Topic 4: Full Costing

Cost Accounting I

Department of Economics and Business

Universitat Pompeu Fabra

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Comptabilitat de Costos, Profesor: Mircea Epure, Carrera: Administració i Direcció d'Empreses, Universidad: UPF

Tipo: Apuntes

1 / 39

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Department of Economics and Business Universitat Pompeu Fabra

Direct-allocation method. Step-down allocation method. Reciprocal allocation method.

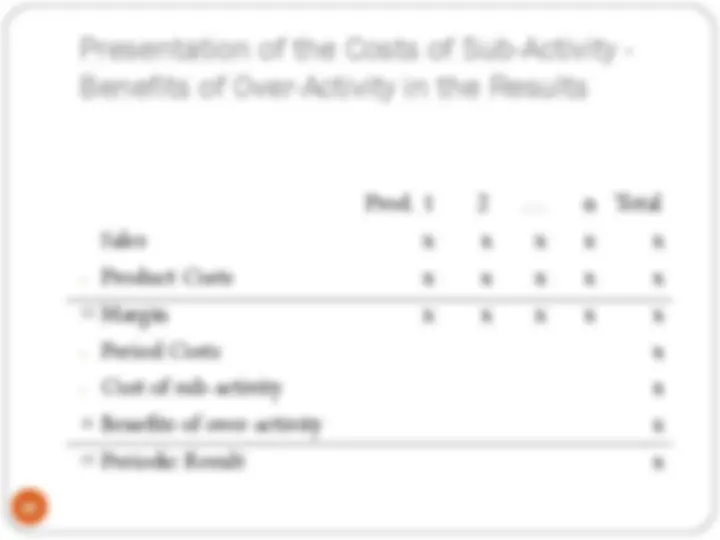

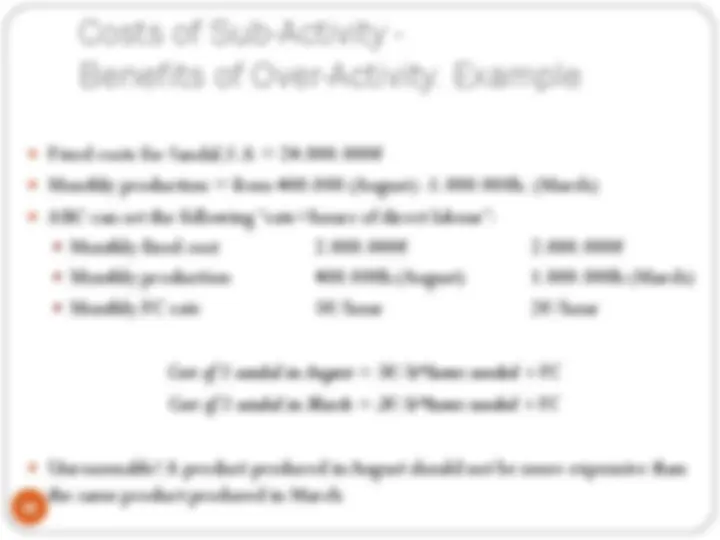

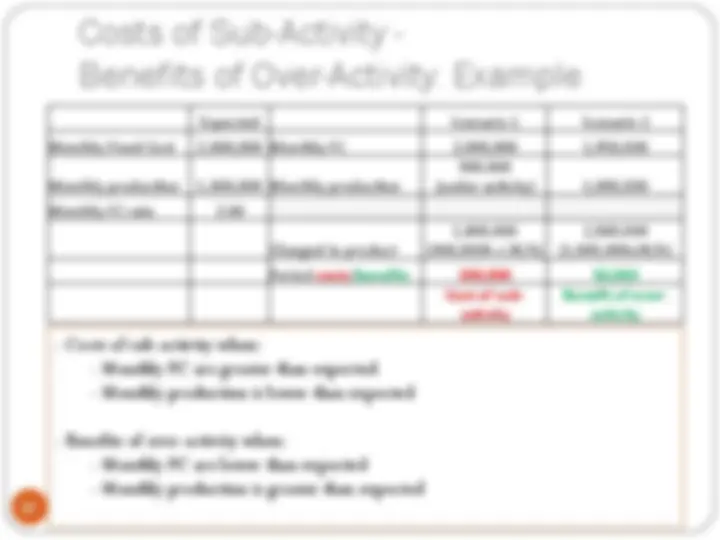

Costs of Sub-Activity and Benefits of Over-Activity. Waste, Scrap and By-Products – Definition. Valuation of Work-In-Process.

Direct Costs Product Costs Period Costs Indirect Costs manufacturing non-manufacturing optional

Indirect costs are allocated to products in two stages. Stage 1: Indirect Costs assigned to cost centers or departments. Stage 2: Costs accumulated in cost centers or departments are allocated to products.

Product Costs Direct Costs Indirect Costs Departments Departmental indirect cost rates

Operating Department Adds value to a product or service that is observable by a customer. Examples: Production, Marketing. Support Department Provides services that maintain other internal departments. Examples: Legal Department, Human Resources Department.

Cost Center Is a responsibility center in which a manager is accountable for costs only. It may be based on

Cost Pool Is a grouping of individual cost items. Examples:

Units produced If a single product or quite homogeneous products are produced. Machine-hours If relatively homogeneous machinery is intensively used. Direct labor-hours High proportion of relatively homogeneous labor. Direct labor-costs High proportion of heterogeneous labor (significant differences in the wages) Direct materials-costs High proportion of different direct materials (significant differences in materials’ costs)

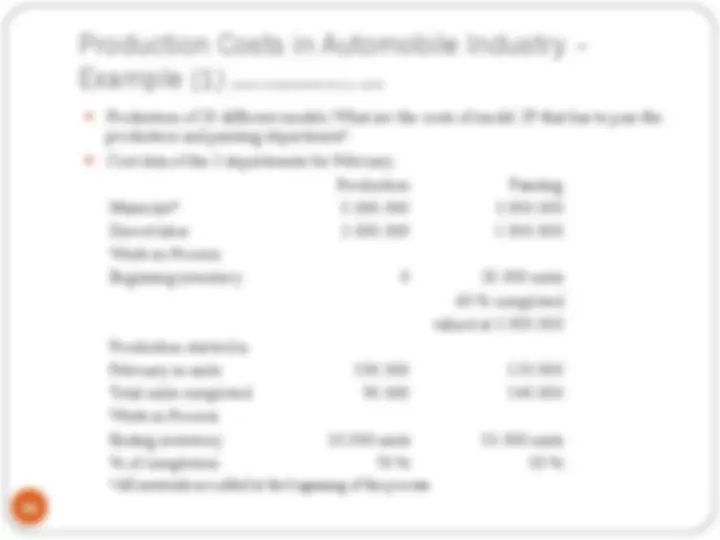

Statement of Costs Cost Items Production Painting Packaging Mainten. Administr. Managem. Total Materials Labor Rents Depreciat. Energy Others Total 20,200 16,100 38,100 8,900 41,100 16,000 140, Departments

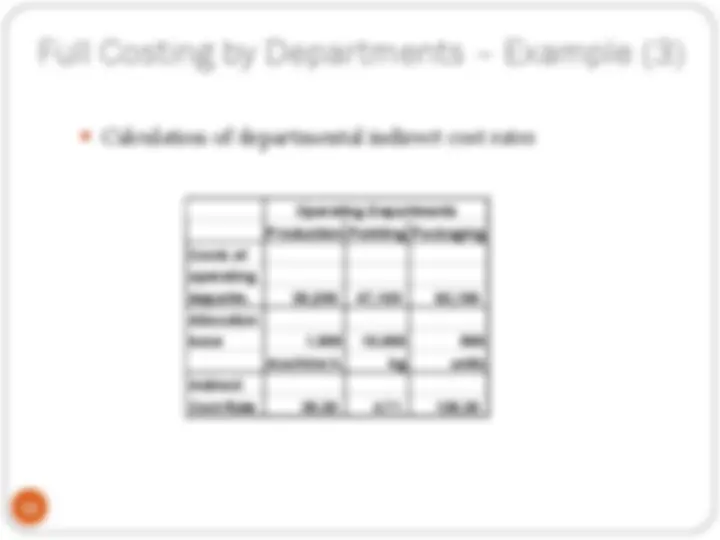

Calculation of departmental indirect cost rates Production Painting Packaging Costs of operating departm. 30,200 47,100 63, Allocation base 1,000 10,000 500 machine h. kg units Indirect Cost Rate 30.20 4.71 126. Operating Departments

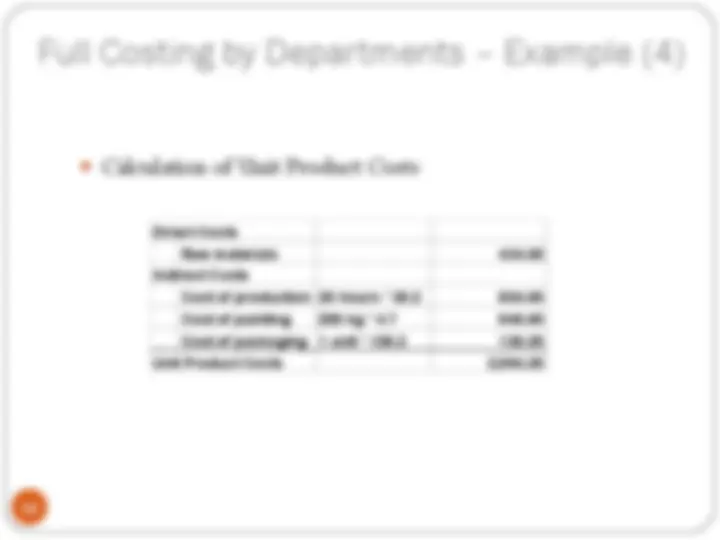

Calculation of Unit Product Costs Direct Costs Raw materials 424. Indirect Costs Cost of production 20 hours * 30.2 604. Cost of painting 200 kg * 4.7 940. Cost of packaging 1 unit * 126.2 126. Unit Product Costs 2,094.

Step-down allocation method Services rendered by support departments to other support departments are partially recognized. Procedure:

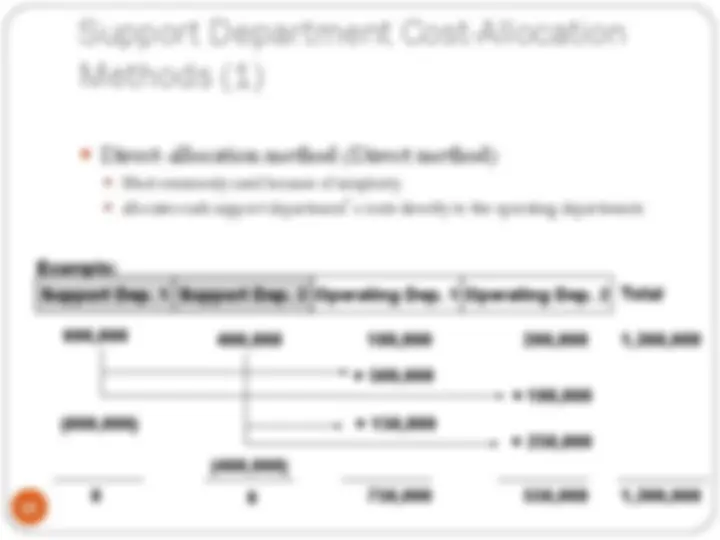

Step-down allocation method - continued Support Dep. 1 Support Dep. 2 Operating Dep. 1 Operating Dep. 2 600, (600,000) Example: 50, 350, 200,

Total 1,500, 0 1,500,

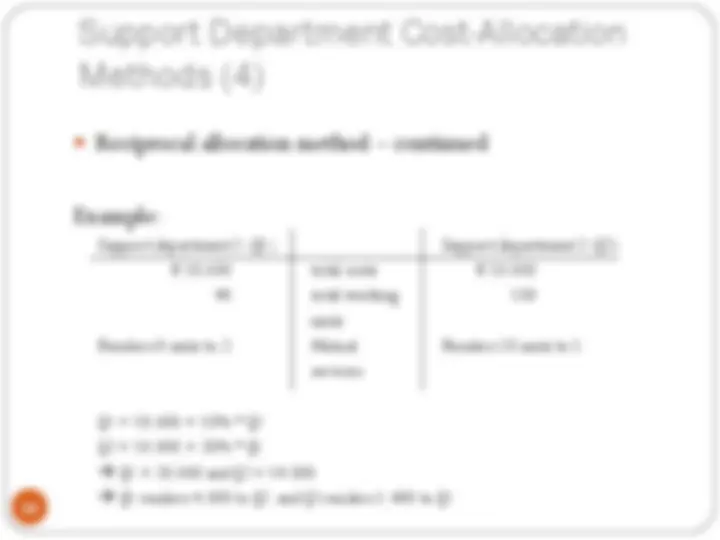

Reciprocal allocation method – continued Example: Support department 1 (§1) Support department 2 (§2) € 18,600 total costs € 10, 40 total working 100 units Renders 8 units to 2. Mutual Renders 10 units to 1. services §1 = 18,600 + 10% * § §2 = 10,000 + 20% * § à §1 = 20,000 and §2 = 14, à §1 renders 4,000 to §2, and §2 renders 1,400 to §

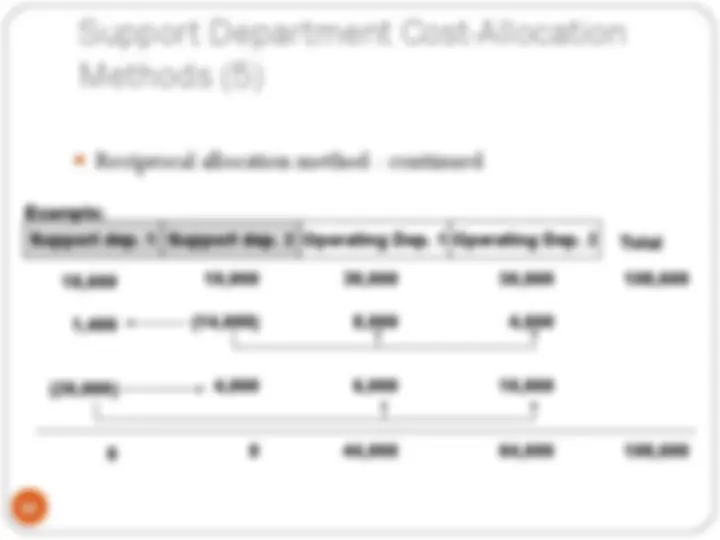

Reciprocal allocation method - continued Support dep. 1 Support dep. 2 Operating Dep. 1 Operating Dep. 2 18, 1, (20,000) 0 Example: 10, (14,000) 4, 0

Total 108, 108,