Scarica COST ACCOUNTING HANDOUTS e più Schemi e mappe concettuali in PDF di Cost Accounting solo su Docsity!

LESSON# 1

COST CLASSIFICATION AND COST BEHAVIOR

INTRODUCTION

Cost Accounting Cost Accounting is an expanded phase of financial accounting which provides management promptly with the cost of producing and/or selling each product and rendering a particular service.

Management Accounting Management accounting is application of professional knowledge and skill in the preparation and presentation of financial information in such a way as to assist management in decision making and in the planning and control of operations of the entity

Objectives Objective of cost accounting is computation of cost per unit, whereas the objective of management accounting is to provide information to the management for decision making purposes.

Users of Cost Accounting Users of cost & management accounting are the decision makers and the managers of the entity/organization for which all this exercise is undertaken.

Uses of Cost and Management Accounting

- It determines total cost of production and cost of sales

- It determines appropriate selling price

- It discloses the profitable products, areas and activity/capacity levels

- It is used to decide whether to manufacture or purchase for outside

- It helps in planning and controlling the cost of production

Elements of Cost Any product that is manufactured is the result of consumption of some resources. The management, for its planning and controlling functions, must know the cost of using these resources. The constituent elements of cost are broadly classified into three distinct elements: 1 Direct Material Cost 2 Direct Labor Cost 3 Other Production Cost a) Direct Cost b) Indirect Cost

COST CLASSIFICATION Elements of cost (Direct Material, Direct Labor, Other Production costs) can be classified as direct cost or indirect cost.

Direct Cost A direct cost is a cost that can be traced in full to the product or service for which cost is being determined. Costs that can be economically identified with a specific saleable product or service (cost unit).

a) Direct material costs are the costs of materials that are known to have been used in

producing and selling a product or rendering a service.

b) Direct labor costs are the specific costs of the workforce used to produce a product or

rendering a service.

c) Other direct production costs are those expenses that have been incurred in full as a

direct consequence of producing a product, or rendering a service.

Indirect Cost/Overhead Cost An indirect cost or overhead cost is a cost that is incurred in the course of producing product or rendering service, but which cannot be traced in the product or service in full. Expenditure incurred on labor, material or other services which cannot be economically identified with a specific cost product or service (cost unit). Examples include: Wages of supervisor, cleaning material, workshop insurance.

Material Cost Labor Cost Other Production Cost Total Production Cost

Direct Direct Direct Prime Cost

Indirect Indirect Indirect Factory Overhead Cost

1. Prime Cost Direct Material +Direct Labor +Other direct production cost Prime cost. 2. Total Production Cost Prime Cost +Factory overhead cost Total production cost. 3. Conversion Cost Direct labor cost +Factory overhead cost Conversion cost.

COST BEHAVIOR

Cost behavior is the way in which total production cost is affected by fluctuations in the activity (production) level.

Activity level The activity level refers to the amount of work done, or the number of events that have occurred. Depending on circumstances, the level of activity may refer to the volume of production in a period, the number of items sold, the value of items sold, the number of invoices issued, the number of invoices received, the number or units of electricity consumed, the labor turnover etc. etc. Basic principle The basic principle of cost behavior is that as the level of activity rises, costs will usually raise. For example; it will cost more to produce 500 units of output than it will cost to produce 100 units; it will usually cost more to travel 10 km than to travel 2 km. Although the principle is based on the common sense, but the cost accountant has to determine, for each cost elements, whether which cost rises by how much by the change in activity level.

Further division of cost behavior

- Step fixed cost

- Semi variable cost

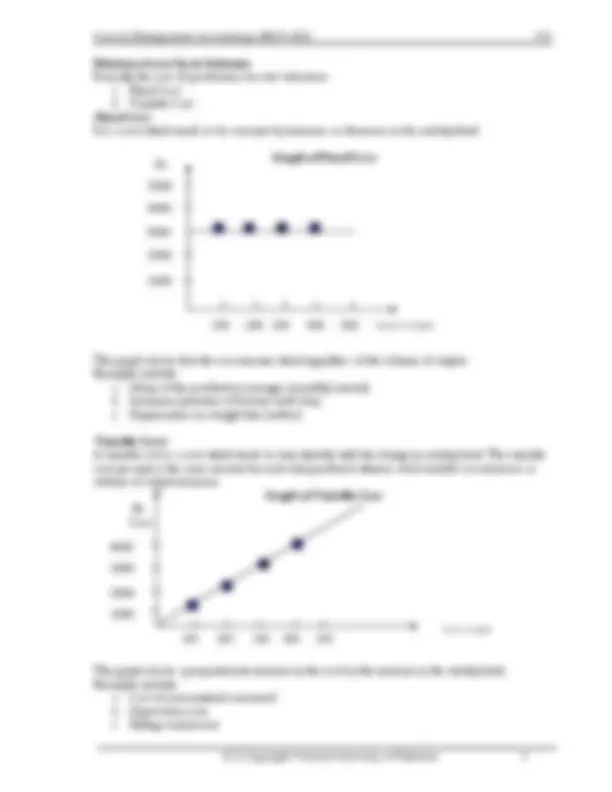

Step fixed cost

A step fixed cost is the cost which is constant for a specific range of activity and rises to a new constant level once the range exceeds. The range over which the fixed cost remains constant is known as the relevant range. For example; the depreciation of a machine may be fixed if production remains below 100 number of units per month, but if the production exceeds 100 number of units, a second machine may now be required, and the cost of depreciation would go up a step. Other examples include: a. Rent of workshop (in case of increase in the production one needs to rent one more workshop) b. Salary of supervisor (increase in output will be supervised by increased number of supervisors) Graph of Step fixed Cost

Rs. Cost

Units

Volume of output

This graph shows a stepwise increase in the total cost. Relevant range in this graph is of 100 numbers of units.

Semi Variable Cost

It is also known as mixed cost. It is the cost which is part fixed and par variable. It is in fact the mixture of both behaviors. Examples include: Utility bills – there is a fixed line rent plus charges for units consumed. Salesman’s salary – there is a fixed monthly salary plus commission per units sold. The graph of semi variable cost is as follow:

Rs. Cost

Volume of output

Variable cost portion

Fixed cost portion

This graph shows a fixed cost of Rs. 2,000 and there after the cost is variable.

COST BEHAVIOR PER UNIT OF PRODUCTION Cost Behavior Per unit of production

Cost per unit behaves differently than the total cost of production. Following tables show the difference in behavior.

Increasing Production Volume Situation

Decreasing Production Volume Situation

Per Unit Total Fixed Cost Increase Constant Variable Cost Constant Decrease Total Cost Increase Decrease

Increase or decrease in production volume causes no change to the variable cost per unit it remains constant, assuming there is not rebate in case of bulk purchase and the labor receives constant rate despite change in production volume. Whereas, increase in production volume causes a decrease in fixed cost per unit and in the same way a decrease in production volume causes an increase in fixed cost per unit. Following example helps understanding this concept.

Total fixed cost = Rs. 4, Per unit variable cost = Rs. 3 Cost per unit at different activity levels 1000, 2000, 4000, and 5000 units

1000 units 2000 units 4000 units 5000 units Rs. Per Unit

Total Rs. Rs. Per Unit

Total Rs. Rs. Per Unit

Total Rs. Rs. Per Unit

Total Rs.

Fixed Cost 4 4,000 2 4,000 1 4,000 0.8 4, Variable Cost 3 3,000 3 6,000 3 1,200 3 15, Total Cost 7 7,000 5 10,000 4 16,000 3.8 19,

Sunk Cost Sunk cost is the cost expended in the past that cannot be retrieved on product or service.

Example

The entity purchase stationary in bulk last moth. This expense has been incurred and hence will not be relevant to the management decisions to be taken subsequent to the purchase.

Opportunity Cost Opportunity cost is the value of a benefit sacrificed in favor of an alternative.

Example

An investor invests in stock exchange he foregoes the opportunity to invest further in his hotel. The profit which the investor will be getting from the hotel is opportunity cost.

Product Cost Product cost is a cost that is incurred in producing goods and services. This cost becomes part of inventory.

Example

Direct material, direct labor and factory overhead.

Period Cost The cost is not related to production and is matched against on a time period basis. This cost is considered to be expired during the accounting period and is charged to the profit & loss account.

Example

Selling and administrative expenses

Historical Cost It is the cost which is incurred at the time of entering into the transaction. This cost is verifiable through invoices/agreements. Historical cost is an actual cost that is borne at the time of purchase.

Example

A building purchased for Rs 400,000, has market value of Rs. 1,000,000. Its historical cost is Rs. 400,000.

Standard Cost Standard cost is a Predetermine cost of the units.

Example

Standard cost for a unit of product ‘A’ is set at Rs 30. It is compared with actual cost incurred for control purposes.

Implicit Cost Implicit cost imposed on a firm includes cost when it foregoes an alternative action but doesn't make a physical payment. Such costs are related to forgone benefits of any single transaction, and occur when a firm:

Example

Uses its own capital or Uses its owner's time and/or financial resources

Explicit Cost Explicit cost is the cost that is subject to actual payment or will be paid for in future.

Example

Wage Rent Materials

Differential Cost or Incremental cost It is the difference of the costs of two or more alternatives.

Example

Difference between costs of raw material of two categories or quality.

Costing: The measurement of cost of a product or service is called costing; however, it is not a recommended terminology.

Cost Accounting: It is the establishment of budgets, standard cost and actual costs of operations, processes, activities or products and the analysis of variances, profitability or social use of funds. It involves a careful evaluation of the resources used within the business. The techniques employed are designed to provide financial information about the performance of a business and possibly the direction which future operations should take.

Prime Cost: The total costs which can be directly identified with a job, a product or service is known as Prime cost. Thus prime cost = direct materials + direct labor + other direct expenses.

Conversion Cost. This is the total cost of converting the raw materials into finished products. The total of direct labor other direct expenses and factory overhead cost is known as conversion cost

Cost Accumulation Cost accumulations are the various ways in which the entries in a set of cost accounts (costs incurred) may be aggregated to provide different perspectives on the information.

Methods o cost accumulation f

Process costing It is a method of cost accounting applied to production carried out by a series of operational stages or processes. Job order costing Generally, it is the allocation of all time, material and expenses to an individual project or job.

- Cost accounting concepts include all of the following except a Planning b Controlling c Sharing d Costing

- The three elements of product cost are all but a Direct material cost b Factory overhead cost c Indirect labor cost d Direct labor cost

Answers:

Q1 Q2 Q3 Q4 Q5 Q6 Q

c d b c c c c

LESSON#

IMPORTANT TERMINOLOGIES

Cost Unit It is a unit of a product or service in relation to which the cost is ascertained, i.e. it is the unit of the out put or product of the business. In simple words the unit for which cost of producing the units is identified /allocated.

Example

¾ Ball point for a Ball point manufacturing entity ¾ Bottle for Beverage producing entity ¾ Fan for a Fan manufacturing entity

Cost Center Cost centre is a location where costs are incurred and may or may not be attributed to cost units.

Examples

¾ Workshop in a manufacturing concern ¾ Auto service department ¾ Electrical service department ¾ Packaging department ¾ Janitorial service department

Revenue Centre It is part of the entity that earns sales revenue. Its manager is responsible for the revenue earned not for the cost of operations.

Examples

Sales department Factory outlet

Profit Centre Profit centre is a section of an organization that is responsible for producing profit.

Examples

A branch A division

Investment Centre An investment centre is a segment or a profit centre where the manager has significant degree of control over his/her division’s investment policies.

Examples

A branch A division

Relevant Cost Relevant cost is which changes with a change in decision. These are future costs that effect the current management decision.

Examples

Variable cost Fixed cost which changes with in an alternatives Opportunity cost

Irrelevant Cost

Explicit Cost Explicit cost is the cost that is subject to actual payment or will be paid for in future.

Example

Wage Rent Materials

Differential Cost or Incremental cost It is the difference of the costs of two or more alternatives.

Example

Difference between costs of raw material of two categories or quality.

Costing: The measurement of cost of a product or service is called costing; however, it is not a recommended terminology.

Cost Accounting: It is the establishment of budgets, standard cost and actual costs of operations, processes, activities or products and the analysis of variances, profitability or social use of funds. It involves a careful evaluation of the resources used within the business. The techniques employed are designed to provide financial information about the performance of a business and possibly the direction which future operations should take.

Prime Cost: The total costs which can be directly identified with a job, a product or service is known as Prime cost. Thus prime cost = direct materials + direct labor + other direct expenses.

Conversion Cost. This is the total cost of converting the raw materials into finished products. The total of direct labor other direct expenses and factory overhead cost is known as conversion cost

Cost Accumulation Cost accumulations are the various ways in which the entries in a set of cost accounts (costs incurred) may be aggregated to provide different perspectives on the information.

Methods o cost accumulation f

Process costing It is a method of cost accounting applied to production carried out by a series of operational stages or processes. Job order costing Generally, it is the allocation of all time, material and expenses to an individual project or job.

Assignment Questions

Answer to each of the following question should not exceed five lines.

- Define Cost Accounting

- What are the three broad elements of cost?

- Give any five examples of factory overhead cost. Also explain.

- Give any two examples of distribution overheads.

- Give any two examples of office overheads

- Define direct cost and give two examples.

- What is indirect cost? Give three examples.

- What is meant by step fixed cost and semi-variable cost? Also show graphs.

- What is fixed cost? Give three items of fixed cost, also show its graph.

Exam Type Questions

- What is a cost unit? Give two example

- Define cost centre. How does it differ from cost unit

- What is the difference between direct and indirect materials? Give two examples of each.

- Fixed cost per unit remains fixed. Do you agree?

- How variable cost per unit behaves? Give two examples.

- What are semi-variable costs? Draw graph for such costs

Costing department of these entities works very much efficiently, a complete cost accounting system is followed in manufacturing concerns in which procedures of cost accumulation, methods of product costing, process of calculating per unit cost and determining the cost of inventories are defined.

Trading Entities Trading entities purchase and then sell tangible products without changing their basic form. Costing department of these entities is not involved in that much minute calculations and procedures. It simply has to keep records of the cost of goods purchased and cost of inventory.

Servicing Entities Servicing entities provide services or intangible products to their customers. Costing department of these entities is also concerned with calculation of the cost of service provided. Inventory of service is also determined in this type of concerns.

Inventory It is the cost held in material & supplies, work in process and finished goods that will provide economic benefits in future, it is also known as stock. Adjustment for inventories is pivotal in calculation of cost of goods sold. The basic reason for its adjustment is that profit and loss account is prepared on the basis of accrual concept. Adjustments of opening and closing inventories in the cost of production (for manufacturing entities), cost of purchases (for trading entities) is essential to match the cost with its revenue.

For manufacturing entities inventories are classified into three categories:

- Material and supplies inventory

- Work in process inventory

- Finished goods inventory Following is a self explanatory chart for different categories of inventories.

LOCATIONS

Inventory

Manufacturing Trading Services

Material & supplies Inventory

Finish Goods Inventory

Work In Process Inventory

Purchased Goods Inventory

Work In Process Inventory

Showroom/ Godown

Godown/ Store Work-shop Warehouse Workplace/ Office

Standard format of the cost of goods sold statement:

Entity Name Cost of Goods Sold statement for the year ended_______ Rupees Direct Material Consumed Opening inventory 10, Add Net Purchases 100, Material available for use 110, Less Closing inventory 20, Direct Material used 90, Add Direct labor 60, Prime cost 150, Add Factory overhead Cost 80, Total factory cost 230, Add Opening Work in process 30, Cost of good to be manufactured 260, Less Closing Work in process 50, Cost of good manufactured 210, Add Opening finish goods 100, Cost of good to be sold 310, Less closing finish goods 10, Cost of good to sold 300,

(Important tip for students) To prepare cost of goods sold statement, firstly one needs to collect six elements. Three of these belong to the cost and three belong to the inventory.

Six Elements of Cost of Goods Manufactured and Sold Statement

Cost Inventory Material & Supplies Material & Supplies Labor Work in Process FOH Finished goods

Following is the stepwise calculation of the information that is produced in the cost of goods sold statement:

Material Consumed Rupees Direct material opening inventory 10, Add Net purchases 100, Material available for use 110, Less raw material closing stock 20, 90, Note: Amount of net purchases comes up with the help of following calculation:

Purchases of direct material Less trade discounts and rebates Less purchases returns Add carriage inward

Usama manufacturing company submits the following information on June 30,2005.

**Required: 1)Cost of raw material consumed.

- Factory overhead cost**

SOLUTION:

Required: Prepare a statement showing total manufacturing cost.

Qasim & Co. Required

- Calculate cost of raw-material consumed

- Calculate prime cost

- Q.

- Raw material inventory, July 1, 2004 25,

- Purchases 125,

- Power, heat and light 3,

- Indirect material purchased and consumed 5,

- Administrative expenses 24,

- Depreciation of plant 18,

- Purchases returns 7,

- Fuel expenses 29,

- Depreciation of building

- Carriage inwards 3,

- Bad debts 2,

- Indirect labor

- Other manufacturing expenses 15,

- Raw materials inventory, June 30,2005 26,

- Raw materials inventory, July 1 2004 25, 1) Cost of raw material consumed:

- Add: purchases of materials 125,

- Less: purchase returns (7,000) 118,

- Add: carriage inwards 3,

- Cost of materials consumed 120, Less: materials inventory, June 30,2005 (26,000)

- Power, heat and light 3, 3) Factory overhead cost:

- Indirect material purchased and consumed 5,

- Depreciation of plant 18,

- Indirect labor 4,

- Fuel expenses 29,

- Other manufacturing expenses 15,

- Opening stock of raw material 52, Q. 3 Following data relates to Qasim & Co,

- Opening stock of work in process 46,

- Purchases of raw material 255,

- Direct labor cost 85,

- Factory overheads 76,

- Closing stock of raw material 61,

- Closing stock of work in process 36,

- Opening stock of raw material 52, Cost of goods manufactured statement

- Add: Purchases of raw material 255,

- Cost of raw material consumed 246, Less: Closing stock of raw material (61,000)

- Add: Direct labor cost 85,

- Prime cost/Direct cost 331,

- Add: Factory overheads 76,

- Manufacturing cost/Factory cost 407,

- Q.

- Sales for the year 450, FNS manufacturing company submits the following information on June 30,2005.

- Raw material inventory, July 1,2004 15,

- Finished goods inventory, July 1,2004 70,

- Purchases 120,

- Direct labor 65,

- Power, heat and light 2,

- Indirect material purchased and consumed 4,

- Administrative expenses 21,

- Depreciation of plant 14,

- Selling expenses 25,

- Depreciation of building 7,

- Bad debts 1,

- Indirect labor 3,

- Other manufacturing expenses 10,

- Work in process, July 1,2004 14,

- Work in process, June 30,2005 19,

- Raw materials inventory, June 30,2005 21,

- Finished goods inventory, June 30,2005 60,