Download Auditing Problems_Bank and more Summaries Auditing in PDF only on Docsity!

I - AUDIT OF CASH AND CASH EQUIVALENTS

PROBLEM NO. 1 - Composition of Cash and Cash Equivalents The following data pertain to PRTC Corporation at December 31, 2015: Current account at Metrobank P 1,800, Current account at Allied Bank (100,000) Payroll account 500, Foreign bank account (in equivalent pesos) 800, Savings deposit in a closed bank 150, Postage stamps 1, Employee's postdated check 4, IOUs from employees 10, Credit memo from a vendor for a purchase return 20, Traveler's check 50, Money order 30, Petty cash fund (P4,000 in currency and expense receipts for P6,000)

Pension fund 2,000, DAIF check of customer 15, Customer's check dated 1/1/16 80, Time deposit - 30 days 200, Money market placement (due 6/30/16) 500, Treasury bills, due 3/31/16 (purchased 12/31/15) 200, Treasury bills, due 1/31/16 (purchased 2/1/15) 300, REQUIRED: Determine the cash and cash equivalents to be reported on the entity's December 31, 2015 statement of financial position. SOLUTION: Items included: Current account at Metrobank 1,800, Payroll account 500, Foreign bank account (in equivalent pesos) 800, Traveler’s check 50, Money order 30, Petty cash fund - currency 4, Time deposit – 30 days 200, Treasury bills, due 3/31/13 (purchased 12/31/12) 200, 3,584,

Items not included: Current account at Allied Bank (100,000) Short term borrowing Savings deposit in a closed bank 150,000 Other noncurrent assets Postage stamps 1,000 Unused supplies (Other CA) Employee’s post dated check 4,000 Trade and other receivables IOU from employees 10,000 Trade and other receivables Credit memo from a vendor for a purchase return 20, Deduction from accounts payable Petty cash fund - expense receipts 6,000 Expenses Pension fund 2,000,000 Noncurrent asset DAIF check of customer 15,000 Trade and other receivables Customer’s check dated 1/1/13 80,000 Trade and other receivables Money market placement (due 6/30/13) 500,000 Short term investment Treasury bills, due 1/31/13 (purchased 2/1/12) 300,000 Short term investment PROBLEM NO.2 - Computation of adjusted cash and cash equivalents You were able to gather the following from the December 31, 2015 trial balance of PRTC Corporation in connection with your audit of the company: Cash on hand P 372, Petty cash fund 10, BPI current account 950, Security Bank current account No.01 1,280, Security Bank current account No.02 (40,000) PNB savings account 500, PNB time deposit 300, Cash on hand includes the following items: a) Customer's check for P60,000 returned by bank on December 26, 2015 due to insufficient fund but subsequently redeposited and cleared by the bank on January 8, 2016. b) Customer's check for P30,000 dated January 2, 2016, received on December 29, 2015. c) Postal money orders received from customers, P36,000.

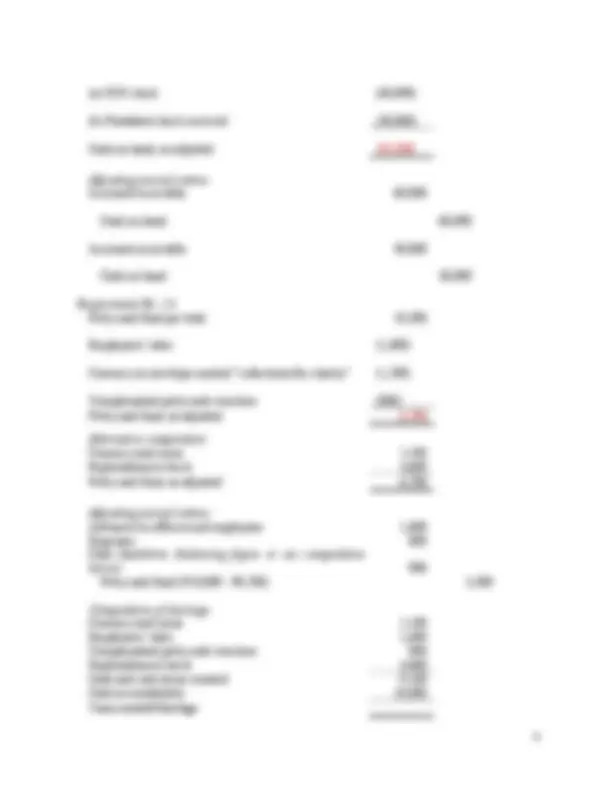

(a) NSF check (60,000) (b) Postdated check received (30,000) Cash on hand, as adjusted 282, Adjusting journal entries Accounts receivable 60, Cash on hand 60, Accounts receivable 30, Cash on hand 30, Requirement No. 1.b Petty cash fund per total 10, Employees' vales (1,600) Currency in envelope marked "collections for charity" (1,200) Unreplenished petty cash vouchers (800) Petty cash fund, as adjusted 6, Alternative computation: Currency and coins 2, Replenishment check 4, Petty cash fund, as adjusted 6, Adjusting journal entries: Advances to officers and employees 1, Expenses 800 Cash short/over (balancing figure or see computation below) 900 Petty cash fund (P10,000 - P6,700) 3, Computation of shortage: Currency and coins 2, Employees' vales 1, Unreplenished petty cash vouchers 800 Replenishment check 4, Cash and cash items counted 9, Cash accountability 10, Unaccounted/Shortage

Requirement No. 1.c BPI current account, per trial balance 950, Unreleased check 50, Post dated check delivered 86, BPI current account, as adjusted 1,086, Adjusting journal entries: BPI current account 50, Accounts payable 50, Accounts receivable 86, Cash on hand 86, Requirement No. 1.d Cash on hand (see no. 1.a) 282, Petty cash fund (see no. 1.b) 6, BPI current account (see no. 1.c) 1,086, Security Bank current account no. 1 1,280, Security Bank current account no. 2 (40,000) 1,240, PNB time deposit (cash equivalent) 300, Cash and cash equivalents, as adjusted 2,914, Note: The P500,000 PNB savings account should be presented separately from cash and cash equivalents since it has been earmarked for the acquisition of a noncurrent asset.

Accounted for as follows: Cash returned by Roy to the sales manager P 240 Personal check of sales manager 3, Total P 3, Additional information: a) The custodian is not authorized to cash checks. b) The last official receipt included in the deposit on December 30 is No. 351 and the last official receipt issued for the current year is No. 355. The following official receipts are all dated December 31, 2015. O.R. No. Amount Form of payment 352 P 27, Cash 353 35,600 Check 354 7,200 Cash 355 16,600 Check c) The Petty Cash balance per general ledger is P20,000. The last replenishment of the fund was made on December 22, 2015. REQUIRED:

- Determine shortage or overage, if any

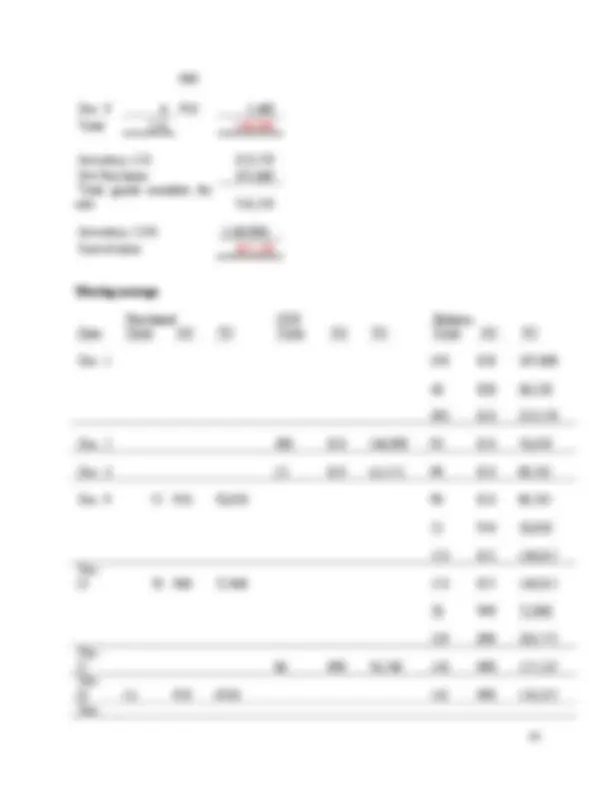

- Adjusting entries as of December 31, 2015 SOLUTION: Requirement No. 1 Bills and coins Denomination Quantity Amount Total P100.00 10 1, 50.00 80 4, 20.00 70 1, 10.00 54 540 1.00 410 410 0.50 324 162 0.25 64 16 7,

Checks Date Drawer Amount Dec. 30 Ms. Jessie 2, Dec. 30 Robert 28, Dec. 31 Jay Ar 3, Dec. 31 Francis 35, Dec. 31 Ryan 16,600 85, Unreplenished vouchers Date Account Amount Dec. 23 Advances 14, Dec. 27 Postage 3, Dec. 29 Transportation 300 Dec. 29 Repairs 1, 19, AJE 1& Total cash and cash items counted 112, Less accountabilities: Petty cash 20, Undeposited collections - per OR 86, Undeposited collections - without OR 28,000 AJE 4 Excess travel advance returned 3,360 AJE 3 Unclaimed salaries 15,000 152,960 AJE 5 Cash shortage (40,332) AJE 6 Requirement No. 2 1 Advances to officers and employees 14, Postage expense 3, Transportation expense 300 Repairs and maintenance 1, Petty cash fund 19, 2 Unused postage 730 Postage expense 730

c. A customer's check for P15,400 was entered as P14,500 by both the depositor and the bank but was later corrected by the bank. d. Check no. 142 for P12,425 was enter in the cash disbursement journal at P12, 245 and check no. 156 for P3,290 was entered as P32,900. e. Bank service charges of P1,830 for December were not yet recorded on the books. f. A bank memo stated that a customer's note for P25,000 and interest of P1,000 had been collected on December 28, and the bank charged P500 (No entry was made on the books when the note was sent to the bank for reconciliation). g. Receipts for December 31 for P24,000 were deposited on January 2. No. 123 P 3,000 No. 154 P 4, 143 2,000 157 6, 144 7,000 159 7, 147 3,000 169 5, *Certified by the bank in December i. A deposit of P20,000 was recorded by the bank on December 5, but it should have been recorded for Dolor Company rather than Dollar Company. j. Petty cash of P10,000 was included in the Cash in Bank balance. k. Proceeds from cash sales of P60,000 for December 18 were stolen. The company expects to recover this amount from insurance company. The cash receipts were recorded in the books, but no entry was made for the loss. l. The December 21 deposit included a check for P20,000 that had been returned on December 15 marked NSF. Dollar Company had made no entry upon return of the check. the redeposit of the check on December 21 was recorded in the cash receipts journal of Dollar Company as collection on account. REQUIRED:

- Bank reconciliation using: a. Bank to book method; b. Book to bank method; and c. Adjusted balance method

- Adjusting entries as of December 31, 2015.

SOLUTION:

DOLLAR COMPANY

Bank Reconciliation - Bank to Book Method December 31, 2012 Balance per bank 106, Add (deduct): a) Customer's uncollectible check (NSF) 30, b) Dishonored note receivable (including P2,000 protest fee) 62, c) Book error in recording collection (P15,400 - P14,500) (900) d) Book errors in recording disbursements Check no. 142 (P12,425 - P12,245) - under 180 Check no. 156 (P3,290 - P32,900) - over (29,610) e) December bank service charges 1, f) Note collected by bank (including interest income of P1,000 and net of service charge of P500) (25,500) g) Deposits in transit 24, h) Outstanding checks (35,000) I) Bank error in recording deposit (20,000) j) Petty cash fund 10, k) Stolen cash sales to be recovered from insurance co. 60, l) Double counted deposit - NSF 20, Balance per books 203, DOLLAR COMPANY Bank Reconciliation - Book to Bank Method December 31, 2012 Balance per books 203, Add (deduct): a) Customer's uncollectible check (NSF) (30,000) b) Dishonored note receivable (including P2,000 protest fee) (62,000) c) Book error in recording collection (P15,400 - P14,500) 900 d) Book errors in recording disbursements Check no. 142 (P12,425 - P12,245) - under (180) Check no. 156 (P3,290 - P32,900) - over 29, e) December bank service charges (1,830) f) Note collected by bank (including interest income of P1,000 and net of service charge of P500) 25, g) Deposits in transit (24,000)

Cash in bank 180

- Cash in bank 29, Accounts payable 29,

- Bank service charge 1, Cash in bank 1,

- Cash in bank 25, Bank service charge 500 Notes receivable 25, Interest income 1,

- Petty cash fund 10, Cash in bank 10,

- Claims from insurance co. 60, Cash in bank 60,

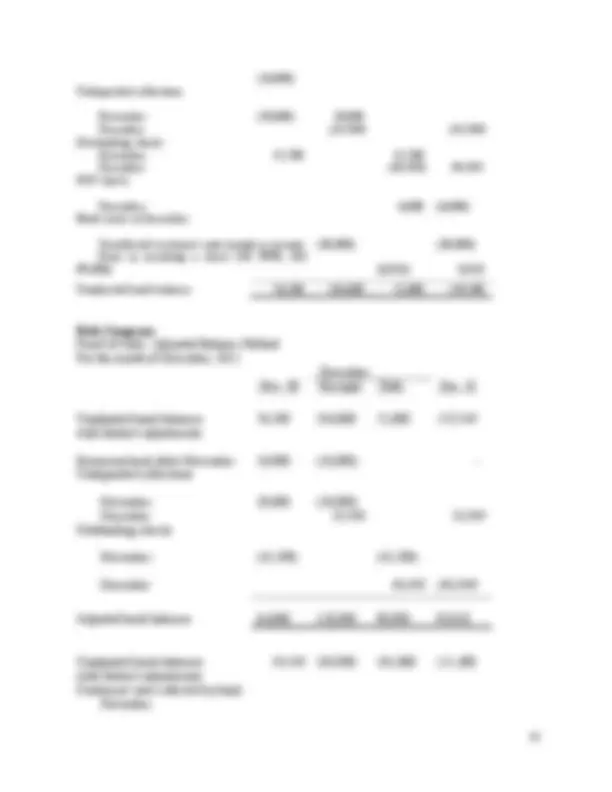

- Accounts receivable 20, Cash in bank 20, PROBLEM NO. 5 - Bank reconciliation and shortage computation You are conducting an audit of the Swerte Company for the year ended December 31, 2015. The internal control procedures surrounding cash transactions were not adequate. The bookkeeper-cashier handles cash receipts, maintains accounting records, and prepares the monthly bank reconciliations. The bookkeeper-cashier prepared the following reconciliation at the end of the year: Balance per bank statement P 350, Add: Deposit in transit P 175, Note collected by bank 15,000 190, Total 540, Less: Outstanding checks 246, Balance per general ledger 293, In the process of your audit, you gathered the following:

- At December 31, 2015, the bank statements and general ledger showed balances of P350,000 and P293,500, respectively.

- The cut-off bank statement showed a bank charge on January 2,2016 for P30, representing correction of an erroneous bank credit.

- Included in the list of outstanding checks were the following:

a. A check payable to a supplier, dated December 29, 2015, in the amount of P14,750, released on January 5,2016. b. A check representing advance payment to a supplier in the amount of P37,210, the date of which is January 4, 2016, and released in December, 2015.

- On December 31, 2015, the company received and recorded customer's postdated check amounting to P50,000. REQUIRED

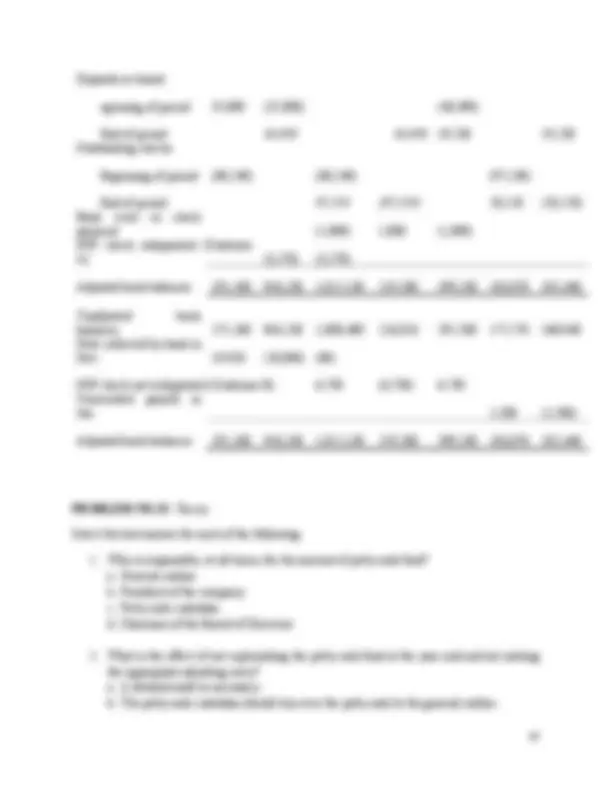

- Compute for the following as at December 31, 2015: a. Adjusted deposit in transit b. Adjusted outstanding checks c. Adjusted cash in bank d. Cash shortage

- Adjusting entries as of December 31, 2015 SOLUTION: Requirement No. 1.a Unadjusted deposit in transit 175, Post dated check received (50,000) Adjusted deposit in transit 125, Requirement No. 1.b Unadjusted outstanding checks 246, Unreleased check (14,750) Post dated check issued (37,210) Adjusted outstanding checks 194, Requirement No. 1.c&d Bank Books Unadjusted balances 350,000 293, Add (deduct) adjustments: Post dated check received (50,000) AJE 1 Deposit in transit (see 1.a)

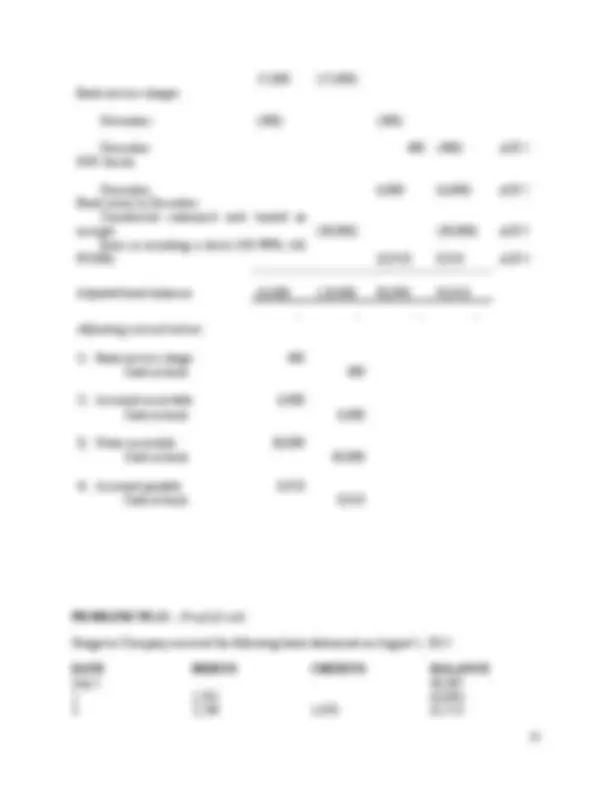

PROBLEM NO. 6 - Cash shortage computation You were engaged to audit the books of Davao Company. From the records of the company, you gathered the following information: Davao Company started operations on October 2, 2015 with the owners investing P150,000 cash. Monthly bank reconciliation statements have not been prepared; however, bank statements for October, November, and December were made available to you. Your analysis of these bank statements showed total bank credits (deposits) of P575,000 including the owners' initial investment and a bank loan, details of which are in additional data. The bank statement in December, 2015 showed an ending balance of P91, 500. Examination of the paid checks disclosed that checks totaling P4,500 were issued by the company in December, 2015, and were presented for payment only in January, 2016. Cash count of the cashier's accountability amounted to P5,000. You were told by the cashier that these were collections from credit sales on December 30, 2015, deposited on January 2, 2016. Additional information are as follows: a. Accounts receivable subsidiary ledgers had a total balance of P70,000 at December 31,

- P5,000 of this was ascertained to be uncollectible. b. Suppliers' unpaid invoices for merchandise totaled P15,000;while an account for store fixtures bought for P50,000 had an unpaid balance of P5,000. c. Merchandise inventory at December 31, 2015 amounted to P30,000 but P5,000 of these were spoiled with no resale value. d. The bank statement in October showed a bank credit for P98,000, dated October 2, 2015. Inquiry from the cashier disclosed that the amount represents proceeds of a 90-day, discounted bank note.P80,000 o this loan was paid by check in December, 2015. e. Operating expenses paid during the period totaled P180,000; while merchandise purchase amounted to P250,000. f. The gross profit rate is 120% of cost. REQUIRED: Determine the cash shortage as of December 31, 2015. SOLUTION:

Unadjusted balance per bank, 12/31 91, Outstanding checks , 12/31 (4,500) Undeposited collections, 12/31 5, Adjusted balance per bank, 12/31 (Cash accounted) 92, Cash balance per books, 12/31/Cash accountability (see computation below) 122, Cash over (short) (30,000) Computation of cash balance per books, 12/ Cash receipts: Owners' investment 150, Proceeds from loan 98, Collections from customers (see computation below) 414, Total 662, Cash disbursements: Purchases (P250,000 - P15,000) 235, Store fixtures (P50,000 - P5,000) 45, Loan payment 80, Expenses paid 180,000 540, Cash balance per books, 12/31 122, Computation of collections from sales Purchases/TGAS 250, Less merchandise inventory, 12/31 30, Cost of sales 220, Add gross profit (P220,000 x 120%) 264, Sales 484, Less accounts receivable, 12/31 70, Collections from sales 414, PROBLEM NO. 7 - Proof of cash

SOLUTION:

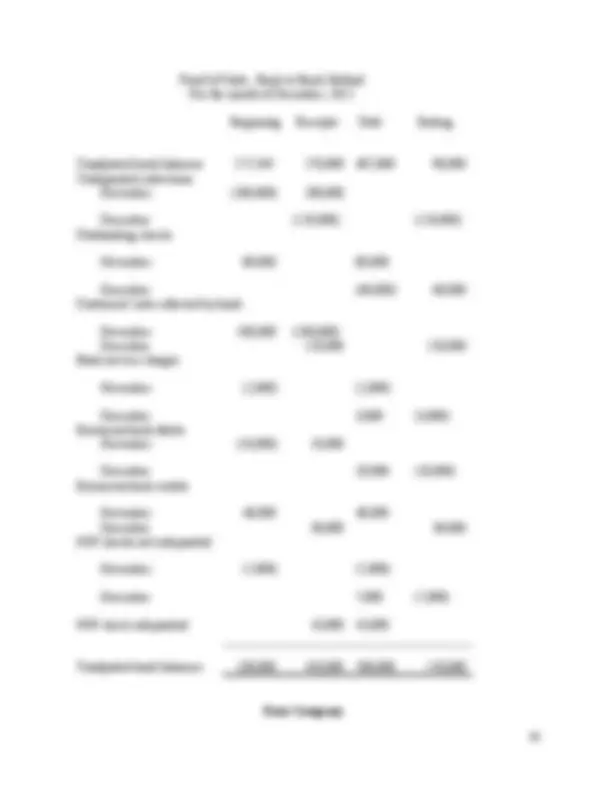

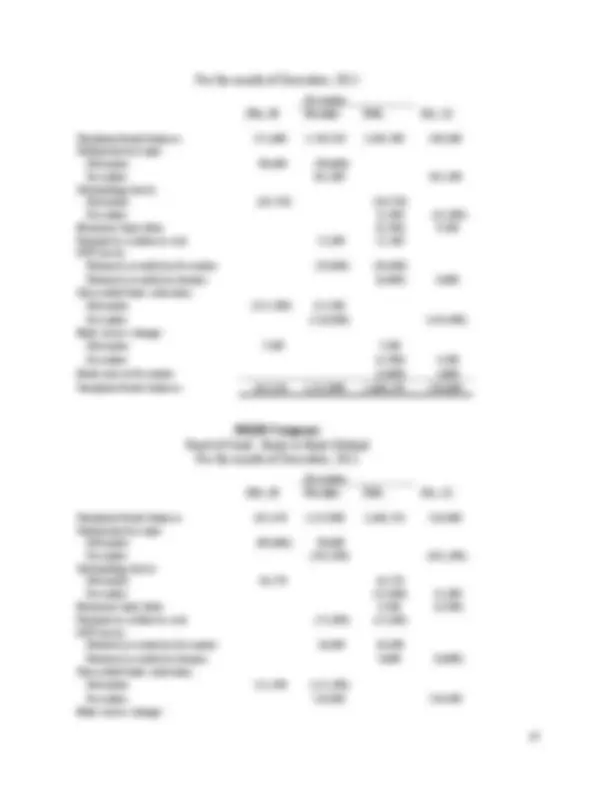

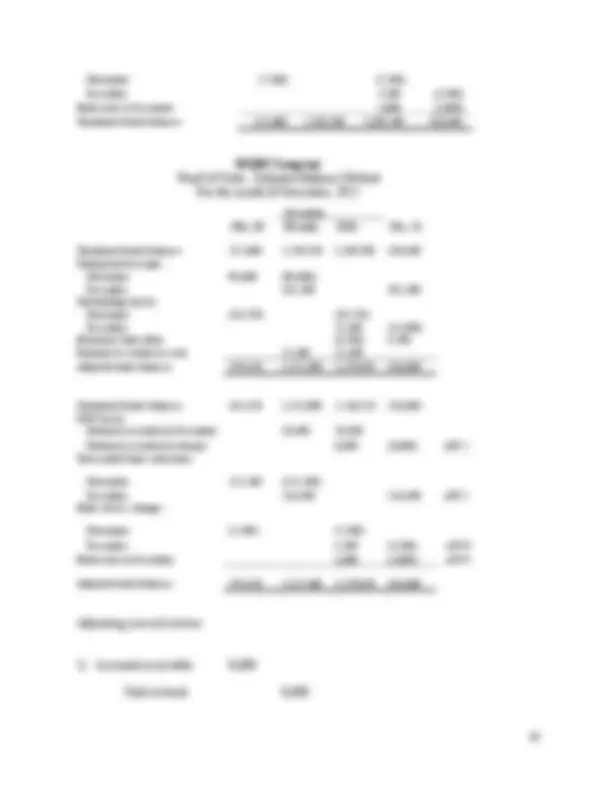

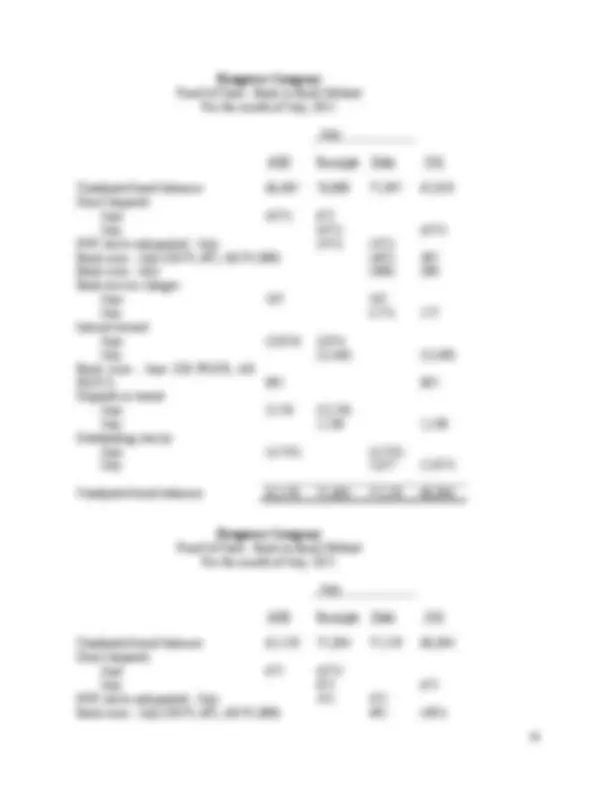

Euro Company Proof of Cash - Bank to Book Method For the month of December, 2012 Beginning Receipts Disb Ending Unadjusted bank balances 230,000 420,000 500,000 150, Undeposited collections November 200,000 (200,000) December 120,000 120, Outstanding checks November (80,000) (80,000) December 60,000 (60,000) Customers' note collected by bank November (100,000) 100, December (120,000) (120,000) Bank service charges November 2,000 2, December 3,000) 3, Erroneous bank debits November 10,000 (10,000) December 20,000) 20, Erroneous bank credits November (40,000) 40,000) December (30,000) (30,000) NSF checks not redeposited November 5,000 5, December (7,000) 7, NSF check redeposited (10,000) (10,000) Unadjusted book balances 227,000 270,000 407,000 90, Euro Company

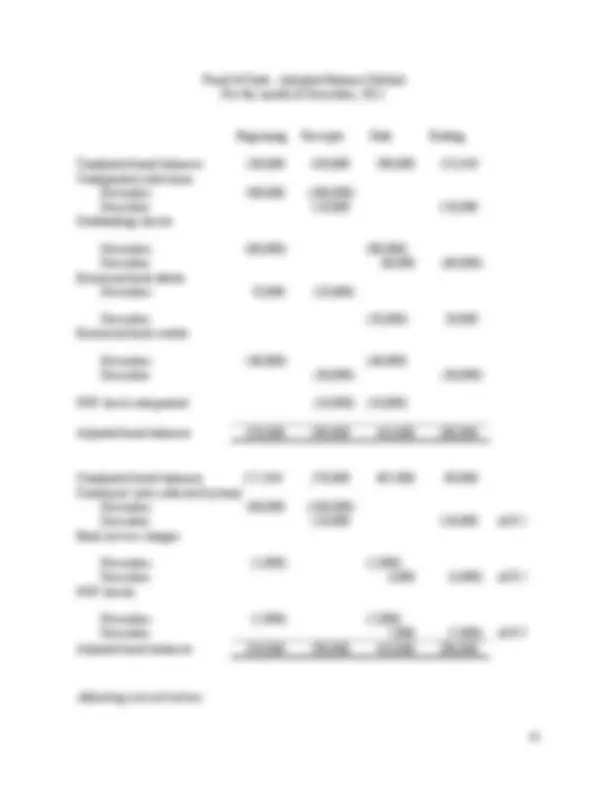

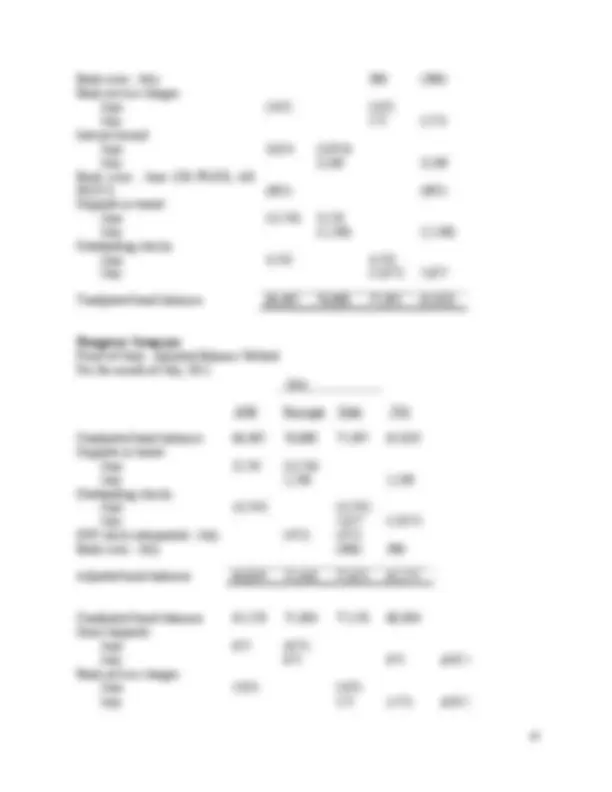

Proof of Cash - Book to Bank Method For the month of December, 2012 Beginning Receipts Disb Ending Unadjusted book balances 227,000 270,000 407,000 90, Undeposited collections November (200,000) 200, December (120,000) (120,000) Outstanding checks November 80,000 80, December (60,000) 60, Customers' note collected by bank November 100,000 (100,000) December 120,000 120, Bank service charges November (2,000) (2,000) December 3,000 (3,000) Erroneous bank debits November (10,000) 10, December 20,000 (20,000) Erroneous bank credits November 40,000 40, December 30,000 30, NSF checks not redeposited November (5,000) (5,000) December 7,000 (7,000) NSF check redeposited 10,000 10, Unadjusted bank balances 230,000 420,000 500,000 150, Euro Company