Corporate Finance

Chapter 1: Investment Decisions

Albert Banal-Estanol

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

An introduction to corporate finance, focusing on project selection and evaluation. Topics covered include computing earnings and free cash flows, net working capital requirements, and various methods for evaluating projects such as net present value, internal rate of return, and payback period. The document also discusses the importance of adjusting for risk when evaluating projects and estimating a firm's cost of capital.

Tipo: Diapositivas

1 / 42

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Corporate Finance - Chapter 1

In this chapter…

Compute projects’ cash flows

Corporate Finance - Chapter 1

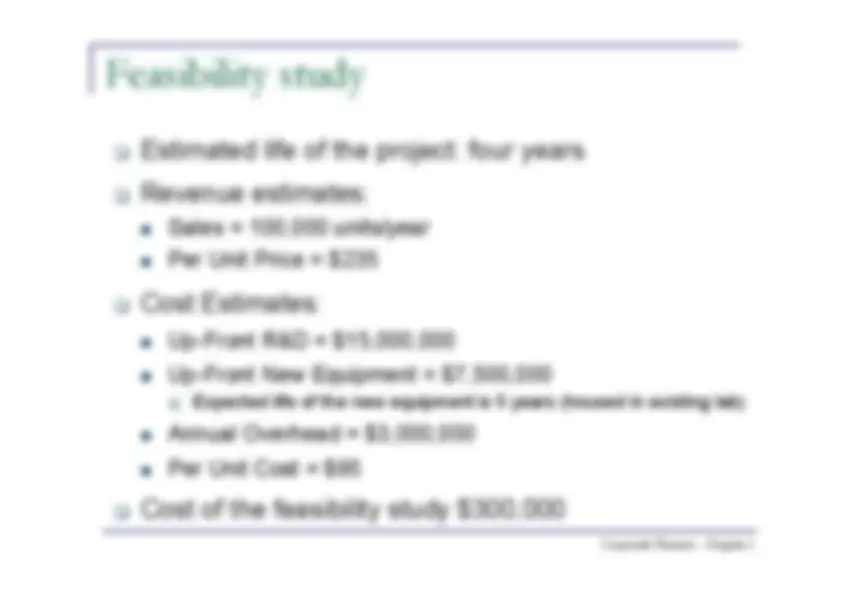

Feasibility study

Estimated life of the project: four years

Revenue estimates:

Sales = 100,000 units/year

Per Unit Price = $

Cost Estimates:

Up-Front R&D = $15,000,

Up-Front New Equipment = $7,500,000^

Expected life of the new equipment is 5 years (housed in existing lab)

Annual Overhead = $3,000,

Per Unit Cost = $

Cost of the feasibility study $300,

Corporate Finance - Chapter 1

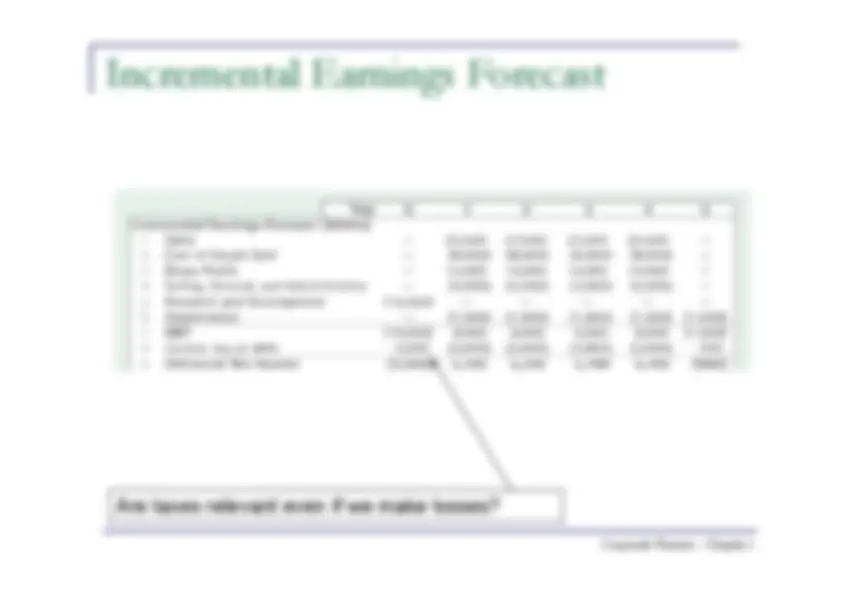

Incremental Earnings Forecast

Are taxes relevant even if we make losses?

Corporate Finance - Chapter 1

From Earnings to Cash Flows

Outflow Inflow

Corporate Finance - Chapter 1

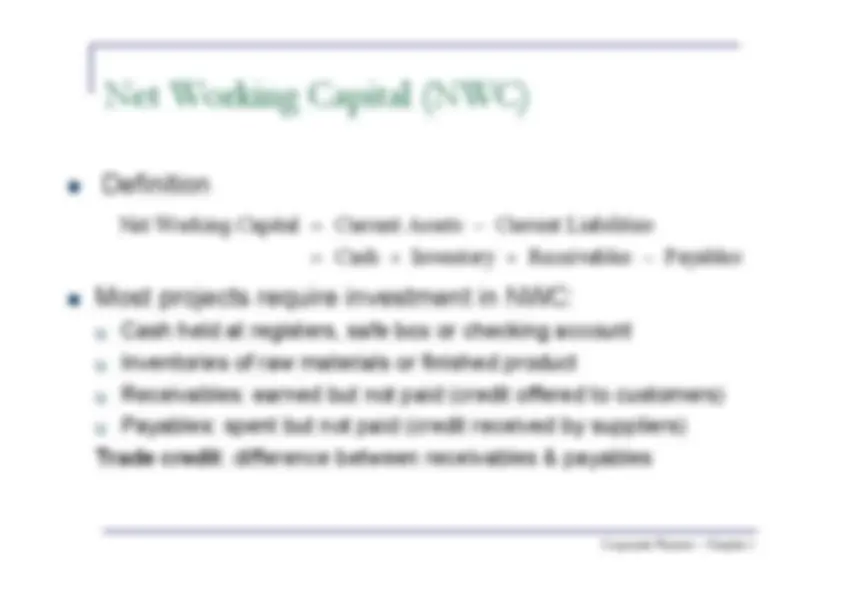

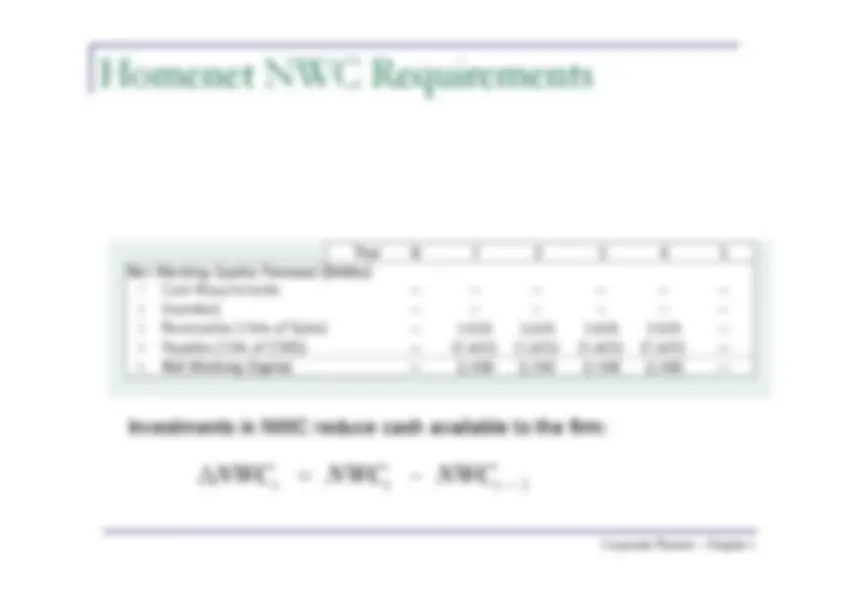

Net Working Capital (NWC)

Definition

Most projects require investment in NWC:

Cash held at registers, safe box or checking account

Inventories of raw materials or finished product

Receivables: earned but not paid (credit offered to customers)

Payables: spent but not paid (credit received by suppliers)

Trade credit

: difference between receivables & payables

Net Working Capital

Current Assets

Current Liabilities

Cash

Inventory

Receivables

Payables

Corporate Finance - Chapter 1

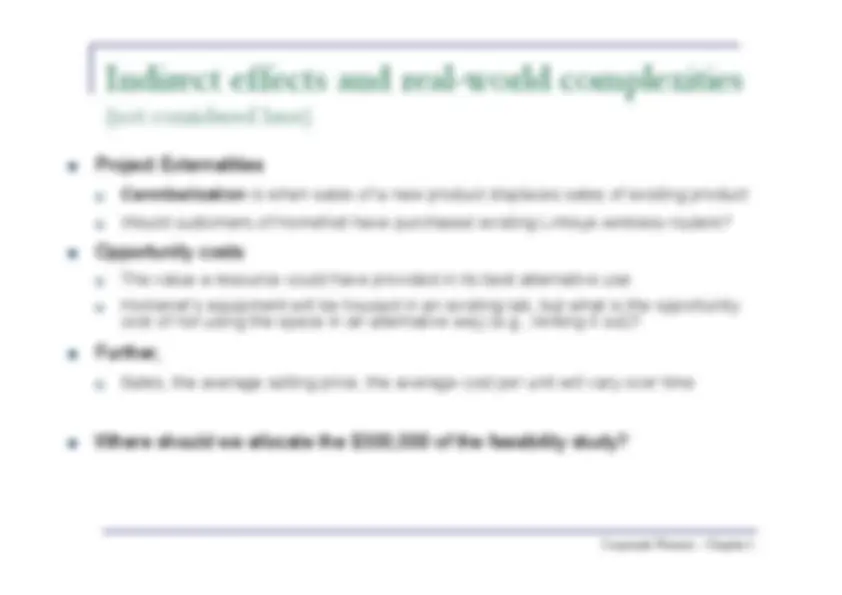

Indirect effects and real-world complexities(not considered here)

Project Externalities

Cannibalization

is when sales of a new product displaces sales of existing product

Would customers of HomeNet have purchased existing Linksys wireless routers?

Opportunity costs

The value a resource could have provided in its best alternative use

Homenet’s equipment will be housed in an existing lab, but what is the opportunitycost of not using the space in an alternative way (e.g., renting it out)?

Further,

Sales, the average selling price, the average cost per unit will vary over time

Where should we allocate the $300,000 of the feasibility study?

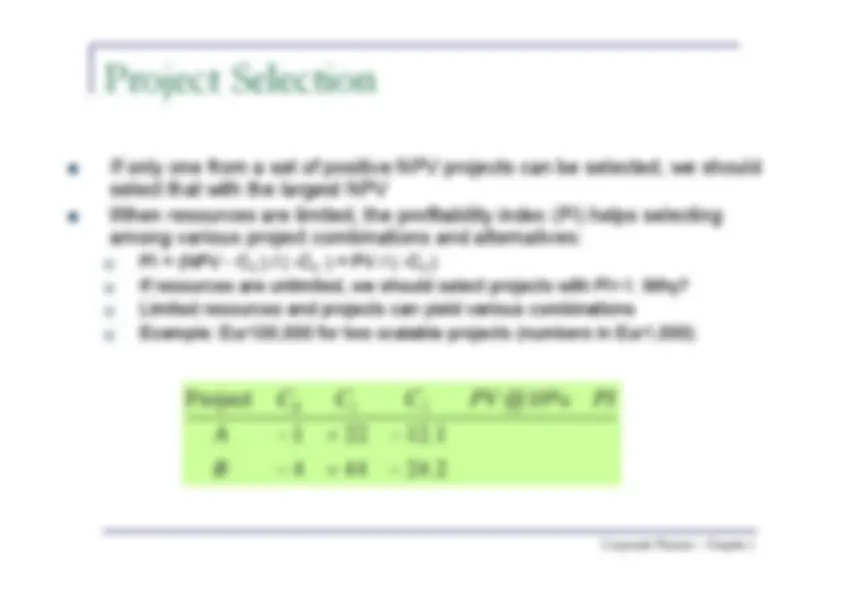

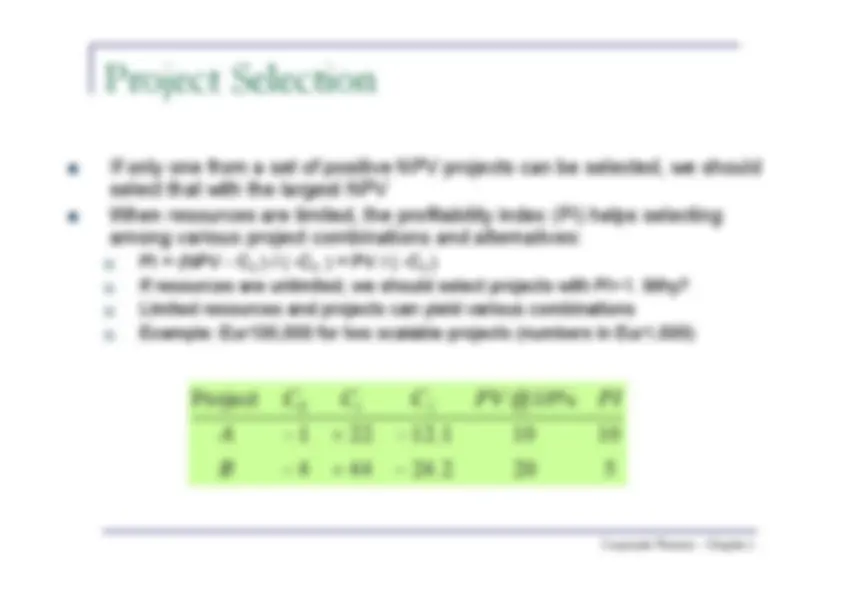

Part (b): evaluating risk-free projects

Corporate Finance - Chapter 1

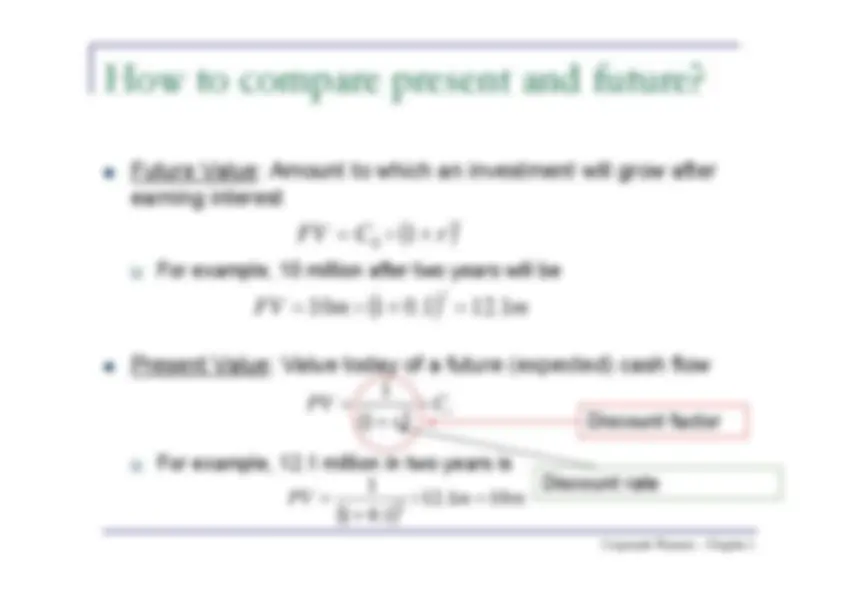

How to compare present and future?

Future Value: Amount to which an investment will grow afterearning interest

For example, 10 million after two years will be

Present Value: Value today of a future (expected) cash flow

For example, 12.1 million in two years is

t

0

2

t

t

C

r

PV

1

1

m

m

PV

10

1 .

12

1 .

0

1

1

2

Discount factor

Discount rate

Corporate Finance - Chapter 1

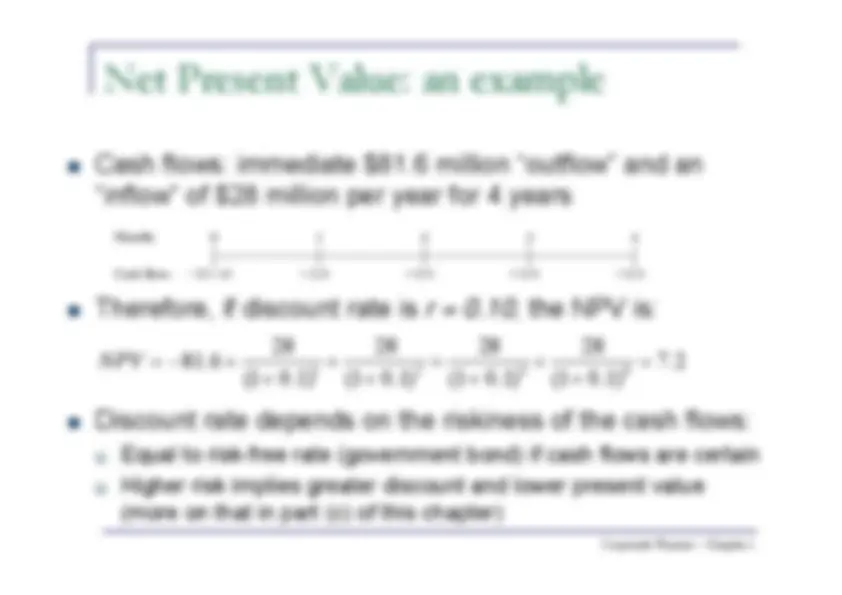

Net Present Value: an example

Cash flows: immediate $81.6 million “outflow” and an“inflow” of $28 million per year for 4 years

Therefore, if discount rate is

r = 0.

, the NPV is:

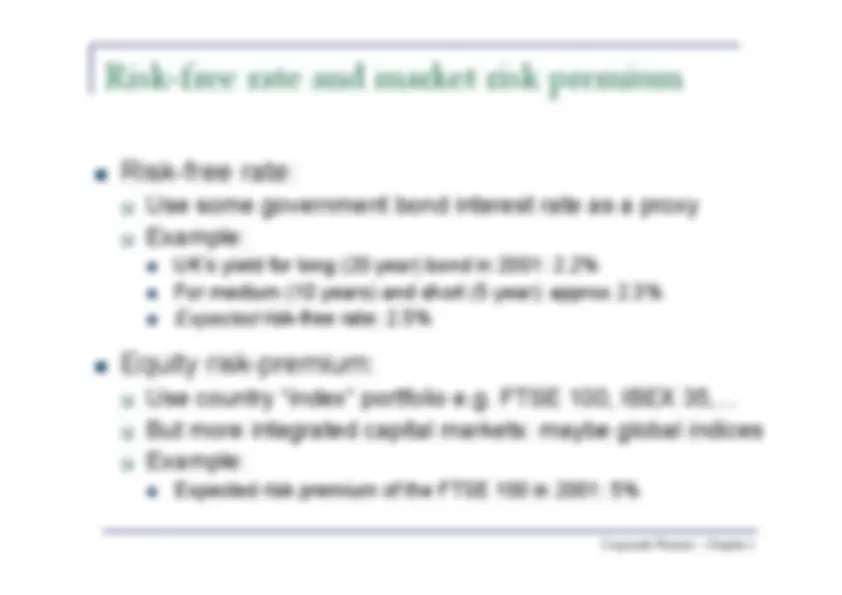

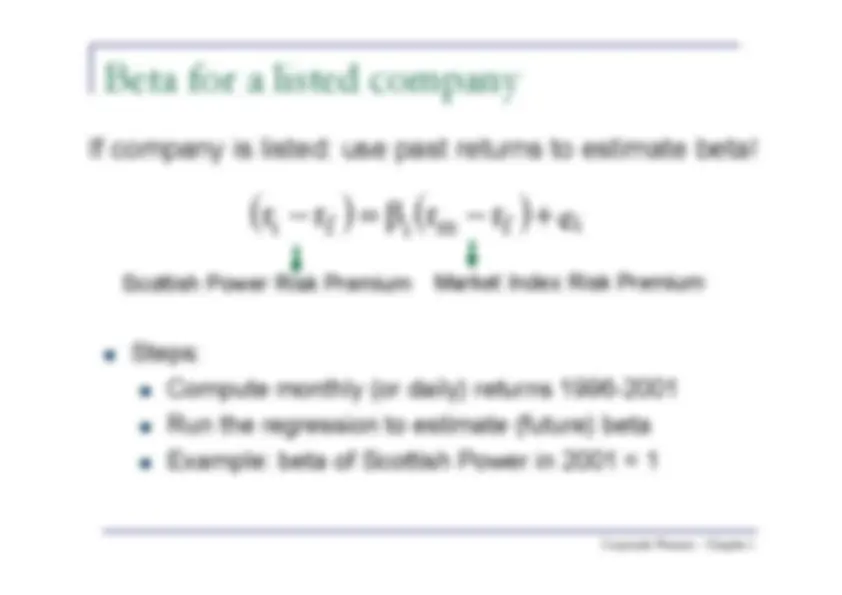

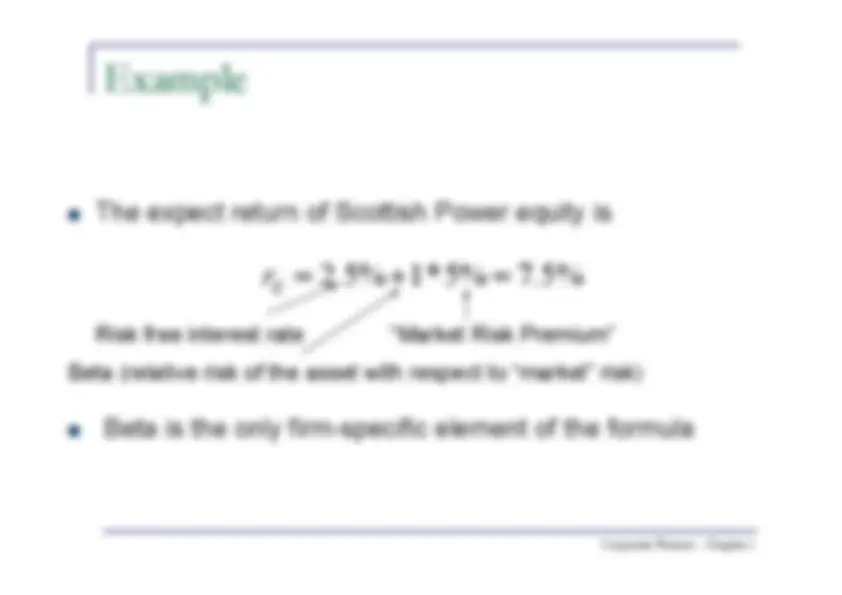

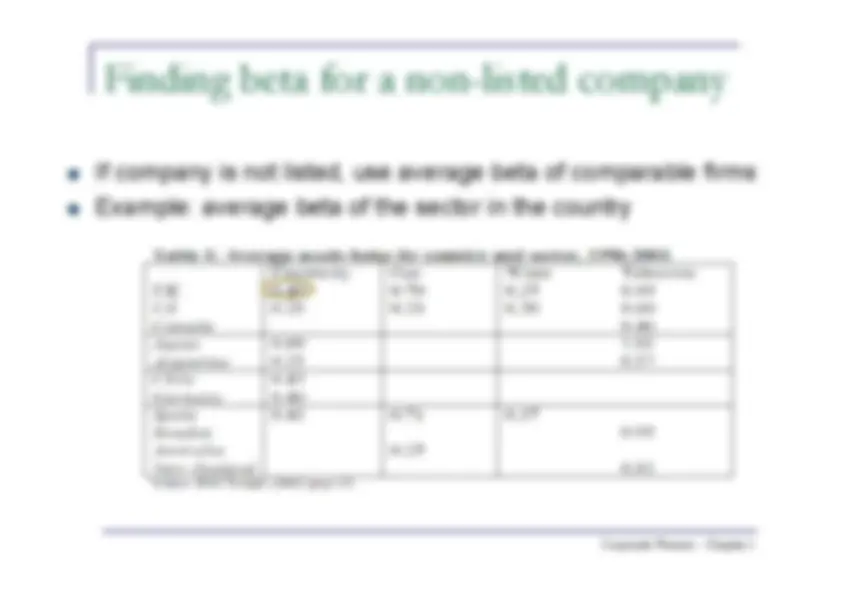

Discount rate depends on the riskiness of the cash flows:

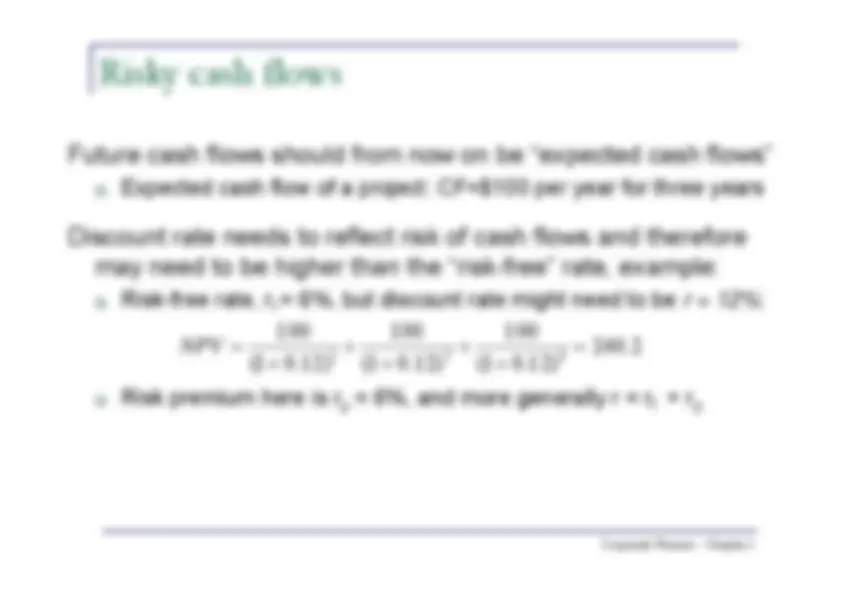

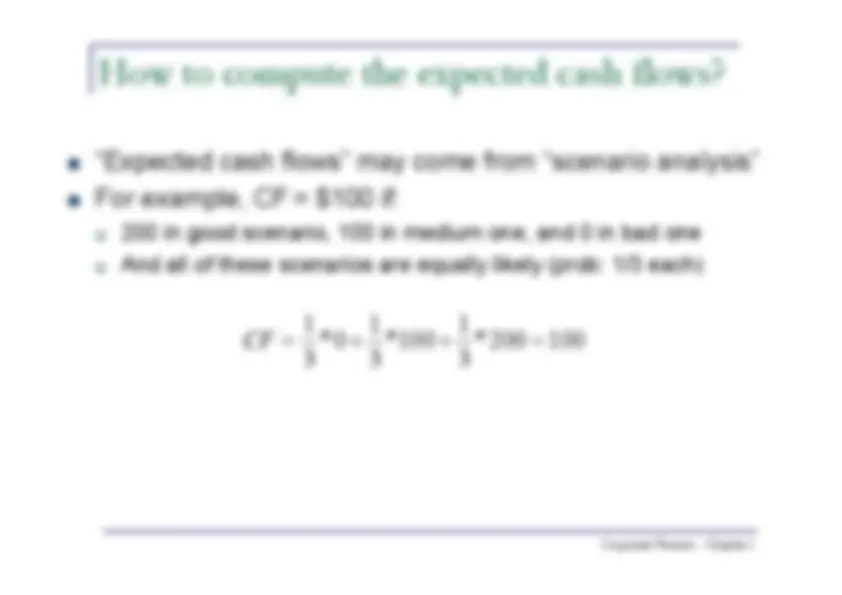

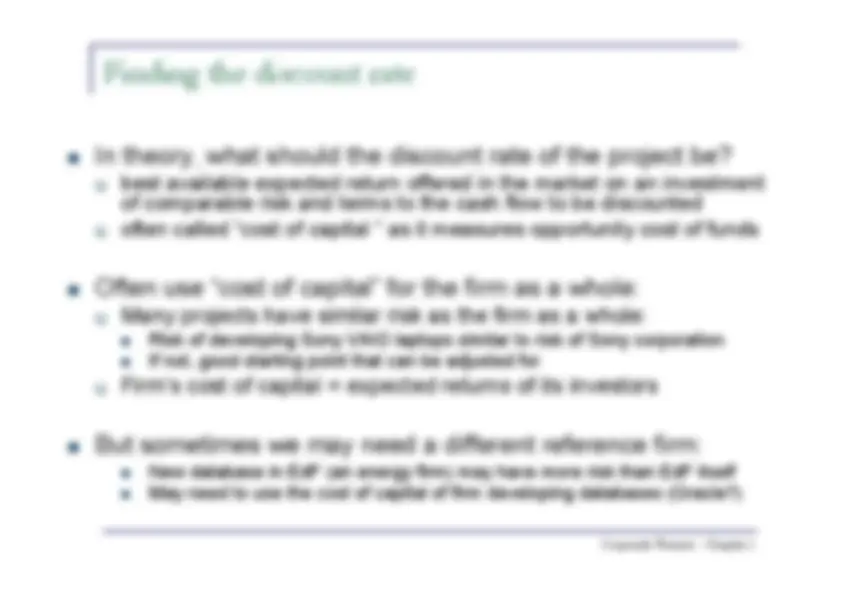

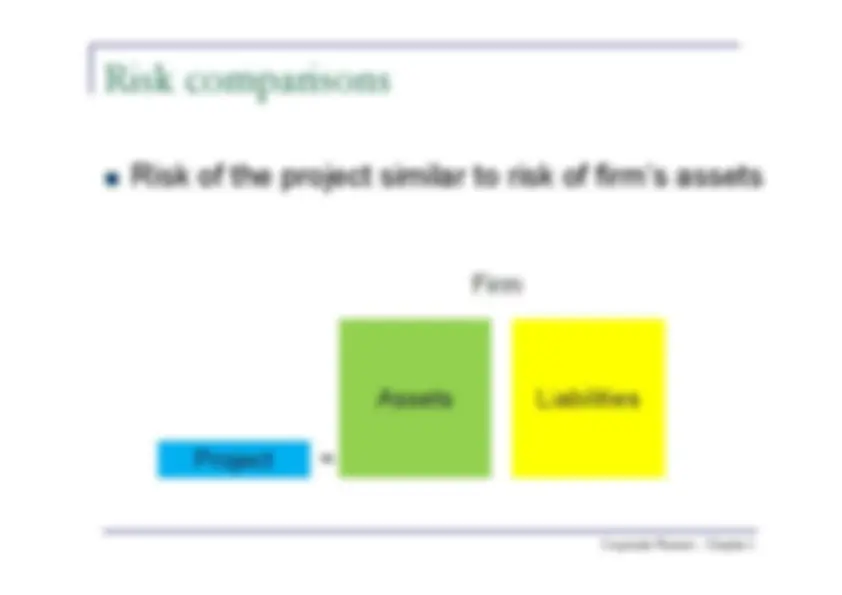

Equal to risk-free rate (government bond) if cash flows are certain

Higher risk implies greater discount and lower present value(more on that in part (c) of this chapter)

4

3

2

1

Corporate Finance - Chapter 1

In general, the NPV rule: Step 1: Forecast future cash flows

(see part (a) of this chapter)

Step 2: Estimate discount rate

(see part (c) of this chapter)

Step 3: Discount future cash flowsStep 4: Go ahead if PV of payoff exceeds

investment, i.e. if NPV > 0

T

T r

C r C r C r C

3 3 2 2 1 0 0

Corporate Finance - Chapter 1

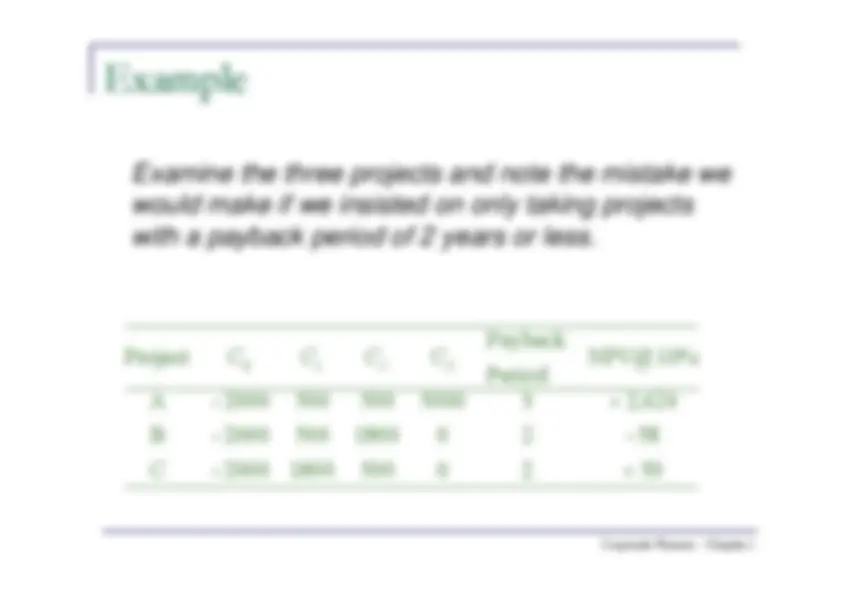

But, are there other criteria?

ProfitabilityIndex, 12%

Payback, 57%

IRR, 76% NPV, 75%

Book rate ofreturn, 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Survey Data on CFO Use of Investment Evaluation Techniques

SOURCE: Graham and Harvey, “The Theory and Practice of Finance: Evidence from the Field,”Journal of Financial Economics 61 (2001), pp. 187-243.

Corporate Finance - Chapter 1

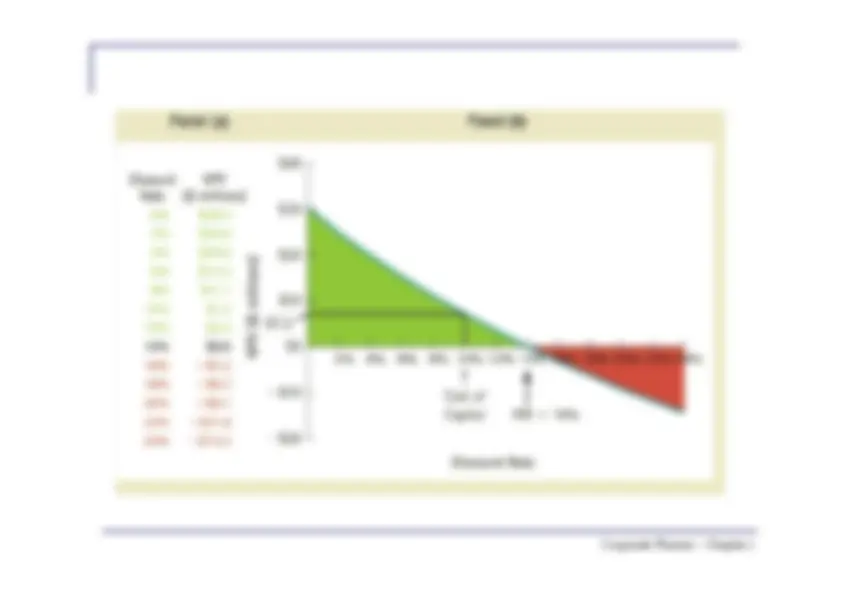

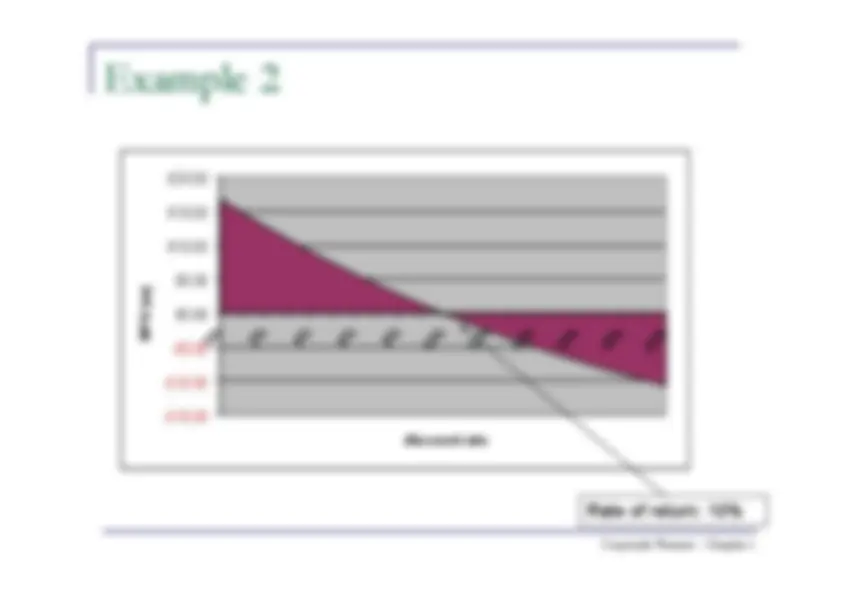

Example 2

-£10.00 -£15.

-£5.

£5.00£0.

£20.00£15.00£10.

NPV (m)

discount rate

Rate of return: 10%

Corporate Finance - Chapter 1

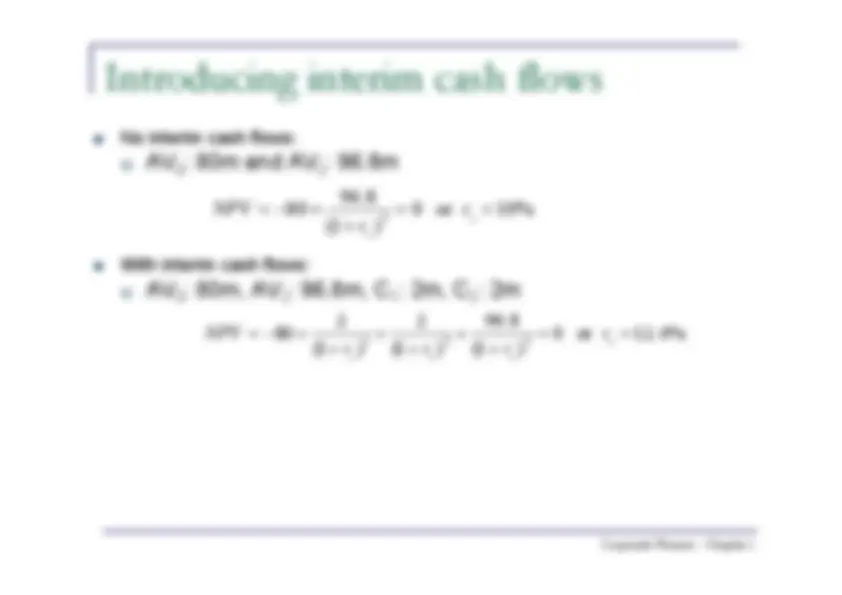

Introducing interim cash flows

No interim cash flows:

0

: 80m and AV

2

: 96.8m

With interim cash flows:

0

: 80m, AV

2

: 96.8m, C

1

: 2m, C

2

: 2m

%

10

or

0

)

1 (

8 .

96

80

2

y

y

r

r

NPV

%

4 .

12

or

0

)

1 (

8 .

96

)

1 (

2

)

1 (

2

80

2

2

1

y

y

y

y

r

r

r

r

NPV