7. THE FINANCIAL SYSTEM

English Group (AR) -ECO

References:García Delgado &Myro (2020): chapter 13

Spanish Economy, 2020-2021 0

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

An overview of the Spanish financial system, focusing on the banking system, money and capital markets, and financial intermediaries. It discusses the classification of financial markets, the role of financial intermediaries, and the prevalence of the bank-based model in Spain. The document also covers the history of the Spanish banking system, its main players, and the impact of the financial crisis on the system.

Tipo: Apuntes

1 / 48

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

English Group (AR) - ECO References : García Delgado & Myro ( 2020 ): chapter 13

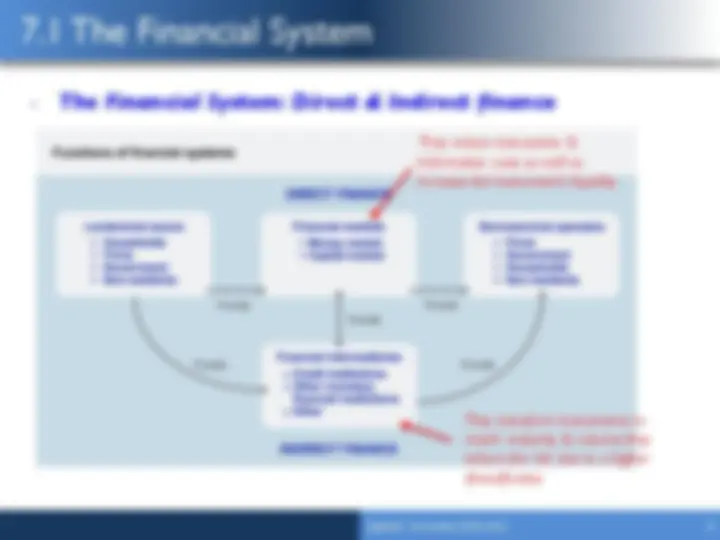

They reduce transaction & information costs as well as increase the instrument’s liquidity They transform instruments to match maturity & volume; they reduce the risk due to a higher diversification

FINANCIAL INTERMEDIARIES : are economic agents that acquire funds issued by the lenders and transform these funds into assets which are lent to the borrowers. Main functions: Reduce the information costs of the system Match the needs between borrowers & lenders

Banks (deposit-taking institutions; their liabilities are used as mean of payment, together with coins and notes)

Financial systems can be classified (à in a corporate finance ¹ perspective) wrt several dimensions:

1. The pre-crisis banking system

ü Reinforcement of prudential regulation (obligation to fulfil a coefficient of own resources, ...). ü Improvement of supervisory systems. ü Development of deposit protection funds (deposit guarantee fund).

Ø In the face of the intensification of the competition, the entities respond by concentrating the activity (BBVA, BSCH), an international expansion and the mediation of disintermediation.

The main players in the Spanish BS

Ø Traditionally they were active in corporate financing; however, they gained relevance in the mortgage loans market and in the household financing in the last years before the crisis.

institutions that use their profits by financing social (healthcare and

Ø Cooperativas de crédito (credit unions): they distribute benefits among their members.

# of firms Branches Workers Market share Banks 153 (51 Spanish) 15.000 110.000 45% Saving Inst. (CCAA) 46 24.000 132.000 50% Credit Unions 81 5.000 21.000 5% Data for 2009

q It is a model of universal banking in which banks carry out a wide range of operations (gathering deposits, conceding credit lines, investing in financial assets,...).

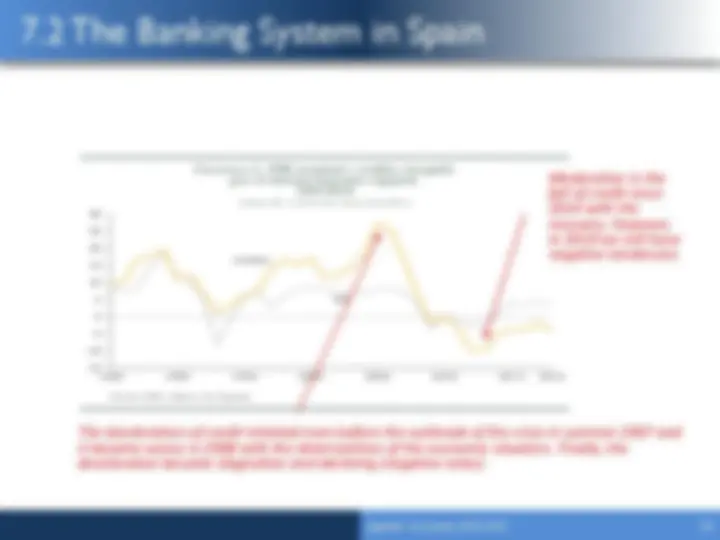

The 2008 CRISIS q PERIOD [1] : The Spanish Banking system avoided the first wave of

Ø Regulation by the Bank of Spain (countercyclical provisions) Ø Specialization of the Spanish banking intermediaries in credit to families and companies Ø Better consciousness of the Spanish executives? q This does not seem a plausible explanation, given what has happened with respect to other assets (real-estate/housing sector) Error in diagnosis and paralysis: liquidity crisis