Forecasting a Single Variable from

its own History, continued

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The concepts of time series analysis, focusing on forecasting a single variable from its own history. Topics include the need for data, the wold representation, auto-regressive (ar) and moving average (ma) representations, unit root problems, and arma processes. The document also covers forecasting from ar models and the effect of shocks on future observations.

Typology: Slides

1 / 18

This page cannot be seen from the preview

Don't miss anything!

Forecasting a Single Variable from

its own History, continued

History is available, and has implications for the present / future

Errors have finite, time-independent variance

No data is perfect. The question is how imperfect the data can be, and still be useable

How do you choose between AR and MA representations?

What if the shocks are permanent, but caused by temporary shocks in the growth rate? These are referred to as Unit Root problems.

Do you model a permanent shock to GDP (for example), or the temporary shock to the growth rate of GDP that caused it?

E.g.: the effect of being in the Army on your lifetime earnings...

If the autocorrelations of first differences (changes over time) are not significantly different from zero, then we cannot predict future changes of a variable from past changes

Possible to have time series processes that are mixtures of AutoRegressive and Moving Average factors.

Example: ARMA(1,1) Process:

X (^) t a 0 a X 1 t 1 e (^) t b e 1 t 1

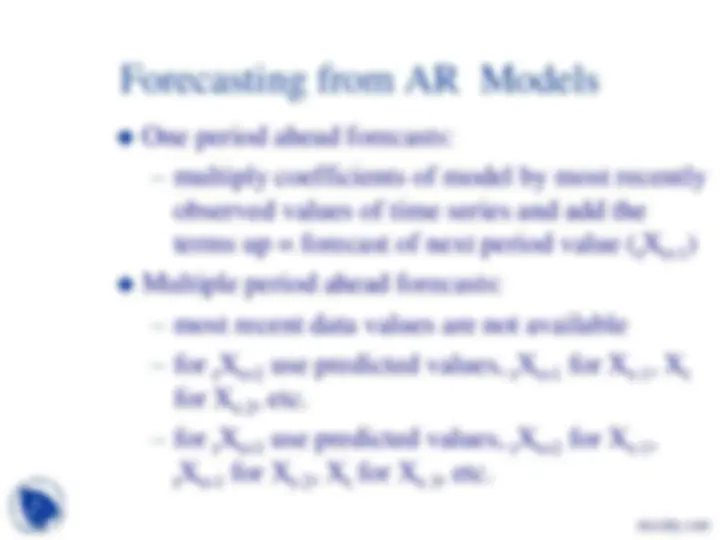

One period ahead forecasts:

Multiple period ahead forecasts:

Procedure of using forecasted values for actual past values in making multiple period forecasts is known as the chain rule of forecasting.

Effect of shock at time = t persists to affect observations at t+3, t+4, etc. (a 13 , a 14 , etc.)

Size of the effect on future observations becomes smaller as long as absolute value of autoregressive coefficient is < 1.

Shocks in AR model carry forward to affect future observations indefinitely

Maximize Adjusted R^2 (or minimize standard error of estimate[s.e.e.])?

Akaike and Schwartz Information Criteria?

Assume et = 1.

Xt = et + c 1 et-1 = 1.0 +c 1 et-

Xt+1 = et+1+ c 1

Xt+2 = et+2 + c 1 et+1 (shock has died out)

Xt+3 = et+3 + c 1 et+

Random Walk models