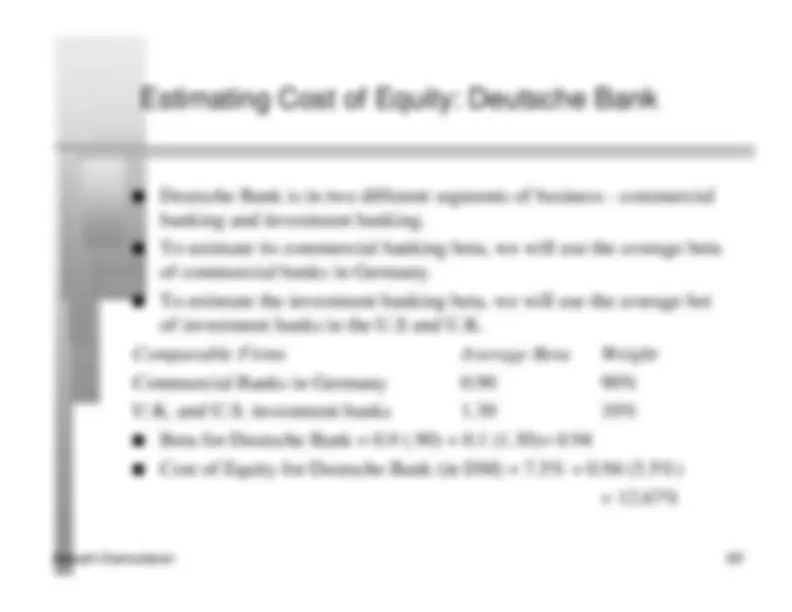

¡Descarga Relación Damodaran y CAPM y más Monografías, Ensayos en PDF de Finanzas Corporativas solo en Docsity!

Dealing with Risk : Investment

Analysis

Aswath Damodaran

First Principles

n Invest in projects that yield a return greater than the minimum

acceptable hurdle rate.

- The hurdle rate should be higher for riskier projects and reflect the financing mix used - owners’ funds (equity) or borrowed money (debt)

- Returns on projects should be measured based on cash flows generated and the timing of these cash flows; they should also consider both positive and negative side effects of these projects.

n Choose a financing mix that minimizes the hurdle rate and matches the

assets being financed.

n If there are not enough investments that earn the hurdle rate, return the

cash to stockholders.

- The form of returns - dividends and stock buybacks - will depend upon the stockholders’ characteristics. Objective: Maximize the Value of the Firm

The Riskfree Rate

n On a riskfree asset, the actual return is equal to the expected return.

n Therefore, there is no variance around the expected return.

Riskfree Rate and Time Horizon

n For an investment to be riskfree, i.e., to have an actual return be equal

to the expected return, two conditions have to be met –

- There has to be no default risk, which generally implies that the security has to be issued by the government. Note, however, that not all governments can be viewed as default free.

- There can be no uncertainty about reinvestment rates, which implies that it is a zero coupon security with the same maturity as the cash flow being analyzed.

The Bottom Line on Riskfree Rates

n Using a long term government rate (even on a coupon bond) as the

riskfree rate on all of the cash flows in a long term analysis will yield a

close approximation of the true value.

n For short term analysis, it is entirely appropriate to use a short term

government security rate as the riskfree rate.

n If the analysis is being done in real terms (rather than nominal terms)

use a real riskfree rate, which can be obtained in one of two ways –

- from an inflation-indexed government bond, if one exists

- set equal, approximately, to the long term real growth rate of the economy in which the valuation is being done.

Measurement of the risk premium

n The risk premium is the premium that investors demand for investing

in an average risk investment, relative to the riskfree rate.

n As a general proposition, this premium should be

- greater than zero

- increase with the risk aversion of the investors in that market

- increase with the riskiness of the “average” risk investment

Risk Aversion and Risk Premiums

n If this were the capital market line, the risk premium would be a

weighted average of the risk premiums demanded by each and every

investor.

n The weights will be determined by the magnitude of wealth that each

investor has. Thus, Warren Bufffet’s risk aversion counts more

towards determining the “equilibrium” premium than yours’ and mine.

n As investors become more risk averse, you would expect the

“equilibrium” premium to increase.

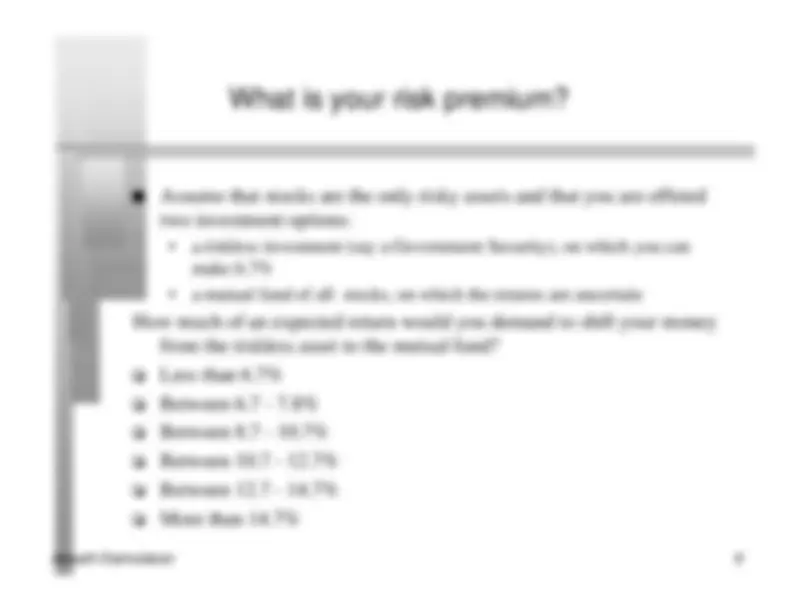

Risk Premiums do change..

Go back to the previous example. Assume now that you are making the

same choice but that you are making it in the aftermath of a stock

market crash (it has dropped 25% in the last month). Would you

change your answer?

o I would demand a larger premium

o I would demand a smaller premium

o I would demand the same premium

The Survey Approach

n Surveying all investors in a market place is impractical.

n However, you can survey a few investors (especially the larger

investors) and use these results. In practice, this translates into surveys

of money managers’ expectations of expected returns on stocks over

the next year.

n The limitations of this approach are:

- there are no constraints on reasonability (the survey could produce negative risk premiums or risk premiums of 50%)

- they are extremely volatile

- they tend to be short term; even the longest surveys do not go beyond one year

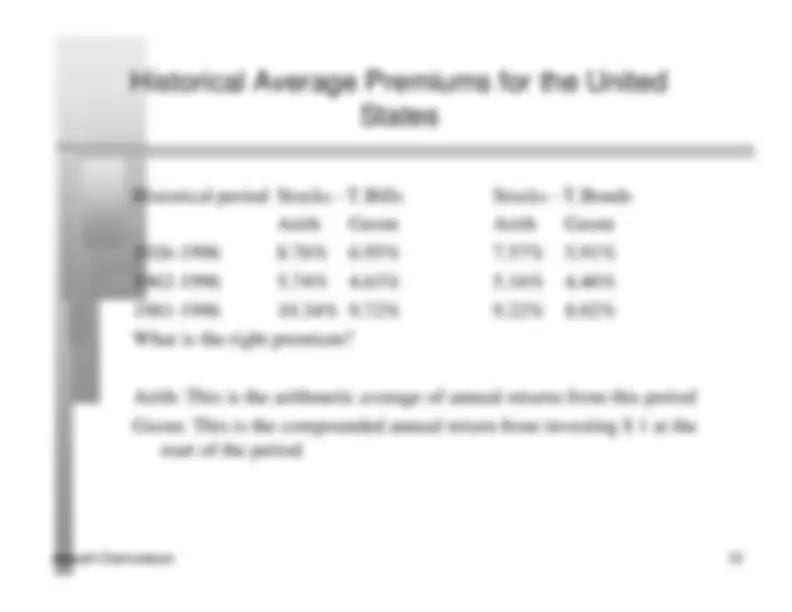

The Historical Premium Approach

n This is the default approach used by most to arrive at the premium to

use in the model

n In most cases, this approach does the following

- it defines a time period for the estimation (1926-Present, 1962-Present....)

- it calculates average returns on a stock index during the period

- it calculates average returns on a riskless security over the period

- it calculates the difference between the two

- and uses it as a premium looking forward

n The limitations of this approach are:

- it assumes that the risk aversion of investors has not changed in a systematic way across time. (The risk aversion may change from year to year, but it reverts back to historical averages)

- it assumes that the riskiness of the “risky” portfolio (stock index) has not changed in a systematic way across time.

What about historical premiums for other markets?

n Historical data for markets outside the United States tends to be sketch

and unreliable.

n Ibbotson, for instance, estimates the following premiums for major

markets from 1970-

Country Period Stocks Bonds Risk Premium Australia 1970-90 9.60% 7.35% 2.25% Canada 1970-90 10.50% 7.41% 3.09% France 1970-90 11.90% 7.68% 4.22% Germany 1970-90 7.40% 6.81% 0.59% Italy 1970-90 9.40% 9.06% 0.34% Japan 1970-90 13.70% 6.96% 6.74% Netherlands 1970-90 11.20% 6.87% 4.33% Switzerland 1970-90 5.30% 4.10% 1.20% UK 1970-90 14.70% 8.45% 6.25%

Risk Premiums for Latin America

Country Rating Risk Premium

Argentina BBB 5.5% + 1.75% = 7.25%

Brazil BB 5.5% + 2% = 7.5%

Chile AA 5.5% + 0.75% = 6.25%

Columbia A+ 5.5% + 1.25% = 6.75%

Mexico BBB+ 5.5% + 1.5% = 7%

Paraguay BBB- 5.5% + 1.75% = 7.25%

Peru B 5.5% + 2.5% = 8%

Uruguay BBB 5.5% + 1.75% = 7.25%

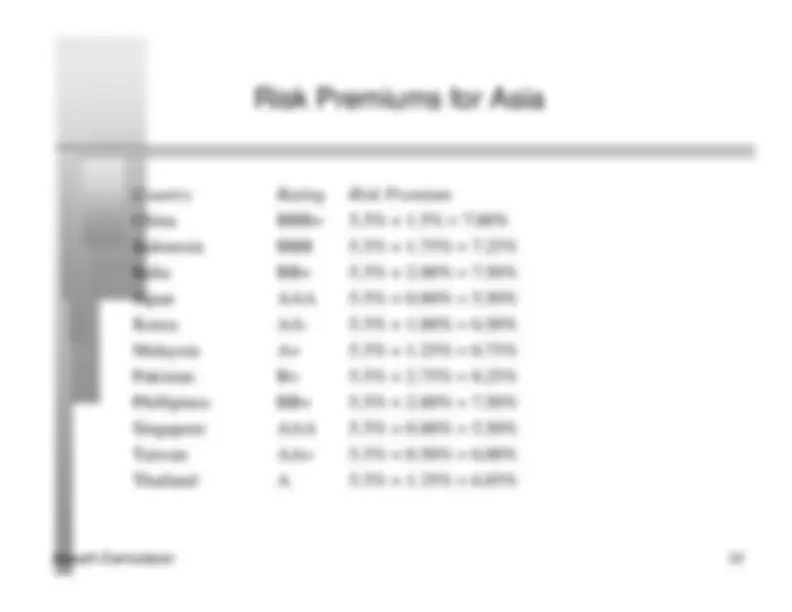

Risk Premiums for Asia

Country Rating Risk Premium China BBB+ 5.5% + 1.5% = 7.00% Indonesia BBB 5.5% + 1.75% = 7.25% India BB+ 5.5% + 2.00% = 7.50% Japan AAA 5.5% + 0.00% = 5.50% Korea AA- 5.5% + 1.00% = 6.50% Malaysia A+ 5.5% + 1.25% = 6.75% Pakistan B+ 5.5% + 2.75% = 8.25% Phillipines BB+ 5.5% + 2.00% = 7.50% Singapore AAA 5.5% + 0.00% = 5.50% Taiwan AA+ 5.5% + 0.50% = 6.00% Thailand A 5.5% + 1.35% = 6.85%

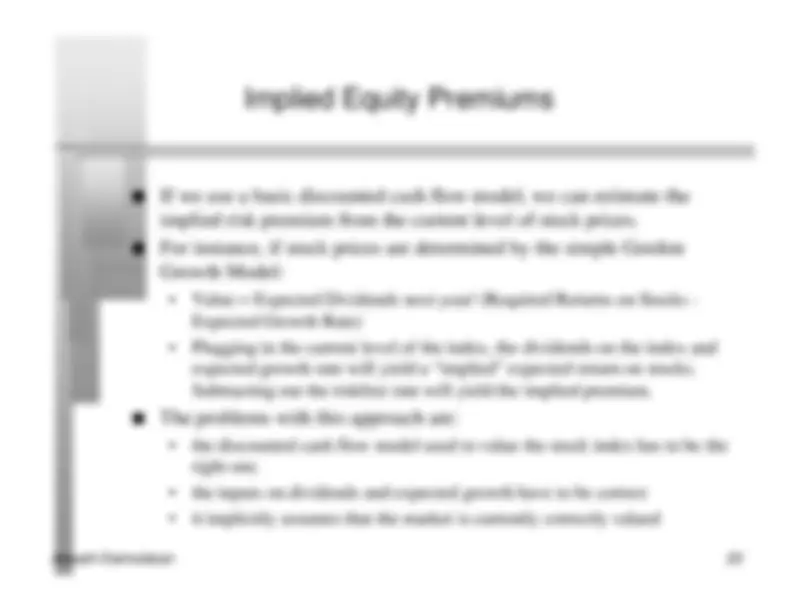

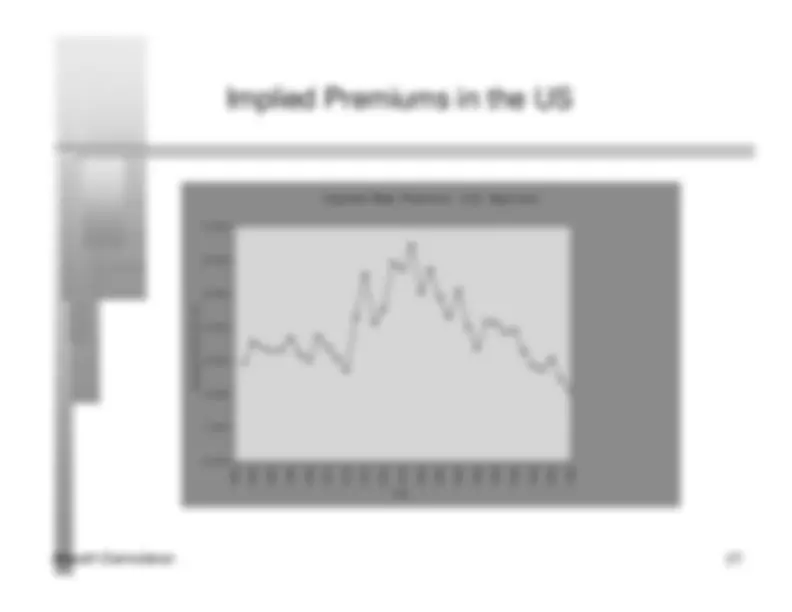

Implied Equity Premiums

n If we use a basic discounted cash flow model, we can estimate the

implied risk premium from the current level of stock prices.

n For instance, if stock prices are determined by the simple Gordon

Growth Model:

- Value = Expected Dividends next year/ (Required Returns on Stocks - Expected Growth Rate)

- Plugging in the current level of the index, the dividends on the index and expected growth rate will yield a “implied” expected return on stocks. Subtracting out the riskfree rate will yield the implied premium.

n The problems with this approach are:

- the discounted cash flow model used to value the stock index has to be the right one.

- the inputs on dividends and expected growth have to be correct

- it implicitly assumes that the market is currently correctly valued