1

CORPORATE TAXATION

CLASS PRESENTATIONS

Unit 1. Basic Concepts. The Principles of Taxation.

Unit 2. Personal Income Tax.

Unit 3. Corporate Income Tax

Unit 4. Value Added Tax

Unit 5. Tax Harmonization in the EU

Carlos Garcimartín

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: tax, Profesor: , Carrera: Business Administration and Management, Universidad: URJC

Tipo: Apuntes

1 / 35

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Unit 1. Basic Concepts. The Principles of Taxation.

Unit 2. Personal Income Tax.

Unit 3. Corporate Income Tax

Unit 4. Value Added Tax

Unit 5. Tax Harmonization in the EU

Carlos Garcimartín

BASIC CONCEPTS: THE PRINCIPLES OF TAXATION

2 2

2.2 The concept of progressivity

2.3. The concept of redistribution

K t

t RS −

= 1

Taxpayers

Tax Base

Main characteristics of dual schemes:

Pros:

Cons:

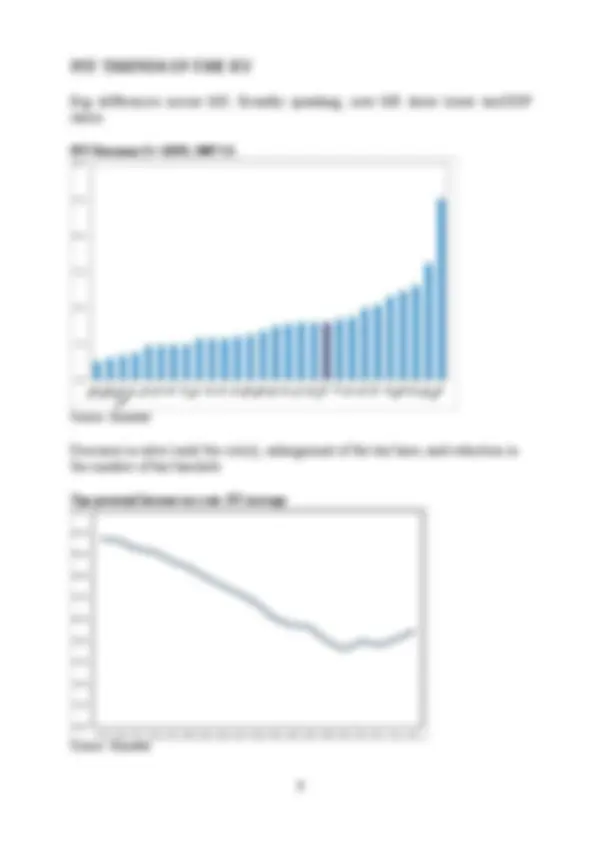

Big differences across MS. Broadly speaking, new MS show lower tax/GDP ratios

PIT Revenue (% GDP). 2007/

Source: Eurostat

Decrease in rates (until the crisis), enlargement of the tax base, and reduction in the number of tax brackets

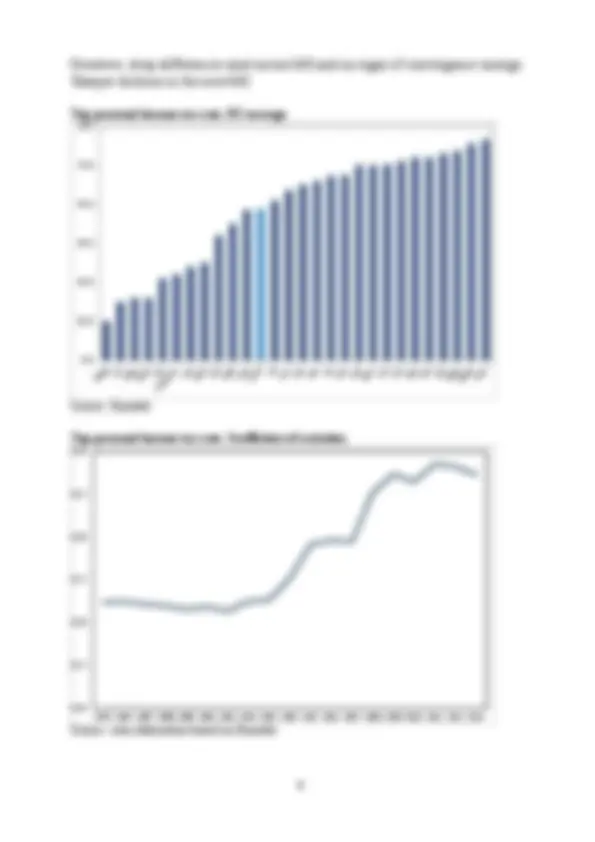

Top personal income tax rate. EU average

Source: Eurostat

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Flat taxes in the new MS and dualisation in the old MS

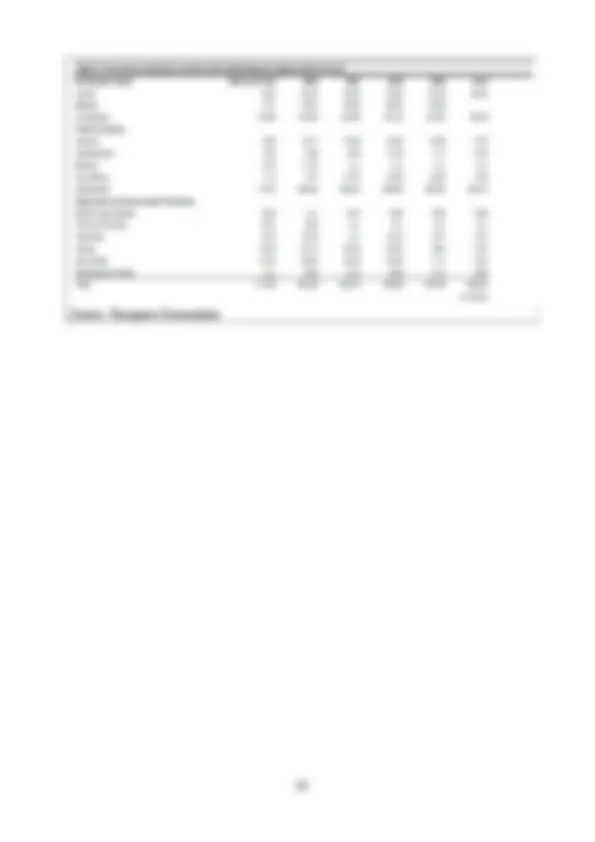

PIT in EU Countries Country PIT Type Austria Comprehensive and progressive with some dualisation Belgium Different categories of income subject to different rates. 25% withholding tax rate for most interest income Bulgaria Flat tax Cyprus Progressive rate structure. Capital income is mostly exempt Czech. Rep Flat tax Denmark Comprehensive and progressive Estonia Flat tax Finland Dual system France Comprehensive and progressive, but some types of capital income is taxed at flat rates Germany Semi-dual system UK Comprehensive and progressive, but some types of capital income is taxed at flat rates Greece Different rate structures are applied to different types of income Hungary Flat tax Ireland Semi-dual system Italy Semi-dual system Latvia Flat tax Lithuania Flat tax Luxembourg Comprehensive and progressive with some dualisation Malta Comprehensive and progressive with some dualisation The Netherlands Semi-dual system Poland Semi-dual system Portugal Comprehensive and progressive Romania Flat Tax Slovakia Flat Tax Slovenia Semi-dual system Spain Semi-dual system Sweden Dual System

From profits to the tax base

Tax rate Progressive?

Tax deductions and benefits Cost and rationale

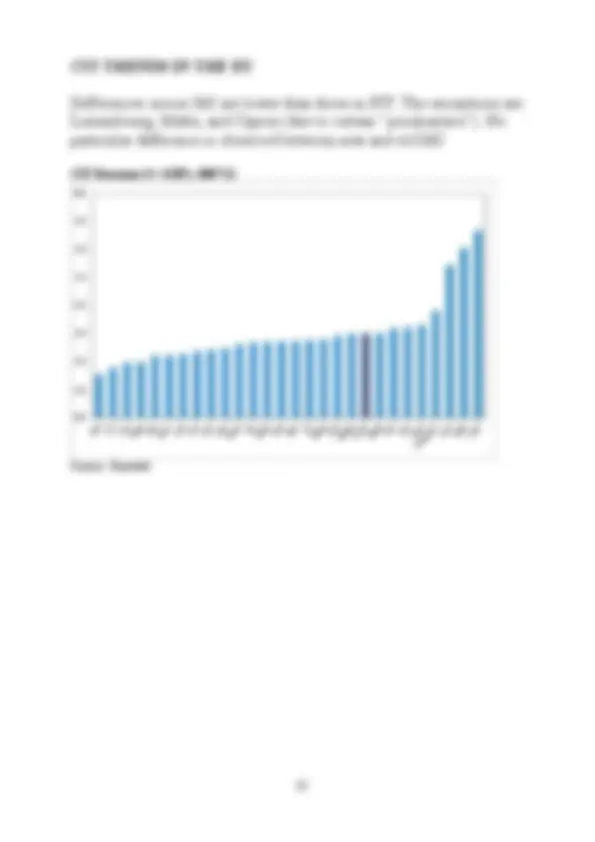

Differences across MS are lower than those in PIT. The exceptions are Luxembourg, Malta, and Cyprus (due to certain “peculiarities”). No particular difference is observed between new and old MS

CIT Revenue (% GDP). 2007/

Source: Eurostat

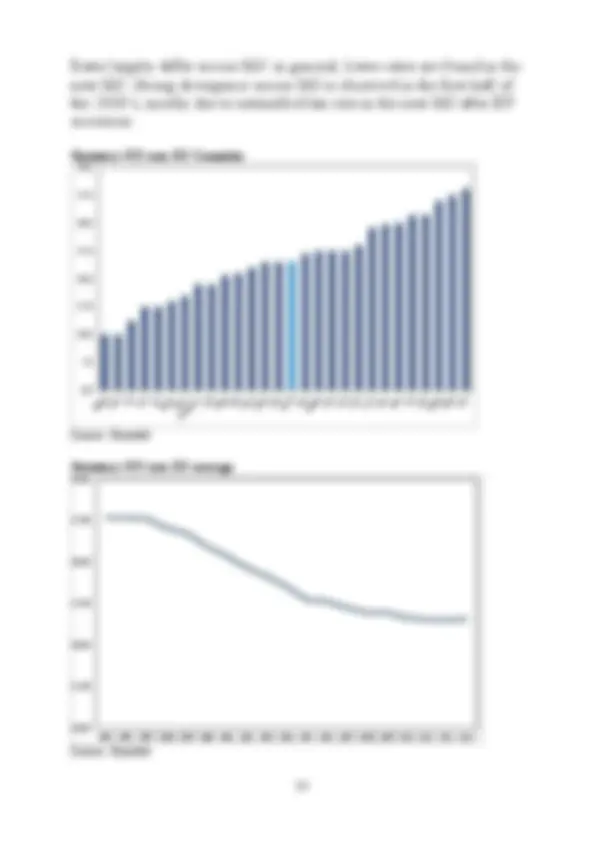

Rates largely differ across MS: in general, lower rates are found in the new MS. Strong divergence across MS is observed in the first half of the 2000’s, mostly due to intensified tax cuts in the new MS after EU accession

Statutory CIT rate. EU Countries

Source: Eurostat

Statutory CIT rate. EU average

Source: Eurostat

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Main characteristics of the VAT

Main pros of the VAT:

Taxes on final consumption would also show some of these advantages, but drawing the distinction between wholesale and retail sales is difficult in practice

Main cons:

Uniform vs. differentiated VAT rates

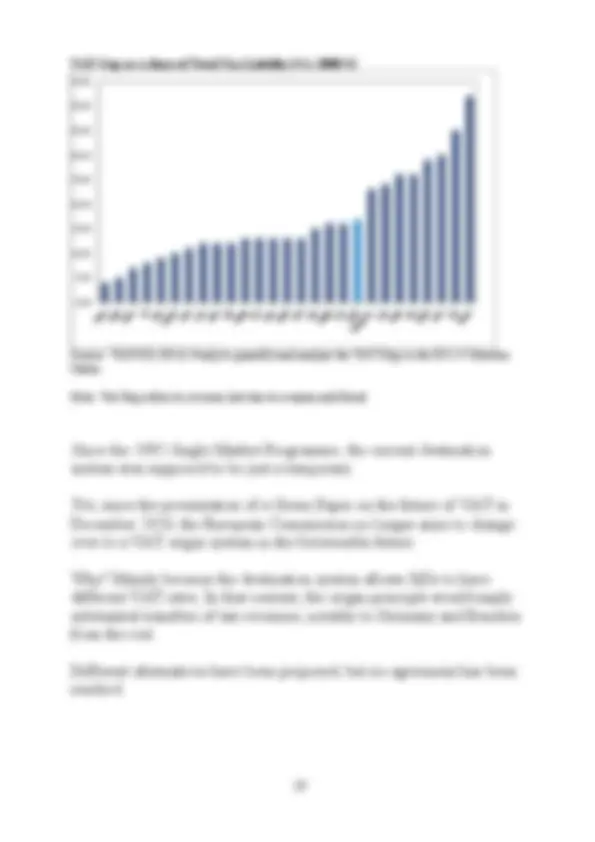

Shares of tax base subject to different rates

Source: TAXUD (2011): “A retrospective evaluation of elements of the EU VAT system”

VAT revenue across MS is more homogenous than that of PIT and CIT. However, the contribution of VAT to total revenue tends to be higher in new MS

VAT Revenue (% GDP). 2007/

Source: Eurostat

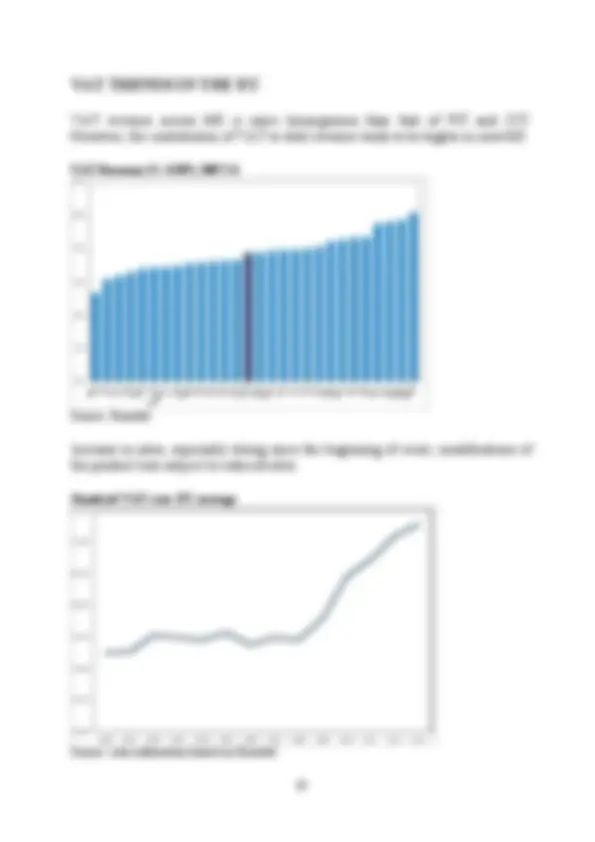

Increase in rates, especially strong since the beginning of crisis; modifications of the product lists subject to reduced rates

Standard VAT rate. EU average

Source: own elaboration based on Eurostat

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Although deep differences exist across MS, there is a clear trend towards convergence (conversely to CIT and PIT rates)

Standard VAT rate. EU Countries

Source: Eurostat

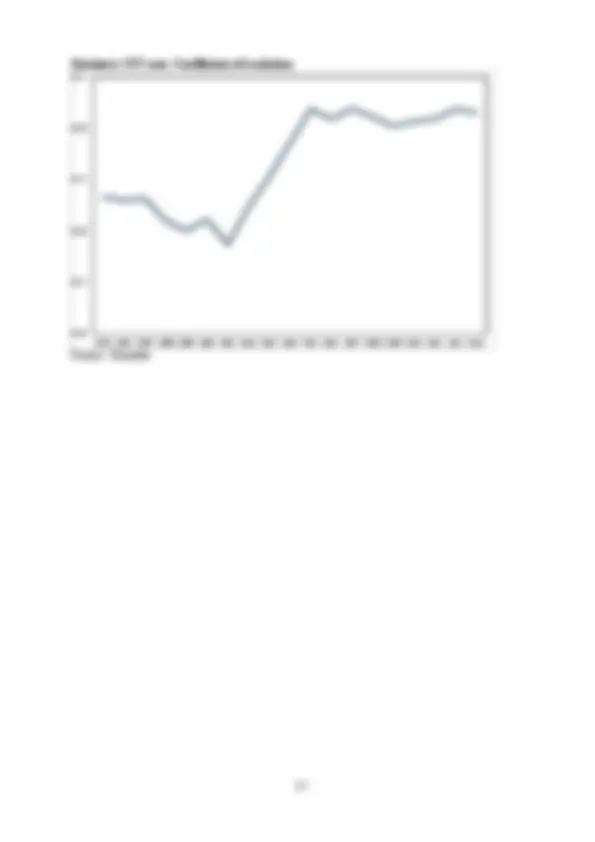

Standard VAT rate. Coefficient of variation

Source: own elaboration based on Eurostat

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013