UNIT 4

THE ACCOUNTING

CYCLE

1

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Análisis financiero y contable, Profesor: Luis Fernando Gracia Sarubbi, Carrera: Global Bachelor´s Degree in International Relations, Universidad: UEM

Tipo: Apuntes

1 / 16

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

ACCRUAL BASIS ACCOUNTING

An accountant recognizes the impact of a business

transaction as it occurs

When the business performs a service, makes a

sale, or incurs an expense, the accountant record

the transaction, whether or not cash has been

received or paid

ADJUSTING ENTRIES

Journal entries that are recorded in order

to properly reflect the appropriate

balances in the various ledger accounts

for a specific accounting period.

ACCRUALS

Unrecorded expenses or revenues

and their subsequent adjusting

entries

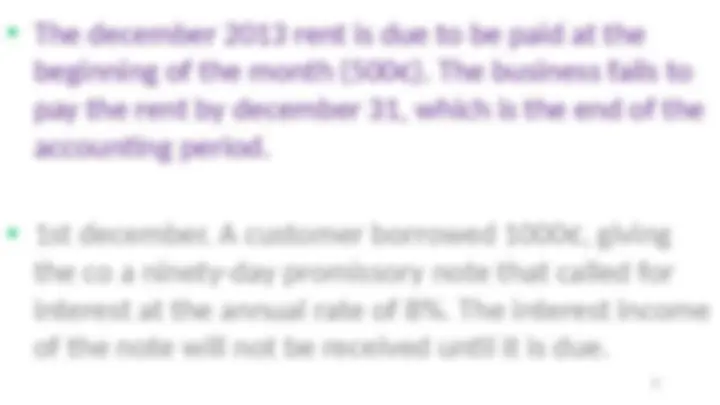

beginning of the month (500€). The business fails to

pay the rent by december 31, which is the end of the

accounting period.

the co a ninety-day promissory note that called for

interest at the annual rate of 8%. The interest income

of the note will not be received until it is due.

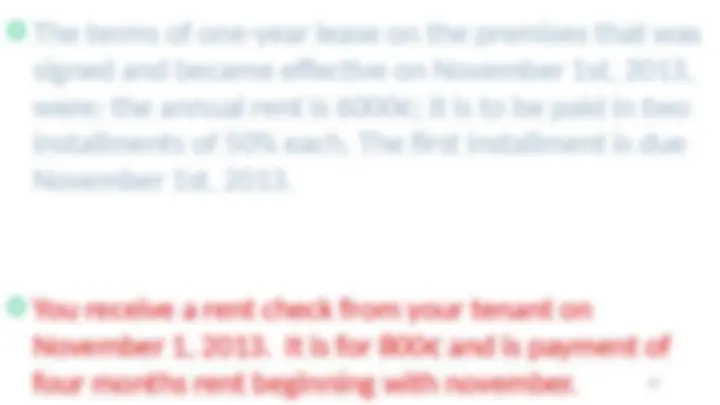

o The terms of one-year lease on the premises that was

signed and became effective on November 1st, 2013,

were: the annual rent is 6000€; it is to be paid in two

installments of 50% each. The first installment is due

November 1st, 2013.

o You receive a rent check from your tenant on

November 1, 2013. It is for 800€ and is payment of

four months rent beginning with november.

10

BREAKDOWN PROCESS OF THE “MERCHANDISE” ACCOUNT

CLOSING ENTRIES: 2) Closing temporary

accounts

It involves transferring the balances of the temporary

accounts to the owner’s equity

Each temporary account must be either debited or credited

to eliminate its balance, while a corresponding debit or

credit is summarized in another temporary account

designed exclusively for that purpose: PROFIT AND LOSS,

INCOME SUMMARY or NET EARNINGS SUMMARY

CLOSING TEMPORARY ACCOUNTS

PROCESS

STEPS IN THE ACCOUNTING CYCLE

Journalize daily business transactions

Post to the various ledger accounts

Calculate the ledger balances

Prepare a trial balance

Record the adjusting entries at the end of the accounting period

Journalize and post closing entries

Prepare financial statements