Scarica Reporting and cost accounting e più Sintesi del corso in PDF di Cost Accounting solo su Docsity!

CHAPTER 1: INTRODUCTION TO MANAGEMENT ACCOUNTING

USERS OF ACCOUNTING INFORMATION

- Managers: for decision-making and control

- Shareholders: value their investment and income derived

- Employees: meet wage demand

- Creditors: meet financial obligations

- Government agencies: collect accounting information 2 categories of users:

- Internal users within organization

- External users (shareholders, creditors….) MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING WHAT IS Is concerned with the provision of information to internal users, to help them make better decisions and improve the efficiency and effectiveness of operations Provision of information to external parties outside the organization LEGAL REQUIREMENTS No (yes if benefits > costs) Yes (statutory requirement for SPA) FOCUS ON Segments of firm Total firm ACCOUNTING PRINCIPLES No (information for internal purposes decision-making, planning and control) Yes (standard financial statements) TIME DIMENSION Future information Past information REPORT FREQUENCY Daily, weekly or monthly (for fast decisions) Annually (and semi-annually)

DECISION-MAKING PROCESS

- IDENTIFYING OBJECTIVES (maximize profits in theory) Specify the company’s goals or organizational objectives as satisfactory profits, build an empire, security, high quality products or being market leader

- THE SEARCH FOR ALTERNATIVE COURSES OF ACTION (strategies) (most important stage) The company should consider one or more courses of action:

- Developing new products for sale in existing markets

- Developing new products for new markets

- Developing new markets for existing products

3) SELECT APPROPRIATE ALTERNATIVE COURSES OF ACTION

Data about:

- The potential growth rates of the alternative activities under consideration

- The market share the company is likely to achieve

- Projected profits for each alternative activity

- IMPLEMENTATION OF DECISIONS Using the budget financial plan to implement decisions of management and communicate to everyone in the organization

- COMPARING ACTUAL AND PLANNED OUTCOMES Performance reports compare actual with planned provide feedback information

- RESPONDING TO DIVERGENCIES FROM PLAN This process represents the application of management by exception corrective action is taken

FACTORS THAT HAVE INFLUENCED THE CHANGES IN THE COMPETITIVE

ENVIRONMENT

a. Globalization of world trade b. Privatization of government-controlled companies and deregulation in various industries c. Changing of customer tastes d. Emergence of e-business

KEY SUCCESS FACTOR ON WHICH ORGANIZATIONS MUST CONCENTRATE

i) COST EFFICIENCY

Strong competitive advantage More accurate cost information Analyse profits by products, sales outlets, customers and markets

ii) QUALITY

Customers demand high quality products and services

iii) TIME AS COMPETITIVE WEAPON

Cycle time:

- processing time value added activity

- move time

- wait time non-value added activities

- inspection time

iv) INNOVATION AND COINTINUOS IMPROVEMENT

Develop a steady stream of innovative new products and services and have the capability to rapidly adapt to changing customer requirements

v) SOCIAL RESPONSIBILITY AND CORPORATE ETHICS

- Integrity (not being a party to any falsification)

- Objectivity (not being biased or prejudiced)

- Confidentiality and professional competence and due care (maintaining skills required to ensure a competent professional service)

CHAPTER 2: AN INTRODUCTION TO COST TERMS AND CONCEPTS

COST OBJECTS

Cost object is any activity for which a separate measurement of costs is desired if the users of accounting information want to know the cost of something, this something is called a cost object Cost collection system typically accounts for costs in 2 broad stages: 1 - It accumulates costs by classifying them into certain categories such as by type of expense (direct labour, direct materials and indirect costs) or by cost behaviour (fixed and variable costs) 2 - It then assigns these costs to cost objects

DIRECT AND INDIRECT COSTS

Costs that are assigned to cost objects can be divided into 2 broad categories direct (materials and labour costs) indirect (materials and labour costs)

DIRECT MATERIALS

Material costs that can be specifically and exclusively identified with a particular cost object Physical observation to measure the quantity consumed by each individual product or service and the cost of direct materials can be directly charged to them

DIRECT LABOUR

Labour costs that can be specifically and exclusively identified with a particular cost object Physical observation to measure the quantity of labour used to produce a specific product It includes the cost of converting the raw materials

INDIRECT COSTS

Cannot be identified specifically and exclusively with a given cost object Consist of indirect labour, materials and expenses Where products are the cost object the wages of all employees whose time cannot be identified with a specific product represent indirect labour costs Examples of indirect expenses lighting and heating expenses and property taxes Overheads = indirect In a manufacturing organization 3 types of overhead costs : a. manufacturing o. all the costs of manufacturing apart from direct labour and material costs b. administrative o. costs associated with general administration that cannot be assigned to other 2 categories c. marketing o. are necessary to market and distribute a product or service (order-getting and order-filling costs) Prime cost consist of all direct manufacturing costs (sum of direct material and direct labour costs) Conversion cost is the sum of direct labour and manufacturing overhead costs cost of converting raw materials into finished products

DISTINGUISHING BETWEEN DIRECT AND INDIRECT COSTS

- direct costs treated as indirect because it is not effective to trace costs directly to the cost object

- distinction direct-indirect depends on the cost object

ASSIGNING DIRECT AND INDIRECT COSTS TO COST OBJECTS

Direct cost can be traced easily and accurately to a cost objects Where products are the cost object, direct materials and labour used can be physically identified with the different products that an organization produces indirect cost cannot be traced to cost objects an estimated must be made of the resources consumed by cost objects using cost allocations Is the process of assigning costs when a direct measure does not exist for the quantity of resources consumed by a particular cost object. Cost allocations involve the use of surrogate rather than direct measure.

PERIOD AND PRODUCT COSTS

Product costs :

- goods purchased or

- produced for resale

- in a manufacturing organization, they are costs that accountant attaches to the product and that are included in the inventory valuation for finished goods, or for a partly completed goods (work in progress), until they are sold then recorded as expenses and matched against sales for calculating profit Period costs :

- costs not included in the inventory valuation treated as expenses

- hence no attempt is made to attach period costs to products for inventory valuation purposes in a manufacturing organization: ➢ all manufacturing costs are regarded as product costs ➢ non-manufacturing costs are regarded as period costs

COST BEHAVIOUR

How costs and revenues will vary with different levels of activity Variable costs vary in direct proportion to the volume of activity total variable costs are linear and unit variable costs is constant Fixed costs Remain constant over wide ranges of activity for a specified time period not affected by changes in activity For decision-making, it is better to work with total fixed costs rather than unit costs

CHAPTER 3: ACCOUNTING FOR DIRECT COSTS

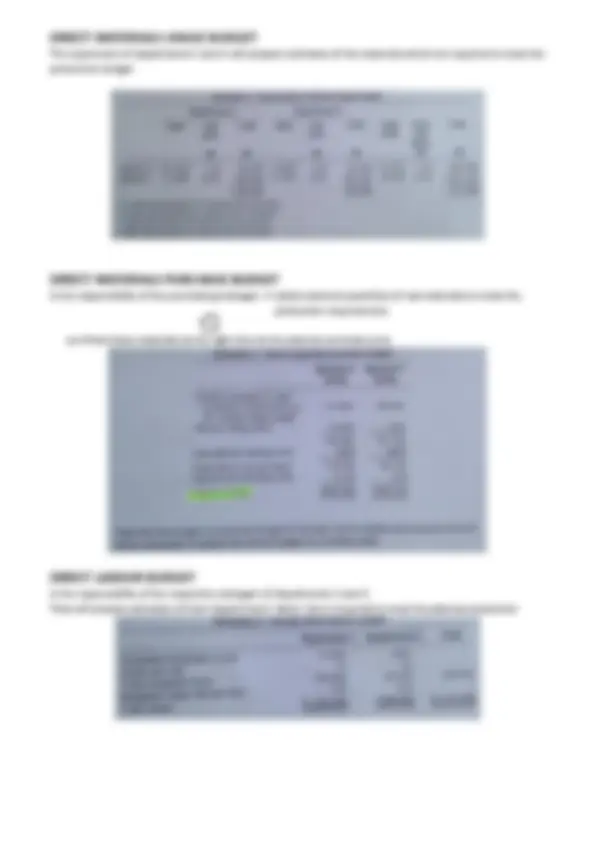

ACCOUNTING TREATMENT OF VARIOUS LABOUR COST ITEMS

HOLIDAY PAY

❖ Normally regarded as direct ❖ Should be charged to activities by means of an inflated hourly rate ❖ Holiday pay is treated as a direct labour cost

OVERTIME PREMIUMS AND SHIFT-WORK PREMIUMS

I. Are included as part of overheads or II. If they are a direct result of a customer’s urgent request charged directly to the customer

OTHER EMPLOYMENT COSTS

➢ Include the employer’s share of National Insurance contributions and pension fund contributions ➢ It is preferable to calculate an average hourly rate for employment costs and add this to the hourly wage rate paid to the employees

MATERIALS RECORDING PROCEDURE

The cost of direct materials represented the dominant costs in manufacturing organizations averaging 51% of total costs for the responding organizations within the manufacturing sector Stages of recording procedure:

1. STORAGE OF MATERIALS

When items of m. have reached their re-order point, a purchase requisition is initiated requesting the purchase department to obtain the re-order quantity from an appropriate supplier

2. PURCHASE OF M.

Purchase order requesting that the supplier supply the materials listed on the order

3. RECEIPT OF M.

The receiving section the lists the materials received on a goods received note (GRN) source document for the stores ledger account

4. ISSUE OF M.

Store requisition list type and quantity of materials issued

5. ASSIGNING THE COST OF M. TO COST OBJECTS

Details on the material requisition represent the source of information to assign costs a. Reducing the value of raw materials stocks by recording the values issued in the issues column of the appropriate stores ledger account b. Assigning the cost of the issues to the appropriate customer’s order number, product/service code or overhead account

PRICING THE ISSUES OF MATERIALS

Cost of the single material varies during time it is required to use a method for evaluation: 1 - FIFO the first item received was the first item to be issued Most logical method physical flow of materials 2 - LIFO not accepted method of pricing in the UK (taxation purposes) 3 - AVERAGE COST each of the items are issued at the average cost per unit

ISSUES RELATING TO ACCOUNTING FOR MATERIALS

1) TREATMENT OF STORE LOSSES

To achieve accurate profit measurement, there must be a complete periodic stockcount (or continuous stocktaking) all the stores items are counted at one point sample of store items being counted regularly on a in time, which can disrupt production daily basis, and is less disruptive Why actual stock level is different from computer records:

- An entry in the wrong stores ledger account

- Items in the wrong physical location

- Arithmetical error when a manual system is operating

- Theft of stock

2) TREATMENT OF MATERIALS DELIVERY COSTS

3 cases: a. materials can be charged directly to cost object b. materials can be apportioned using value or weight and then directly assigned to cost object c. materials can be charged to an overhead account

3) TREATMENT OF MATERIALS HANDLING COSTS

It refers to the expenses involved in:

- receiving m

- storing m

- issuing m

- handling m Charge the costs to materials handling overhead account and allocate these costs to cost objects Some company establish a separate materials handling rate

CONTROL OF STOCKS (quantitative models)

Investments in stocks represents a major asset of most industrial and commercial organizations A firm should determine its optimum level of investment in stocks, based on 2 factors: i. stocks are sufficient to meet the requirements of production and sales ii. avoid holding surplus stocks Holding costs

- opportunity cost of investment in stocks (applicable only to costs that vary with number of units)

- incremental insurance cost

- incremental warehouse and storage costs

- incremental material handling costs

- cost of obsolescence and deterioration of stocks the relevant holding costs for use in quantitative models should include only those items that will vary with the levels of stocks Ordering costs Usually consist of the clerical costs of:

- preparing purchase orders

- receiving deliveries

- paying invoices ordering costs that are common to all stock decision are not relevant, and only the incremental costs of placing an order are used in formulating the quantitative models. The costs of acquiring stock through buying or manufacturing are not a relevant cost to be included in the quantitative models

CONTROL OF STOCKS THROUGH CLASSIFICATION ABC method

Requires that an estimate be made of the total purchase cost for each item of stock for the period. The sales forecast is used for estimating the quantities of each item of stock to be purchased during the period. Each item is then grouped in decreasing order of annual purchase cost: The top 10% of items in stock in terms of annual purchase cost are categorized as A ITEMS the next 20% as B ITEMS the final 70% as C ITEMS

JUST-IN-TIME

Aim to eliminate non-value-added activities (where there is an opportunity for cost reduction without reducing the customer’s perceived usefulness of a product or service) By significantly reducing set-up times, smaller production batches and the purchase of smaller batch sizes become economical Many companies have developed strategic supply partnerships involving JIT The overall impact of adopting this approach is that the EOQ declines

MATERIALS REQUIREMENT PLANNING (MRP)

- complex manufacturing environments

- integrated system

- link with ERP systems

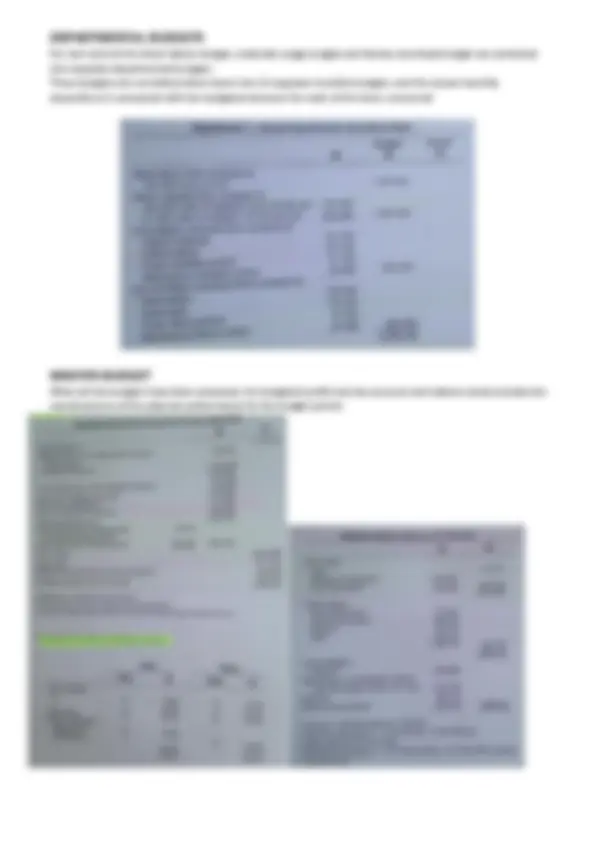

CHAPTER 4: COST ASSIGNMENT FOR INDIRECT COSTS

ASSIGNMENT OF:

DIRECT COSTS INDIRECT COSTS

Can be accurately traced to cost objectives, because they can be specifically and exclusively traced to a particular cost object Cannot be traced as direct Cost tracing method Cost allocation methods (the basis that is used to allocate costs to cost objectives is called allocation base or cost driver) Cause-and-effect allocations (where allocation bases are significant determinants of the costs) Arbitrary allocation (is not a significant determinant of its cost)

ACTIVITY-BASED-COSTING SYSTEM TRADITIONAL COSTING SYSTEM

DIFFERENT COSTS FOR DIFFERENT PURPOSES

Manufacturing organizations assign costs to products for 2 purposes:

- for internal profit measurement and for external financial accounting requirements

- inventories should be valued at manufacturing cost

- not necessary to accurately assign costs to individual products

- To provide useful information for managerial decision-making requirements

- non-manufacturing costs must be taken into account and assigned to products

- more accurate product cost assignment are required

COST-BENEFIT ISSUES AND COST SYSTEM DESIGN

TRADITIONAL SYSTEMS

Depends on level of sophistication <---------------------->

- - + +

ABC SYSTEMS

Simplistic Sophisticated

- Inexpensive to operate

- Extensive use of arbitrary cost allocations

- Low levels of accuracy

- High cost of errors

- Expensive to operate

- Extensive use of cause-and-effect cost allocations

- High levels of accuracy

- Low costs of errors

4) ASSIGNING COST CENTRE OVERHEADS TO PRODUCTS OR OTHER CHOSEN COST OBJECTS

TRADITIONAL VS ABC SYSTEMS

TRADITIONAL COSTING SYSTEM

In the first stage: it allocates overheads to production and service cost centres (typically departments) and then reallocates service cost centre/department costs to the production departments. Normally cost centres consist of departments, but in some cases they consist of smaller segments. In the second stage: Allocates costs from cost centres (pools) to products or other chosen cost objects. TCS trace overheads to products using a small number of second stage allocation bases (overhead allocation rates) which vary directly with volume produced direct labour and machine hours

ABC SYSTEM

In the first stage: Assigns overheads to each major activity; many activity-based cost centres (or activity cost pools) are established, whereas with traditional systems overheads tend to be pooled by departments, although they are normally described as cost centres. Normally has a greater number of cost centres. In the second stage: Use the term cost driver is a measure that exerts the major influence on the cost of a particular activity. Use many different types of second-stage cost drivers, including non-volume-based drivers, such as the number of production runs for producing scheduling and the number of purchase orders for the purchasing activity. Characteristics of ABC systems:

- Greater number of cost centres

- Greater number and variety of second stage cost drivers Can more accurately measure the resources consumed by cost objects

EXTRACTING RELEVANT COSTS FOR DECISION-MAKING

For decision-making, non-manufacturing costs should also be taken into account Some of the costs that have been assigned to the products may not be relevant for certain decisions Relevant if gives information to choose selling price irrelevant if these costs are unaffected by a decision

BUDGETED OVERHEAD RATES

If monthly overhead rates are used, some costs (heating and lighting) will not be allocated fairly to units of output normal product cost based on average long-term production rather than actual product cost budgeted overhead rate based on annual estimated overhead expenditure and activity

UNDER AND OVER RECOVERY OF OVERHEADS

There is a under-or over-recovery of overhead when actual activity or overhead expenditure is different from the budgeted overheads and activity used to estimate the budgeted overhead rate. Accounting regulations in most countries recommend that the under-or over-recovery of overheads should be regarded as a period cost adjustment

NON-MANUFACTURING OVERHEADS

Some non-manufacturing overheads costs may be a direct cost of the product. The problem is that cause-and-effect allocation bases often cannot be established for non-manufacturing overheads. Allocating non-manufacturing costs to products on the basis of their manufacturing costs: 𝐞𝐬𝐭𝐢𝐦𝐚𝐭𝐞𝐝 𝐧𝐨𝐧 𝐦𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐨𝐯𝐞𝐫𝐡𝐞𝐚𝐝 𝐞𝐬𝐭𝐢𝐦𝐚𝐭𝐞𝐝 𝐦𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐜𝐨𝐬𝐭

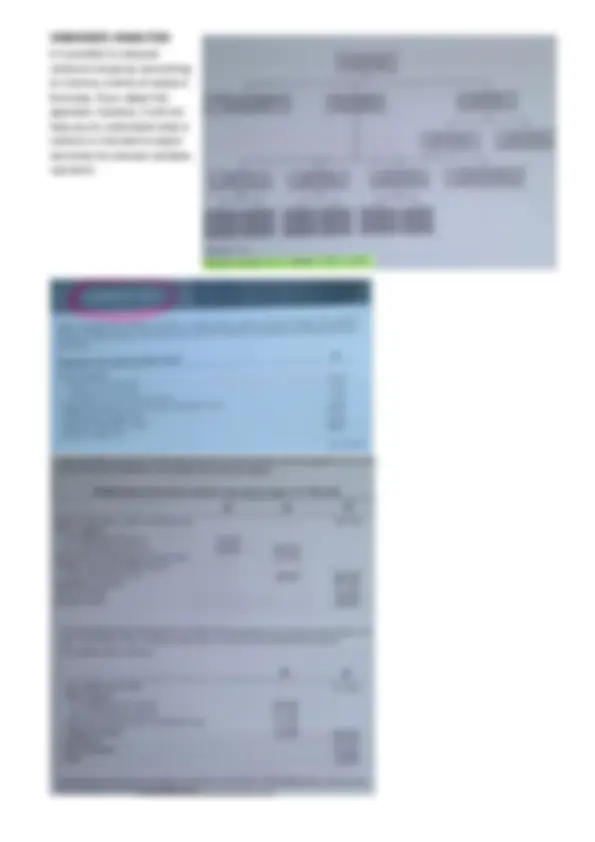

Break-even chart

CONTRIBUTION GRAPH

Fixed costs are represented by the difference between the total cost line and the variable cost line. The advantage of this form of presentation is that it emphasizes the total contribution, which is represented by the difference between the total sales revenue line and the total variable cost line.

PROFIT-VOLUME GRAPH

Is a more convenient method of showing the impact of changes in volume on profit. The horizontal axis represents the various levels of sales volume, and the profits and losses for the period are recorded on the vertical scale. Profit or losses are plotted for each of the various sales levels, and these points are connected by a profit line

MULTI-PRODUCT COST-VOLUME-PROFIT ANALYSIS

➢ If all the fixed costs are directly attributable to products apply the analysis separately to each product ➢ If there are common fixed costs convert the sales volume measure of the individual products into standard batches of products based on the planned sales mix

COST-VOLUME-PROFIT ANALYSIS ASSUMPTIONS

1) ALL OTHER VARIABLES REMAIN CONSTANT

Volume is the only factor that will cause costs and revenues to change If significant changes in other variables occur, the CVP analysis presentation will be incorrect

2) SINGLE PRODUCT OR CONSTANT SALES MIX

3) TOTAL COSTS AND TOTAL REVENUE ARE LINEAR FUNCTIONS OF OUTPUT

Unit variable cost and selling price are constant within the relevant range of production

4) PROFITS ARE CALCULATED ON A VARIABLE COSTING BASIS

Fixed costs incurred during the period are charged as an expense for that period variable-costing profit calculations are assumed

5) COST CAN BE ACCURATELY DIVIDED INTO THEIR FIXED AND VARIABLE ELEMENTS

The separation of semi-variable costs into their fixed and variable elements is extremely difficult a reasonably accurate analysis is necessary if CVP analysis is to provide relevant information for decision-making

6) ANALYSIS APPLIES ONLY TO THE RELEVANT RANGE

It is incorrect to project cost and revenue figures beyond the relevant range

7) ANALYSIS APPLIES ONLY TO A SHORT-TERM TIME HORIZON

It is inappropriate to extend the analysis to long-term decision-making

THE IMPACT OF INFORMATION TECHNOLOGY

Sensitivity analysis is one approach for coping with changes in the values of the variables. It focuses on how a result will be changed if the original estimates or the underlying assumptions change Development in information technology have enabled management accountants to build CVP computerized models Quicker reactions to changes

TESTS OF RELIABILITY

Various tests of reliability can be applied to see how reliable potential cost drivers are in predicting the dependent variable Coefficient of variation (r^2 ) , also known as the coefficient of determination and is the square of the correlation coefficient (r) r represents the degree of association between two variables, such as cost and activity. If the degree of association between two variables is very close it will be almost possibile to plot the observations on a straight line, and r and r^2 will be very near to 1

SUMMARY OF THE STEPS INVOLVED IN ESTIMATING COST FUNCTIONS

A. SELECT THE DEPENDENT VARIABLE Y (THE COST VARIABLE) TO BE PREDICTED

The choice of the cost (or costs) to be predicted will depend upon the purpose of the cost function. If the purpose is to estimate the indirect costs of a production or activity cost centre, then all indirect costs associated with the production ( activity centre ) that are considered to have the same cause- effect relationship with the potential cost drivers should be grouped together. In some situations, it may be necessary to establish more than one cost function. For example, if certain overheads are considered to be related to performing production set-ups and others are related to machine running hours, then it may be necessary to establish two cost pools (centres): one for set-up-related costs and another one for machine-related costs. A separate cost function would be established for each cost pool.

B. SELECT THE POTENTIAL COST DRIVERS

As direct labour hours, machine hours, direct labour cost, number of units of output, number of orders processed and weight of materials

C. COLLECT DATA ON THE DEPENDENT VARIABLE AND COST DRIVERS

Necessary a number of past observations; data adjusted for changes

D. PLOT THE OBSERVATIONS ON A GRAPH

E. ESTIMATE THE COST FUNCTION

F. TEST THE RELIABILITY OF THE COST FUNCTION

Cost functions should be not derived solely on the basis of observed past statistical relationships. Instead, they should be used to confirm or reject beliefs that have been developed from a study on the underlying process. EXERCISES

HIGH-LOW METHOD

VOLUME OF PRODUCTION MAINTEINANCE COSTS

Lowest activity 5000 22000 Highest activity 10000 32000 5000 10000 variable cost per unit = difference in cost / difference in activity To find fixed costs: (total cost) – (variable cost per unit)*(activities)

CHAPTER 11: MEASURING RELEVANT COSTS AND REVENUES FOR

DECISION-MAKING

(page 257)

Relevant costs are future costs that differ between alternatives Irrelevant costs consist of sunk costs, allocated costs and future costs that do not differ between alternatives

IMPORTANCE OF QUALITATIVE FACTORS

Those factors that cannot be expressed in monetary terms are classified as qualitative factors (example might be the decline in employee morale) It is essential that qualitative factors be brought to the attention of management during the decision-making process.

SPECIAL PRICING DECISIONS

Special price decisions relate to pricing decisions outside the main market. Typically they involve one-time only orders or orders at a price below the prevailing market price. From example 11.1 (pag 260), 4 important factors must be considered before recommending acceptance of the order: ➢ It is assumed that the future selling price will not be affected by selling some of the output at a price below the going market price ➢ The decision to accept the order prevents the company from accepting other orders that may be obtained during the period at the going price ➢ It is assumed that the company has unused resources that have no alternative uses that will yield a contribution to profits in excess of 135.000 per month ➢ It is assumed that the fixed costs are unavoidable for the period under consideration

EVALUATION OF A LONG-TERM ORDER

In the longer term, however, it may be possible to reduce capacity and spending on fixed costs and direct labour. The costs and revenues are relevant to the decision because some of the costs that were fixed in the short term could be changed in the longer term

PRODUCT MIX DECISIONS WHEN CAPACITY CONSTRAINTS EXIST

When sales demand is more than a company’s productive capacity, the resources responsible for limiting the output should be identified. These scare resources are known as limiting factors. Within a short-term time, it is unlikely that constraints can be removed and additional resources acquired. When limiting factors apply, profit is maximized when the greatest possible contribution to profit is obtained each time the scarce or limiting factor is used. It is important that you remember that the approach outlined in this section applies only to those situations where capacity constraints cannot be removed in the short term. In the longer term, additional resources should be acquired if the contribution from the extra capacity exceeds the cost of acquisition.