menu

3.X

zoom

Loan operations

X Unit 4 Slide 1

Summary

4.1 Introduction to loan operations

4.2 Single-payment loans

4.3 Annuity-amortized loans

4.4 Changes in the conditions of the loan contract

4.5 The Annual Percentage Rate (APR) of a loan

Studia grazie alle numerose risorse presenti su Docsity

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

Prepara i tuoi esami

Studia grazie alle numerose risorse presenti su Docsity

Prepara i tuoi esami con i documenti condivisi da studenti come te su Docsity

Trova i documenti specifici per gli esami della tua università

Preparati con lezioni e prove svolte basate sui programmi universitari!

Rispondi a reali domande d’esame e scopri la tua preparazione

Riassumi i tuoi documenti, fagli domande, convertili in quiz e mappe concettuali

Studia con prove svolte, tesine e consigli utili

Togliti ogni dubbio leggendo le risposte alle domande fatte da altri studenti come te

Esplora i documenti più scaricati per gli argomenti di studio più popolari

Ottieni i punti per scaricare

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

An introduction to loan operations, focusing on single-payment loans and annuity-amortized loans. Single-payment loans require the repayment of the entire principal sum in a single payment at the end of the loan term, while annuity-amortized loans have scheduled periodic payments that consist of both principal repayment and interest payment. the differences between these two types of loans, their characteristics, and how to calculate the unpaid balance and interest payments.

Tipologia: Slide

1 / 25

Questa pagina non è visibile nell’anteprima

Non perderti parti importanti!

X Unit 4 (^) Loan operations Slide 1

4.1 Introduction to loan operations

4.2 Single-payment loans

4.3 Annuity-amortized loans

4.4 Changes in the conditions of the loan contract

4.5 The Annual Percentage Rate (APR) of a loan

X Unit 4 (^) Loan operations Slide 2

In a loan contract, a borrower receives initially an amount of money (called principal) from a lender, and is obligated to repay an equal amount of money to the lender at a later time (amortization of the loan), plus an additional sum of money, which is the interest of the loan.

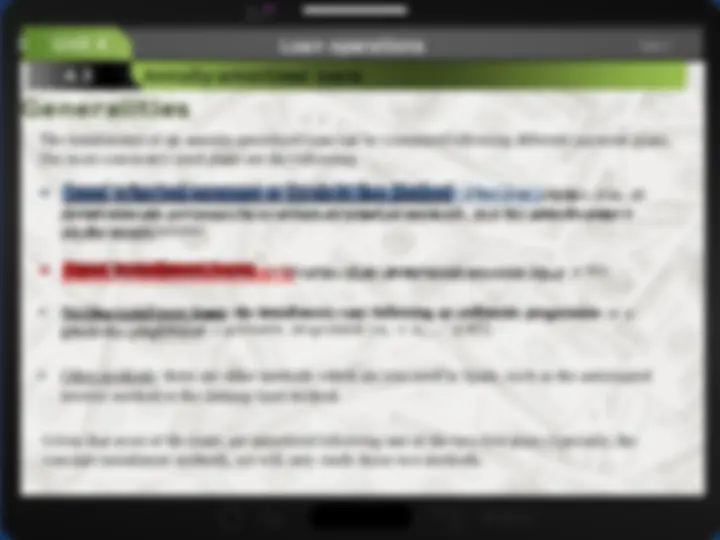

Depending on how the lender repays the principal, we can differentiate between two types of loans:

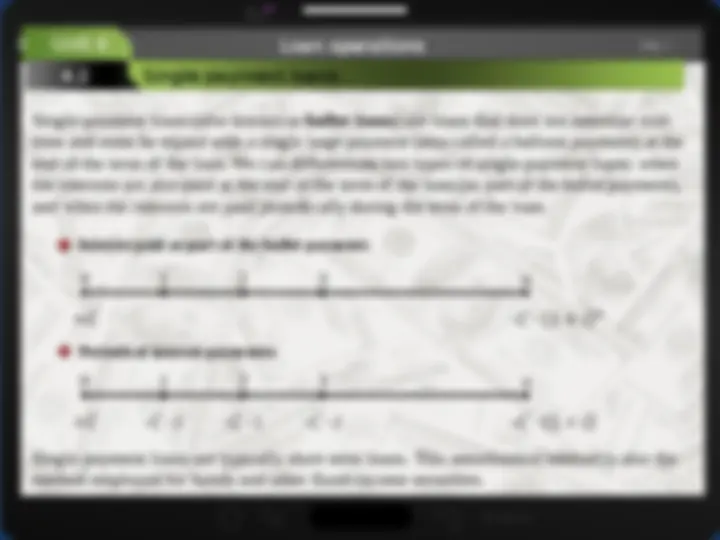

a) Single-payment loans: these loans require the payment of the entire principal sum and the end of its duration. The interests, however, can be paid periodically or not.

b) Loans repaid by annuities: the principal of the loan is repaid by an annuity. The interest is then also paid in an annuity, being computed over the unpaid balance.

4.1 Introduction to loan operations

X Unit 4 (^) Loan operations Slide 4

4.3 Annuity-amortized loans

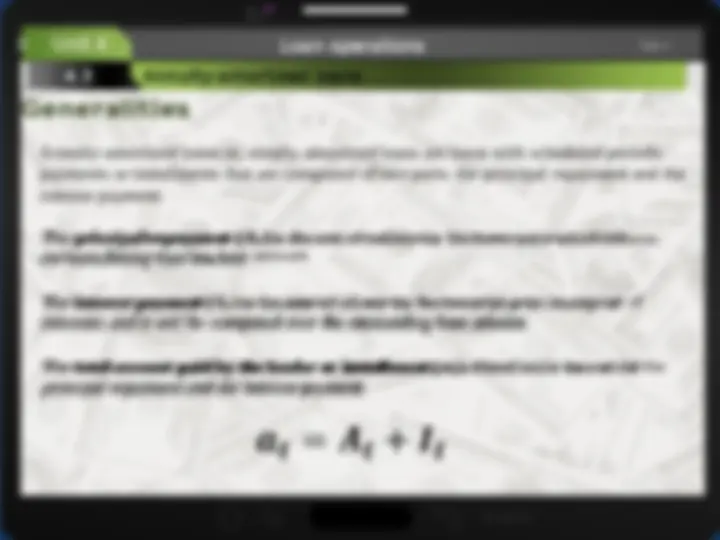

Annuity-amortized loans or, simply, amortized loans are loans with scheduled periodic payments or installments that are composed of two parts: the principal repayment and the interest payment.

The principal repayment ( is the amount of money the borrower pays which reduces the outstanding loan amount.

The interest payment ( is the amount of money the borrower pays in concept of interests, and it will be computed over the outstanding loan amount.

The total amount paid by the lender or installment ( , therefore, is the sum of the principal repaiment and the interest payment.

X Unit 4 (^) Loan operations Slide 5

4.3 Annuity-amortized loans

We will denote by the outstanding loan amount (the unpaid balance) at the moment t. Therefore, denotes the amount of money the lender receives from the borrower (that is, the principal of the loan). Given that the principal repayment ( is the amount paid by the borrower to reduce the outstanding amount, we can conclude that:

X Unit 4 (^) Loan operations Slide 7

4.3 Annuity-amortized loans

The unpaid balance of a loan at any moment k can be calculated as the sum of the discounted value of all the pending installments:

Rule of financial equivalence:^ Rule of financial equivalence:

X Unit 4 (^) Loan operations Slide 8

4.3 Annuity-amortized loans

Usually, loans are amortized by immediate annuities, i.e., the payment of the principal starts in the next period to the collection of the principal by the lender. However, it is possible to agree the payment of the principal by a deferred annuity. The period between the granting of the loan and the first payment of principal is called the grace period. There are two types of grace period: Interest-only grace period : during the grace period the lender only pays interests. 0 1 2 … c c+1 … n

No-payment grace period : during the grace period, the lender will make no payment, but the interests will be compounding. 0 1 2 … c c+1 … n

X Unit 4 (^) Loan operations Slide 10

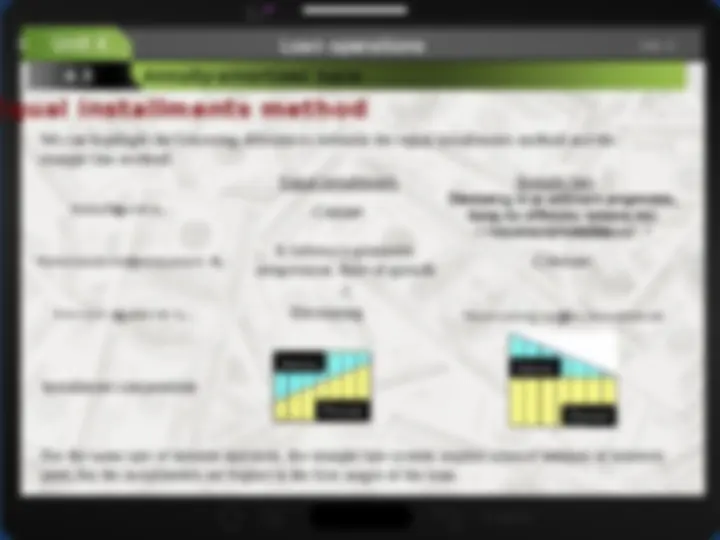

4.3 Annuity-amortized loans

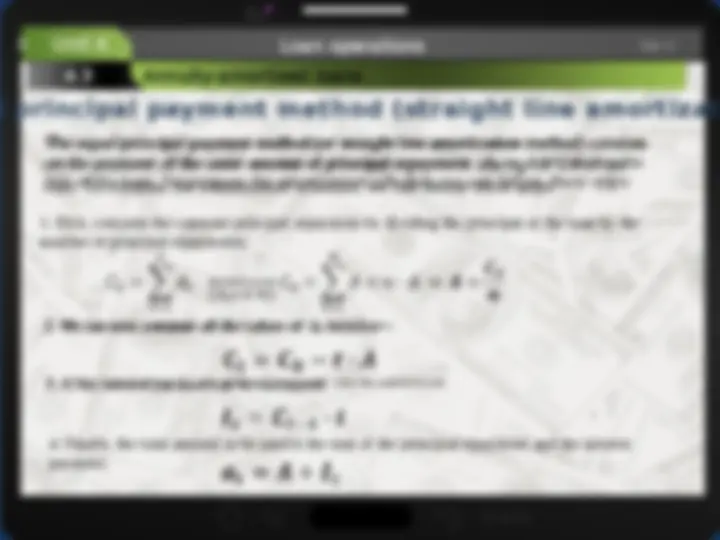

The equal principal payment method (or straight line amortization method) consists on the payment of the same amount of principal repayment during the life of the loan. To compute the amortization schedule, we can follow these steps:

X Unit 4 (^) Loan operations Slide 11

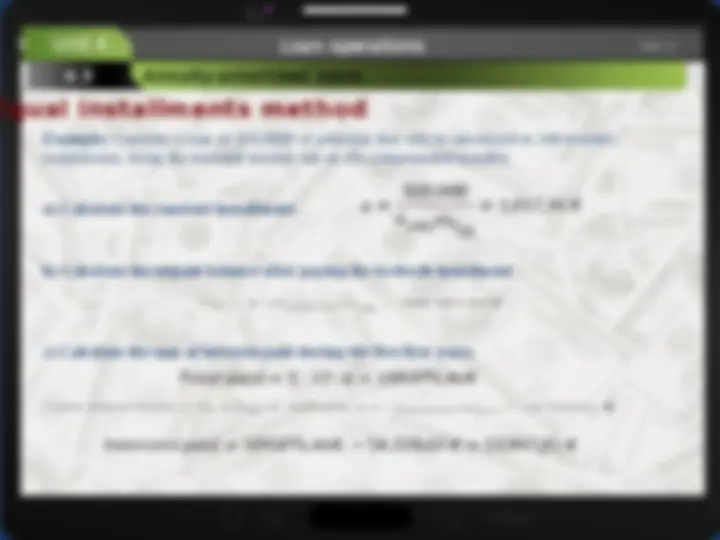

4.3 Annuity-amortized loans

Example: compute the amortization schedule of a loan of 600,000€ that will be amortized in three equal annual principal payments. The rate of interest is 1,5% per year.

Year C^ A I a

(^1) 600.000 200.000 600.000 x 1,5%=9.000 (^) 209.

(^2) 400.000 200.000 400.000 x 1,5%=6.000 206.

(^3) 200.0000 200.000 200.000 x 1,5%=3.000 203.

X Unit 4 (^) Loan operations Slide 13

4.3 Annuity-amortized loans

Once the unpaid balance is computed, we can also calculate the interest payment for any period t :

The principal repayment can be computed as the difference between the installment and the interest payment:

However, we can also study the behavior of those principal repayments in the equal installments method. Considering two consecutive principal repayments for the moments t and t+1 :

That is, the principal repayments vary in a geometric fashion with a growth rate of the rate of interest. Consequently, the principal repayments during the first stages of the loan are smaller than the principal repayments during the last stages of the loan. Consequently, as the installment is constant, the interest payments will be higher at the first stages and smaller at the last stages.

X Unit 4 (^) Loan operations Slide 14

4.3 Annuity-amortized loans

Example: Consider a loan of 300,000€ of principal that will be amortized in 240 monthly installments, being the nominal interest rate of 4% compounded monthly.

a) Calculate the constant installment:

b) Calculate the unpaid balance after paying the twelveth installment

c) Calculate the sum of interests paid during the five first years.

X Unit 4 (^) Loan operations Slide 16

4.3 Annuity-amortized loans

=PAGO(rate of interest; # installments; principal)

Function PAGO can be used to estimate the installment of a equal installments loan.

=PAGOPRIN(rate of interest; period; # installments; principal) Function PAGOPRIN can be used to estimate the principal repayments of a equal installments loan.

=PAGOINT(rate of interest; period; # installments; principal) Function PAGOINT can be used to estimate the interest payments of a equal installments loan.

X Unit 4 (^) Loan operations Slide 17

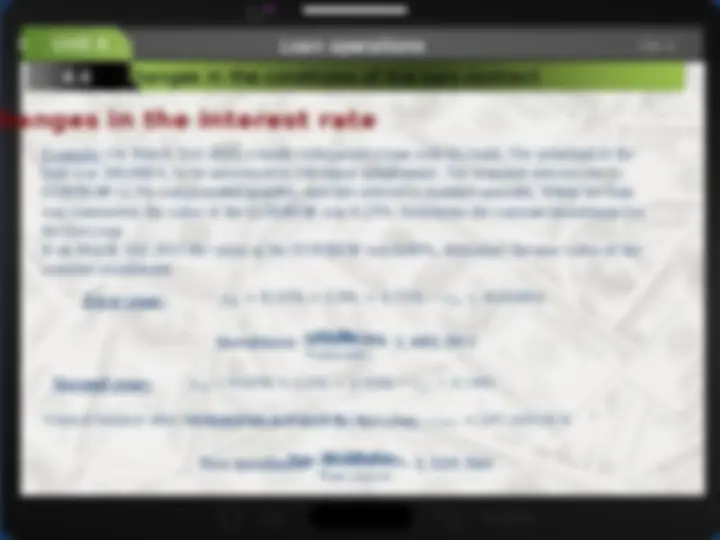

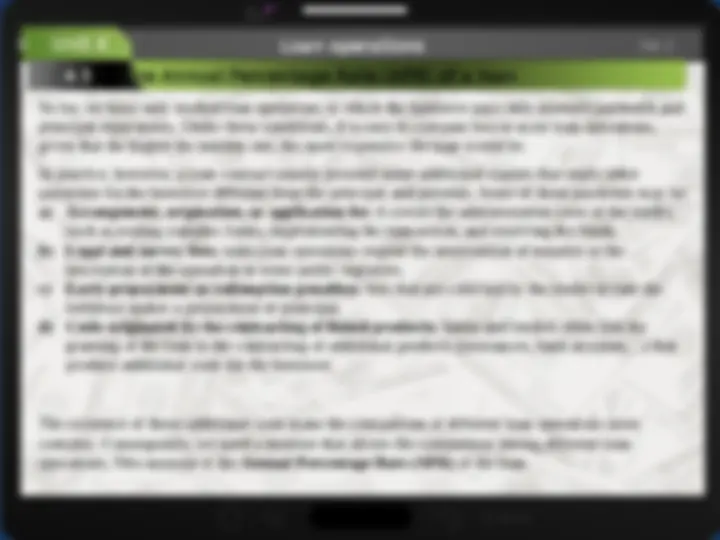

4.4 Changes in the conditions of the loan contract Next, we will study how to recompute the amortization schedule of a loan when some changes in the initial conditions happen. Specifically, we will study the changes in the rate of interest and the prepayment of principal.

Although the examples we have seen so far are fixed interest loans, the floating interest loans are quite frequent nowadays. In a floating interest loan , the interest rate of the loan is referred to an interest index (such as the EURIBOR or the LIBOR). Thus, the interest of the loan is usually equal to the value of that index plus a certain spread. With this agreement, the interest rate of the loan will be similar to the normal rates of interest in the financial markets in any moment. Usually, the floating interest loans include an interest revision plan. In that plan, the borrower and the lender agree the period for revision (a year, a half-year, a quarter…). Thus, at the beginning of every period, the interest rate for that period is calculated as the value of the reference index plus the spread. That interest rate will work as a fixed rate during that revision period, but it may change for the next revision period.

Albeit these changes can be applied to any type of loan, we will study their application to the equity installments loan, because it is the most common in practice.

X Unit 4 (^) Loan operations Slide 19

4.4 Changes in the conditions of the loan contract

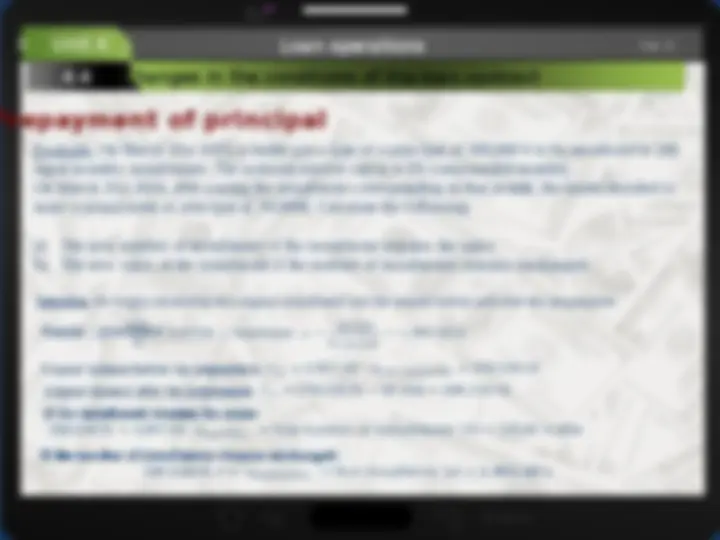

Loan contracts usually include a clause that allows the lender to make non-periodical payments to reduce the unpaid balance. These payments are known as “prepayment of principal”. However, the borrowers usually charges a commission when the lender makes such prepayments.

Given that the prepayments of principal modify the unpaid balance, it is necessary to recalculate the amortization schedule. There are two options for recalculating it:

For both cases, we will use the financial equivalence to calculate the new conditions of the loan.

X Unit 4 (^) Loan operations Slide 20

4.4 Changes in the conditions of the loan contract

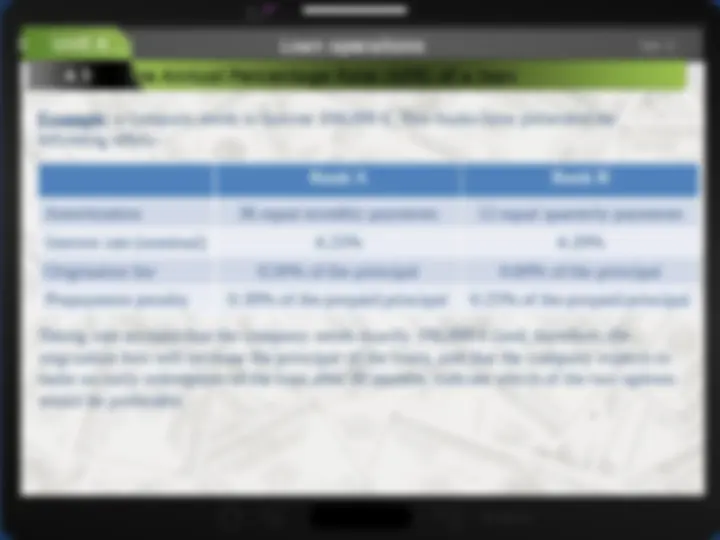

Example: On March 31st 2015, a lender got a loan of a principal of 300,000 € to be amortized in 240 equal monthly installments. The nominal interest rate is 4.5% compounded monthly. On March 31st 2016, after paying the installment corresponding to that month, the lender decided to make a prepayment of principal of 10,000€. Calculate the following:

a) The new number of installments if the installment remains the same. b) The new value of the installment if the number of installments remains unchanged.

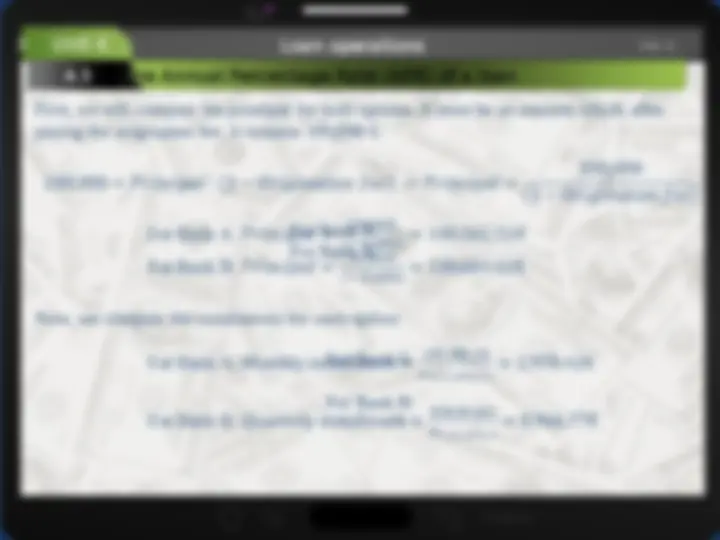

Solution : We begin calculating the original installment and the unpaid before and after the prepayment. Interest: Installment:

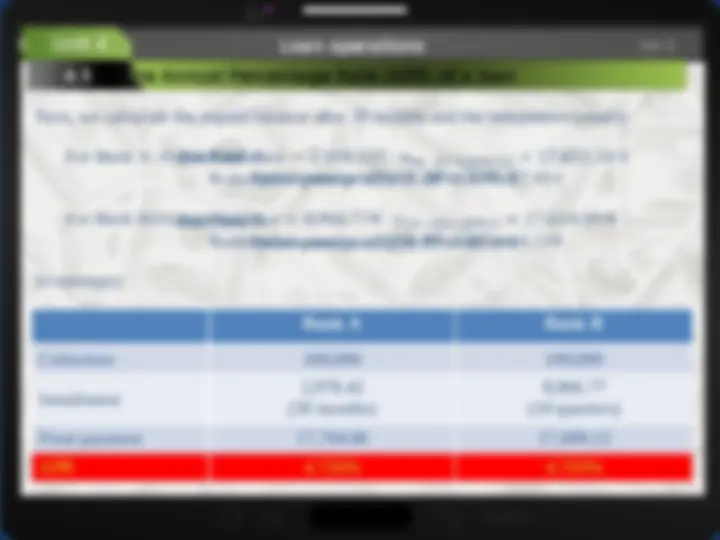

Unpaid balance before the prepayment: Unpaid balance after the prepayment: If the installment remains the same:

If the number of installments remains unchanged: