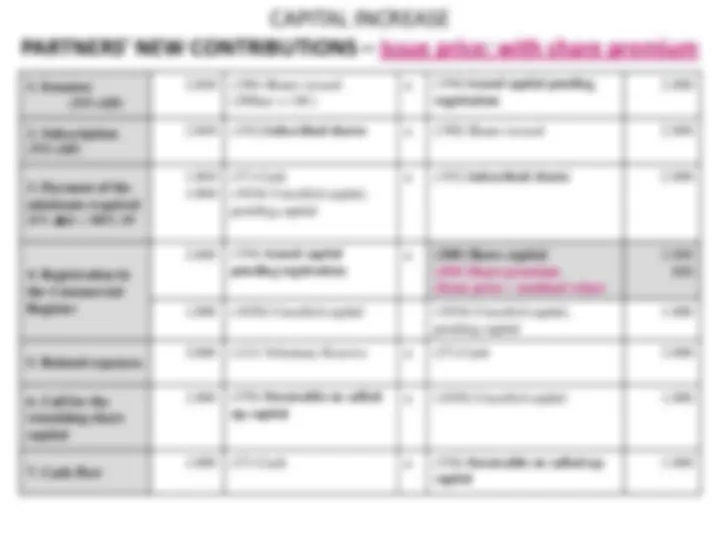

SUCCESSIVE CONSTITUTION

1. Issuance (Issue price: NV+SP)

100.000 (190) Shares issued (10.000acc x 10€)

a (194)^ Issued capital pending registration

2. Subscription (Issue price: NV+SP)

100.000 (192) Subscribed shares a (190) Shares issued 100.

3. Payment of the minimum required 25% K + 100% SP

(57) Cash (1034) Uncalled capital, pending registration

a 100.

4. Registration in the Commercial Register

100.000 (194) Issued capital pending registration

a (100) Share capital 100.

75.000 1030 Uncalled capital (1034) Uncalled capital, pending registration

THE SHARE CAPITAL

SUCCESSIVE CONSTITUTION

5. Related expenses

3.000 (113) Voluntary Reserve a (57) Cash 3.

6. Call for the remaining share capital

75.000 (558)^ Receivable on called-up- capital

a (103) Uncalled capital 75.

7. Cash-flow

75.000 (57) Cash a (558) Receivable on called-up- capital

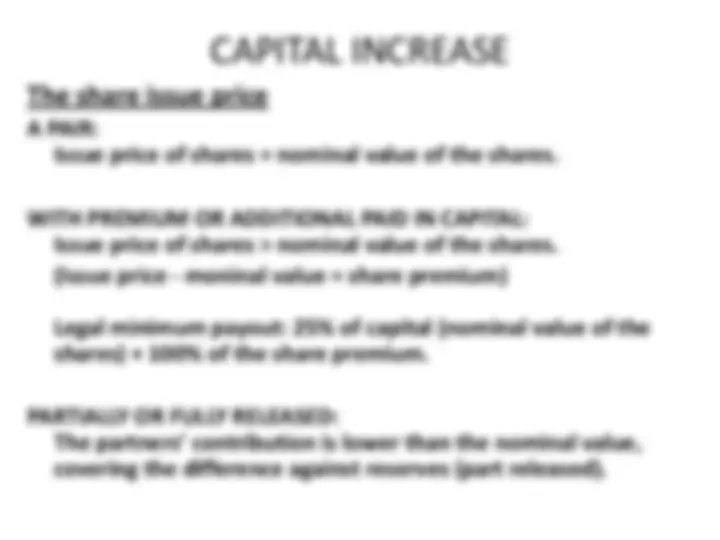

A PAIR:

Issue price of shares = nominal value of the shares.

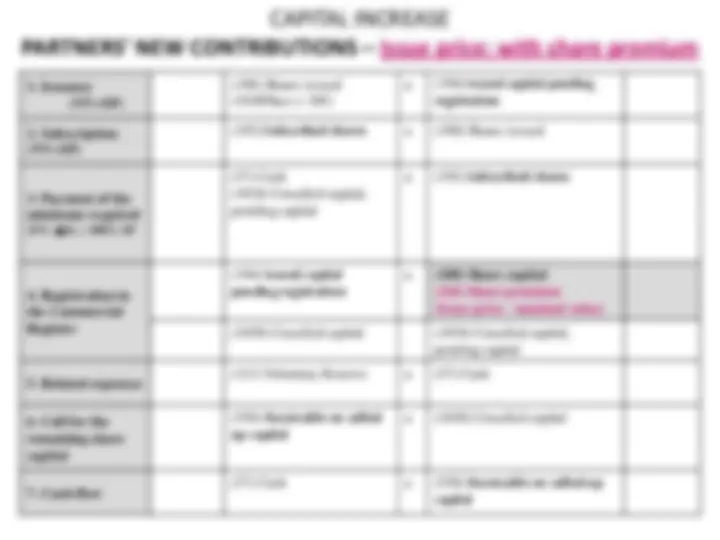

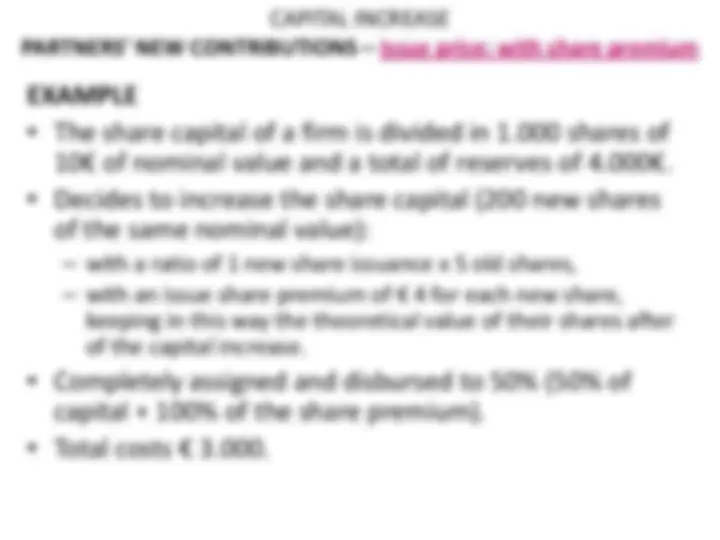

WITH PREMIUM OR ADDITIONAL PAID IN CAPITAL:

Issue price of shares > nominal value of the shares.

(Issue price - moninal value = share premium)

Legal minimum payout: 25% of capital (nominal value of the

shares) + 100% of the share premium.

PARTIALLY OR FULLY RELEASED:

The partners’ contribution is lower than the nominal value,

covering the difference against reserves (part released).