¡Descarga Expectations, Output & Fiscal Policy: Analysis from 'Macroeconomics: European Perspective' y más Apuntes en PDF de Economía solo en Docsity!

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

I.4 EXPECTATIONS,OUTPUT AND POLICY^ a) Ch. 17 in Blanchard-Amighini-Giavazzi

Expectations and the IS relation

b)

Expectations and the LM relation

c)

Monetary policy revisited

d)

Fiscal policy revisited

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Figure 17.

Expectations and spending: the channels

Expectations affect consumption and investment decisions, both directlyand through asset prices

a) Expectations and the

IS

Relation

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

-^

A decrease in

the current real interest rate

reduces the

capital user cost and increases investment.

-^

A decrease in

the current real interest rate

makes current

consumption cheaper relative to future consumption, whichmay also lead to an increase in consumption.

-^

Temporary

changes

in

income

(or

interest

rates)

have

smaller

effects

on

aggregate

demand

than

permanent

changes.

-^

Hence, a decrease in the

current real interest rate

, given

unchanged expectations of the future rates, has only smalleffect on spending: the new IS will be steeper.

Expectations, Wealth, Consumption and Investment

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

The new

IS

curve is steeper, which means that a large

decrease in the current interest rate is likely to have only asmall effect on equilibrium income, for two reasons:•

A decrease in the current real interest rate does not havemuch effect on spending if future expected rates are notlikely to be lower as well.

-^

The multiplier is likely to be small. If changes in income arenot expected to last, they will have a limited effect onconsumption and investment.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Expectations and the

IS

Relation

- Increases in government spendingor in expected future output shift the IS

curve to the right.

in

taxes,

in

expected

future taxes or in the expected futurereal interest rate shift the

IS

curve to

the left.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

The

IS

is then the relation between aggregate spending

Y

and real

interest rate

r

for given policy variables

G

, T

,^

expectations

(of

consumers and investors) and

wealth

Y= C(W

e, Y-T) + I(V

e, Y, r) + G

IS:

Y= Y( r ; G, T, W

e, V

e)

where

-^

W

e^

represents the expected (present) value of consumers’ lifetime

wealth, which depends on current wealth, expected future incomes,future taxes, current and future interest rates and dividends, etc. •^

eV represents

the

expected

present

value

of

(after-tax)

future

profits.

The “new”

IS

relation

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

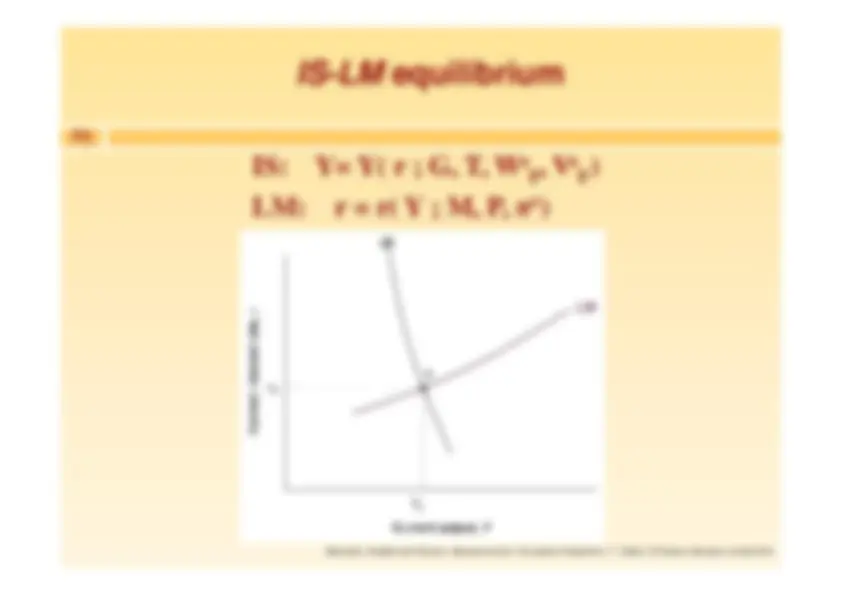

IS:

Y= Y( r ; G, T, W

e F

, V

e F

)

LM:

r = r( Y ; M, P,

π

e)

IS-LM

equilibrium

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

- The effects of monetary policy depend crucially on its effect on expectations

- If a monetary expansion leads financial investors, firms andconsumers to revise their expectations, the effects on aggregatedemand will be

larger

-^ with a higher expected inflation, the downward shift of the LM and thedecrease in r will be larger; •^ with the expectation of lower future interest rates or higher future output,the IS will also shift to the right.

c) Monetary policy revisited

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

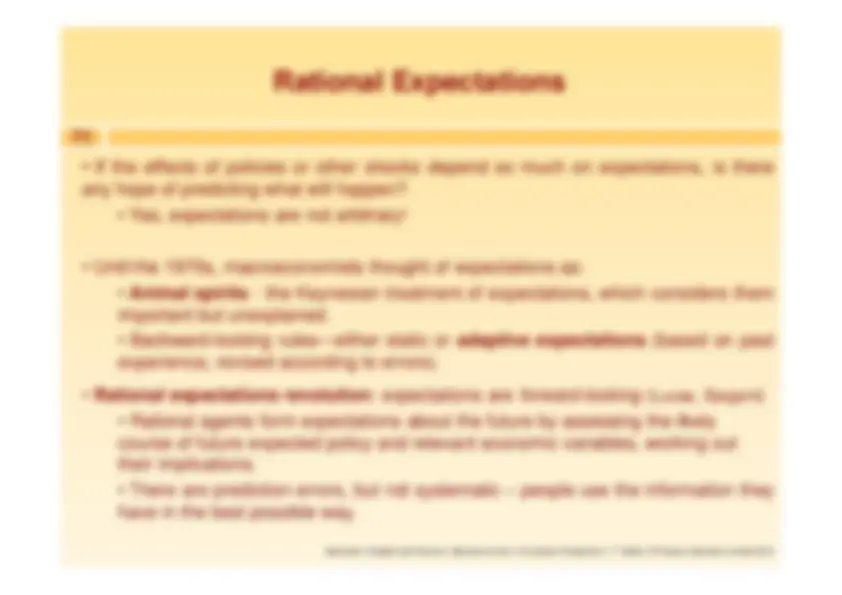

Rational Expectations

-^ If the effects of policies or other shocks depend so much on expectations, is thereany hope of predicting what will happen? - Yes, expectations are not arbitrary! - Until the 1970s, macroeconomists thought of expectations as: -^ Animal spirits - the Keynesian treatment of expectations, which considers them

important but unexplained.• Backward-looking rules—either static or

adaptive expectations

(based on past

experience, revised according to errors).

-^ Rational expectations revolution

: expectations are

forward-looking

(Lucas, Sargent)

- Rational agents form expectations about the future by assessing the likelycourse of future expected policy and relevant economic variables, working outtheir implications.• There are prediction errors, but not systematic – people use the information theyhave in the best possible way.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

-^

The effects of fiscal policy also depend on how they affect

expectations

. For example, a reduction in the budget deficit

(decreasing G or increasing T) would imply: –^ In the short run, under constant expectations, lower current spending

→

IS

(and AD) shift to the left

→

contractionary effects on output.

- In the medium run, no effects on output (natural level), lower real interestrates, higher investment. – In the long run, higher investment

→

higher capital stock

→

higher output,

i.e. higher future income, lower future taxes (IS shift to the right). –^ Taking into account future benefits, therefore, a budget deficit reductioncould also have positive benefits in the short run!

d) Fiscal Policy revisited

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

•^

Back loading

the deficit reduction toward the future, with small

cuts in the present and larger cuts in the future is more likely tolead to an increase in output.

-^

Back loading, however, may decrease the credibility of the deficitreduction program, leaving most of the reduction for the future,not the present.

-^

The government must balance: enough cuts in the current periodto show a commitment to deficit reduction and enough cuts left tothe future to reduce the adverse effects on the economy in theshort run.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Anything that improves expectations about the future, makes deficitreduction programme less painful:•^

Measures

reducing

distortions

in

the

economy

(tax

distortions,

inefficiencies in social security, unemployment benefits, labor andproduct markets regulations) and improving productivity (supply sidepolicies) would have a stronger positive effect on expectations andcurrent spending.

-^

In a major fiscal crisis (high government spending, low tax revenues,very large deficit), a credible deficit reduction program induces lesspessimistic expectations, may actually have a positive net effect oncurrent demand and output.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

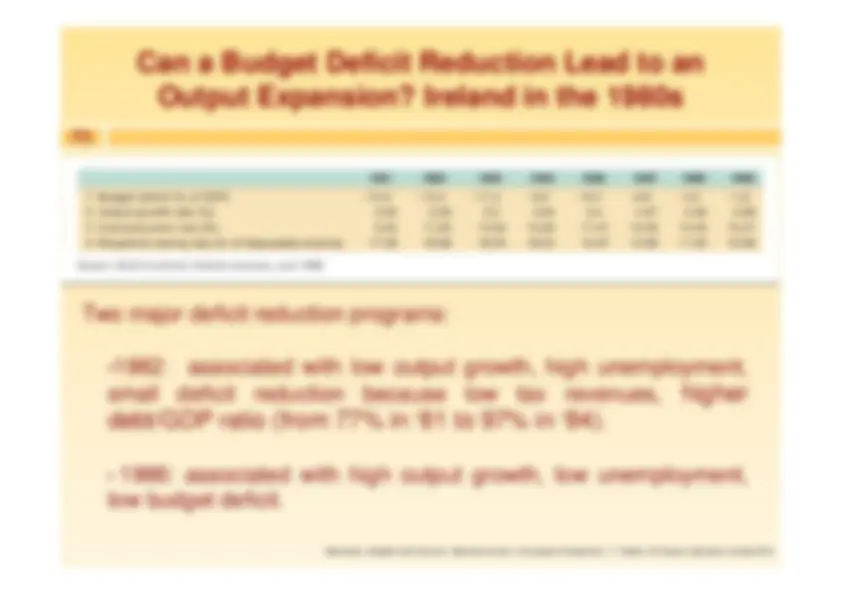

Can a Budget Deficit Reduction Lead to an

Output Expansion? Ireland in the 1980s

Two major deficit reduction programs:

associated with low output growth, high unemployment,

small

deficit

reduction

because

low

tax

revenues

,^

higher

debt/GDP ratio (from 77% in ‘81 to 97% in ‘84). •^ 1986: associated with high output growth, low unemployment,low budget deficit.

Blanchard, Amighini and Giavazzi,

Macroeconomics: A European Perspective

st^ , 1 Edition, © Pearson Education Limited 2010

Slide17.20^ Why were the results of the two programs so different?• There were some important differences:

- 1982: mostly tax increases. – 1986: cuts in government spending, increase in tax base rather than tax rates.

- Key difference: positive impact on expectations in the second butnot the first program.

rate

increased

in

the

first

case

(more

pessimistic

consumers);

decreased in the second case (more optimistic consumers). –^ Also, positive supply side changes in the second time: productivity increasing,tax breaks for foreign firms.