¡Descarga Tema direccion financiera y más Apuntes en PDF de Administración de Empresas solo en Docsity!

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

Topic 1: An Overview ofCorporate Financing

Chp. 14 , 15 y 25 BREALEY, R.A. y MYERS, S.C. (2003): “Principles of corporatefinancing". 7th ed. McGraw Hill.Chp. 2 y 3 GRINBALTT Y TITMAN (2003) “Financial markets and corporate strategy”McGraw Hill.Chp. 14 ROSS, WESTERFIELD Y JAFFE (2000) ”Corporate Finance”

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

Overview of Corporate Financing �^

Outline:

- Introduction: the main decisions of the firm

1.1 Capital budgeting1.2 Financing decisions

- Financial instruments

2.1 Financial markets2.2 Equity and Debt

- Issuing securities and subscription rights

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

- Introduction: the main decisions of the firm

1.1 Capital budgeting1.2 Financing decisions

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

- Introduction:

What do firms do?

�^

Cash flow scheme between the firm and financial markets: (1)^

External funds obtained from investors (2)^

Funds invested in the firm (3)^

Internal funds generated by the operational activities of the firm (4)^

Internal funds reinvested in the firm (5)^

Funds that remunerate investors^ Operatingactivities

Capitalmarkets

CFO

(2) (3)^

(4)

(1) (5)

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

Classifying the financing sources^ �

Internal funds: �^

Retained earnings

�^

External funds: �^

Shares �^

Common shares �^

Preferred shares �^

Convertibles

�^

Debt �^

Bonds �^

Bank loans �^

Leasings �^

Commercial paper �^

Lines of credit �^

Suppliers

Shares, bonds andcommercial paperare all securitiesand they require toissue a title.

Advantages of using internal funds:1.^

Availability: they do not requireauthorization from investors orissuing new securities

2.^

They do not affect the controlstructure of the firm Disadvantages of using internal

funds:

1.^

They are not free cash. Theseare funds that will not bedistributed to shareholders, sotheir reinvestment should offeran adequate return.

2.^

The willingness not to losecontrol of the company shouldnot lead the company to passup profitable investmentopportunities.

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

- Financial instruments

2.1 Financial markets2.2 Equity and Debt

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

2.1 Financial markets^ �^

Financial markets can be

classified (segmented) in different

ways

:

1.^

According to the moment in the life of the financial instrument;^ �^

Primary market (issues), and Secondary market (transactions)

2.^

According to the maturity of the financial instrument;^ �^

Long term and short term markets

3.^

According to the organization of the markets;^ �^

Stock market (electronic), and outcry market (hand-waving)

4.^

According to the moment when the transaction occurs;^ �^

Spot market, Derivatives market, Futures market

5.^

According to where the issue takes place.^ �^

Domestic market, international market

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

2.2 Shares �^

Shares are tradable financial securities.

�^

Shares may be physical securities (paper is now rare) or electronicregistries.

�^

Title of ownership

in the company

�^

Shareholders have the following rights: �^

Entitled to receive dividends if the firm distributes them; �^

Preferential right to acquire new issues of shares if the share carries a subscription right; �^

Voting rights (not the preferred shares) �^

Choice of the managerial team; Firm’s statutory changes; Boardchanges; Major issues (e.g. mergers).

�^

May

be entitled to the liquidation value of the firm:

�^

Residual claimants (last in terms of priority);

�^

Limited liability (if liquidation value is not enough to cover debts, shareholders are not required to cover the shortfall).

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

2.2 Types of shares^ Shares can be classified:

�^

According to their rights: �^

Common shares:

dividends, liquidation, voting, preferential right to

acquire new shares. �^

Preferred shares

: higher dividends and preferential treatment

�^

Convertible securities:

Securities with an embedded option to be

converted into shares.

�^

When new equity is being issued: �^

Old shares (pre-existing shares) �^

New shares

�^

According to their historic performance: �^

Blue chips: shares from companies with big capitalization andliquidity that have done very well in the past �^

Speculative shares: from high risk companies with low capitalization

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

2.2 Types of shares^ Common shares^ �

Common shares issues: used to start a company or to increase thecapital of a company

Share Nominal Value

VS

Share price

�^

Issued shares are registered at their

Nominal Value

(or Face Value)

�^

Share price

:

�^

Issue at par value: the share price is equal to the nominal value �^

Issue above par value (or at premium): share price at issue is greater than its nominal value �^

Issue below par value (or at a discount): share price is below face value

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

2.2 Types of shares^ Convertible securities^ �

They may be converted into shares, either by decision of its holderor of the issuing company, or both

�^

They do not carry the same rights as shares, instead, they mayinclude some options like: �^

Rights issues: entitle the owner to acquire a pre-determinednumber of shares at a fixed price on or until a pre-determineddate. �^

Warrants: long-term call options to buy underlying shares of theissuer at a pre-specified price. �^

Convertible bonds: bonds which may be converted into shares.

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

Some definitions:

�^

Authorized equity: maximum number of shares that can be issued (determined by shareholders or the companies’ statutes) �^

Shares issued: shares that are held by shareholders �^

Own shares: shares of the firm that have been repurchased by the firm, so not in the market. �^

Earnings before Interest and Taxes (

EBIT)

: income before interest and tax

expenses �^

Net earnings (

NE

) or Net income: income after interest and tax expenses

�^

Dividends (

Div)

: share of the net earnings distributed to shareholders

2.2 Shares

2.2 Shares – Some relationships^ �^

ROE:

�^

Dividendos (Div

):t

�^

Retained earnings

:t

�^

Book Value of Equity (BVE

):t

t

t

t

t

t

t^

Div

NE

BVE

NE

Payout

BVE

BVE

−

=

−

=^

−

−^

1

1

*)

(^1) ( (^1) −

=

t t NE BVE

ROE

t

t^

NE

Payout

Div

=

t

t

t

t^

Div

NE

Payout

NE

−

=

−

=^

)

(^1) (

Earnings

Retained^ Departamento de Economía de la Empresa – Universidad Carlos III de Madrid

Dpto. Economía de la Empresa – Universidad Carlos III de Madrid

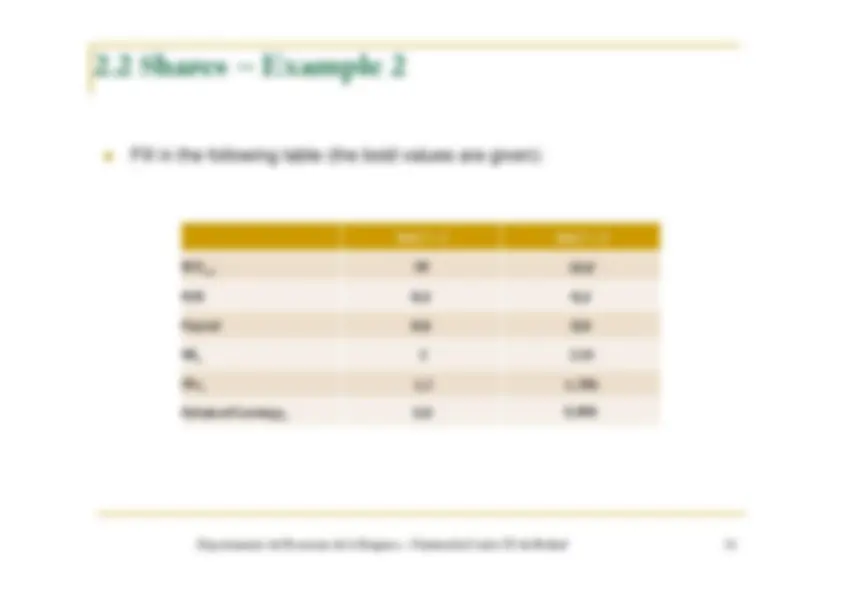

�^

The authorized equity ofcompany GA is 100,000shares. The book value ofequity is as follows: �^

Common shares 40,000 €with face value 0,5€/share �^

Issuance premiums 10,000€ �^

Retained earnings 30,000 € �^

Own capital 80,000 € �^

Own shares (2,000 shr.)5,000€ �^

Book value of equity 75,000€

�^

What is the number ofshares issued? �^

How many shares are therecirculating? �^

How many more shares canthe firm issue withoutpermission from theshareholders? �^

Suppose the firm issues10,000 shares at 2 € pershare. What items in thebalance sheet (ownershipinterests) would change?

2.2 Shares – Example 1