¡Descarga Consumption and Investment: Expectations and Wealth Effects y más Apuntes en PDF de Economía solo en Docsity!

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

I.^

EXPECTATIONS,CONSUMPTIONAND INVESTMENT a)^ “New” consumption theoryb)^ “New” investment theoryc)^ Volatility of consumption and investment Ch. 16 in Blanchard-Amighini-Giavazzi

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.2^ What^

is^ the

role^

of^ expectations

in^ determining

spending

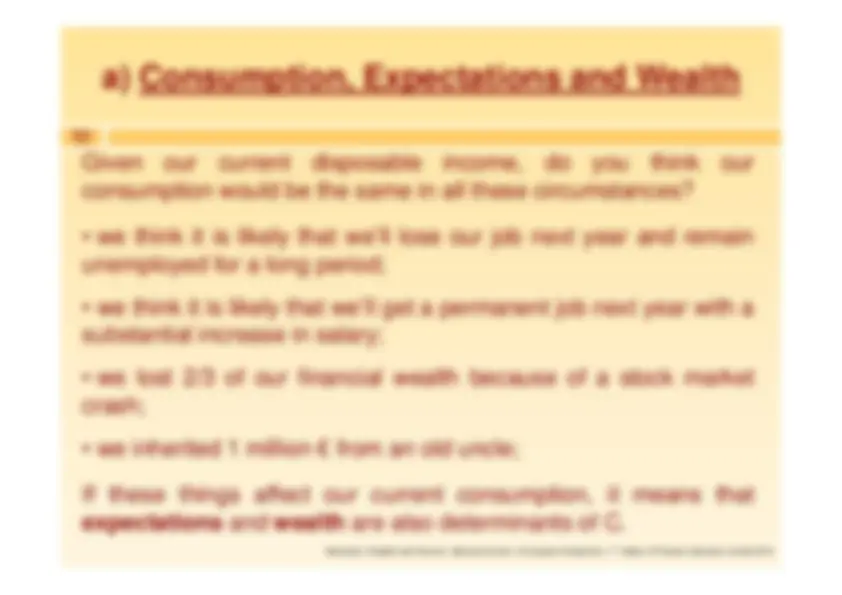

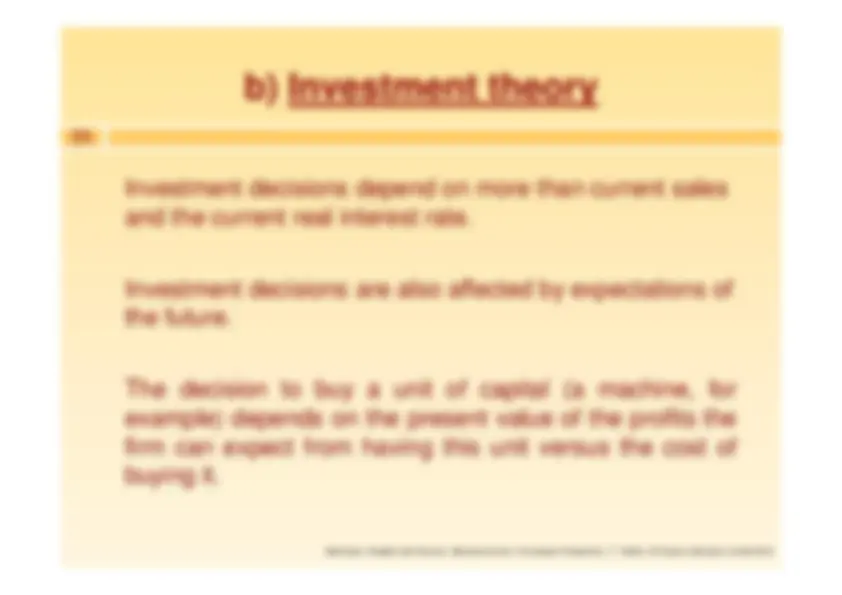

components, i.e. consumption and investment?• Consumption depends not only on current income but also ontotal^ wealth (present value of expected future labor and non-labor income).• Investment depends not only on current profits but also onexpected future profits.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.4^ The theory of consumption was developed by MiltonFriedman in the 1950s, who called it the

permanent

income theory of consumption

, and by Franco

Modigliani, who called it the

life cycle theory of

The permanent income theory of consumption consumption.^ In words:^ Consumption is an increasing function of total wealth,and also an increasing function of after-tax labourincome. Total wealth is the sum of non-human wealth –financial wealth plus housing wealth – and humanwealth – the present value of expected after-tax income.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.

Intertemporal choice

Consumption and saving are two sides of the same choice: howmuch of current (net) income to consume now, how much to save forfuture consumption.•^ Example

: 2 periods – period 1 (current) and period 2 (future)

, future (expected) real income y 1

. Saving 2

s^ (or

borrowing, if negative). Real interest rate r. – Budget constraints:

c+s= y^1

,^ c= y 12

+(1+r)s 2

-cfrom the first into the second constraint: 11

c= y+(1+r)(y^22

-c). 11

- Divide both sides by (1+r) and rearrange to get the^ intertemporal budget constraint

c+ [1/(1+r)] c^1

= y+ [1/(1+r)] y 21

2

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.7^ •^ Consumers

preferences

over current and future consumption can

be represented with

indifference curves

(as if c

and c 1

were two 2

goods).^ – Each

curve^

represents

all^ the

combinations

of^ current

and^ future

consumption among which the consumer is indifferent, that is those thatprovide the same

utility level

- if we represent preferences with a

utility

function^

U(c, c) assigning a value to each basket (c^12

, c). 12

-^ Convex indifference curves mean that consumers prefer a morebalanced consumption path over time (relatively close levels of c

1

and c) rather than more extreme combinations (such as high c^2

low cor viceversa)^2

→^ consumption smoothing

Intertemporal preferences

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.

c^2

cy^1 y^2

1

2

1+r

To represent the intertemporalbudget constraint graphically,rewrite it as:^ c= (1+r) y^2

+ y- (1+r) c 12

. 1

Given y^1

and y, c 2

is a linear 2 function of c

with a negative 1 slope given by -

(1+r). The^ optimal

combination

of

current and future consumptionis the point along the budgetconstraint

that^ lies

on^ the Intertemporal optimization highest indifference curve, i.e.a point of tangency.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.

c^2

cy^1 y^2

1

2

1+r^ y'^1

An increase in currentincome increasesconsumption but alsosaving (

∆^ c<^ ∆^1

y).^1 Change in current income

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.11^ An increase in expectedfuture income increasescurrent consumption(reducing saving).

c^2

cy^1 y^2

1

2

1+r

y'^2

Change in expected income

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.

To summarize:

-^ Consumers prefer more balanced consumptions paths over time toextreme variations (

consumption smoothing

). By adjusting saving

(and^ borrowing)

they^

can^ compensate

income

fluctuations

and

maintain a more stable consumption path. Then consumption is likelyto respond less than one-for-one to fluctuations in current income.•^ Permanent

changes

in^ income

affect^

consumption

more^

than

temporary changes

-^ Expectations

about

future

disposable

income

or^ economic

conditions (consumer confidence) affect current consumption. Thenconsumption may move even if current income does not change.• Changes in non-human

wealth

may also affect consumption.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

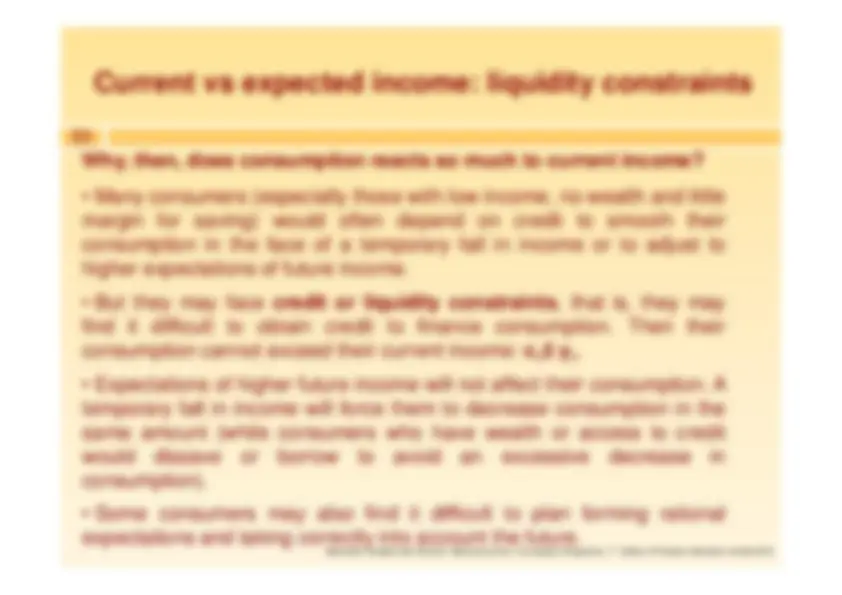

Current vs expected income: liquidity constraints Slide16.14 Why, then, does consumption reacts so much to current income? • Many consumers (especially those with low income, no wealth and littlemargin for^ saving)

would^

often^ depend

on^ credit

to^ smooth

their

consumption in the face of a temporary fall in income or to adjust tohigher expectations of future income.• But they may face

credit or liquidity constraints

, that is, they may

find^ it^

difficult^

to^ obtain

credit^

to^ finance

consumption.

Then^

their

consumption cannot exceed their current income:

c≤^ y.^11

- Expectations of higher future income will not affect their consumption. Atemporary fall in income will force them to decrease consumption in thesame amount (while consumers who have wealth or access to creditwould^

dissave

or^ borrow

to^ avoid

an^ excessive

decrease

in

consumption).• Some consumers may also find it difficult to plan forming rationalexpectations and taking correctly into account the future.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.

The present value of expected profits The^ present value of expected profits

depends on

how long the machine/unit of capital will last.The^

depreciation

rate ,

δ,^ measures

how

much

usefulness the machine loses from one year to thenext. (reasonable values for

δ^ are between 4% and 15% for machines, and between 2% and 4% for buildings and factories)

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.17^ The present value, at year

t , of expected profit in year

t+1^ generated by

the extra machine equals:The present value, at year

t , of expected profit in year

t+2^ equals:

1^ e Π t^1 + r^^ ) (^1) (+ t^ e te t rr (^) t

2 ) (^1) ( ) (^1) )( 1 (^1 1) (

Π− ++

δ

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

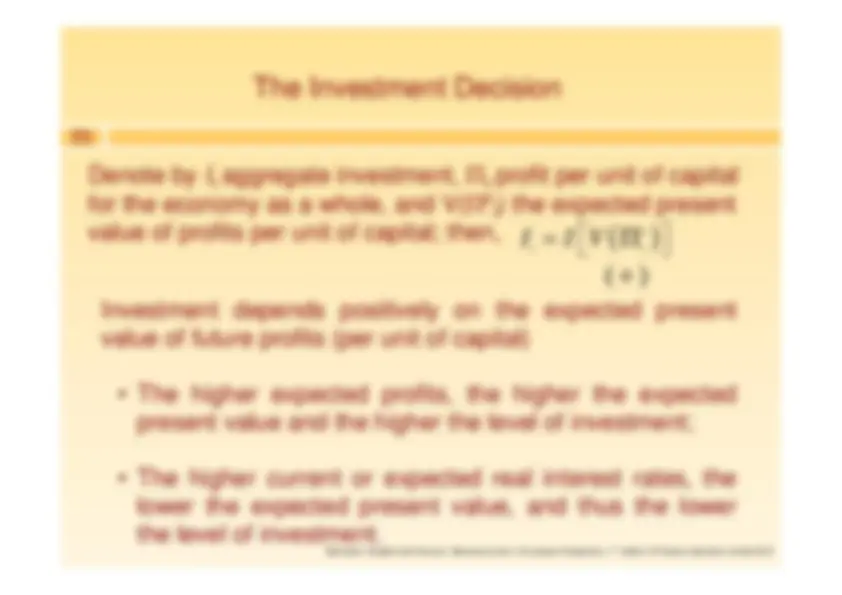

Slide16.19^ Denote by

I aggregate investment, t^

Πprofit per unit of capital t^

for the economy as a whole, and V(

eΠ) the expected present t

value of profits per unit of capital; then,Investment

depends

positively

on^ the

expected

present

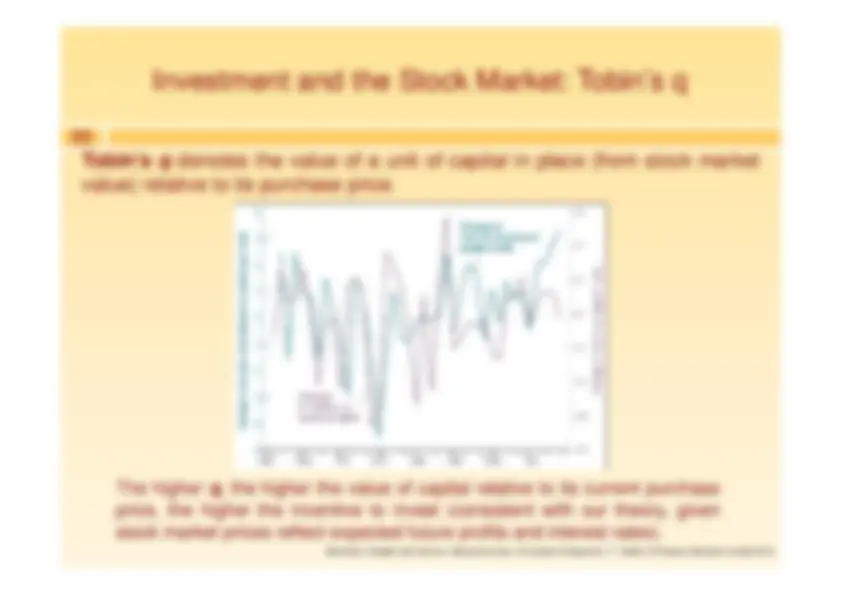

value of future profits (per unit of capital)^ •^ The higher expected profits, the higher the expectedpresent value and the higher the level of investment;^ •^ The higher current or expected real interest rates, thelower the expected present value, and thus the lowerthe level of investment.

e ( ) ( )+ t^

t I^ I V =^

Π

The Investment Decision

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1Edition, © Pearson Education Limited 2010

Slide16.20^ Suppose firms expect a constant flow of future profits andconstant interest rates (static expectations):

e^

e 1 2 t^

t^

t

+^

Π^ = Π

=^

Π... = e^

e 1 2 t^

t^

t

r^

r^

r

+^ =^ =^ +

... =

Under these assumptions, the present value simplifies to

e ( )^

t V^ t rt

Π^ δ Π^ =

A special case^ and