Download Leverage - E-Commerce - Lecture Slides and more Slides Fundamentals of E-Commerce in PDF only on Docsity!

237

ROE and Leverage

237

¨ A high ROE, other things remaining equal, should yield a

higher expected growth rate in equity earnings.

¨ The ROE for a firm is a funcEon of both the quality of its

investments and how much debt it uses in funding these

investments. In parEcular

ROE = ROC + D/E (ROC -‐ i (1-‐t))

where,

ROC = (EBIT (1 -‐ tax rate)) / (Book Value of Capital)

BV of Capital = BV of Debt + BV of Equity -‐ Cash

D/E = Debt/ Equity raEo

i = Interest rate on debt

t = Tax rate on ordinary income.

238

Decomposing ROE

238

¨ Assume that you are analyzing a company with a 15% return

on capital, an aRer-‐tax cost of debt of 5% and a book debt to

equity raEo of 100%. EsEmate the ROE for this company.

¨ Now assume that another company in the same sector has

the same ROE as the company that you have just analyzed

but no debt. Will these two firms have the same growth rates

in earnings per share if they have the same dividend payout

raEo?

¨ Will they have the same equity value?

240

EsEmaEng Growth in Disney

ROC and Expected Growth

240

¨ We compute the return on capital, using operaEng

income in 2008 and capital invested at the start of

2008 (end of 2007):

Return on Capital 2008 =

¨ If Disney maintains its 2008 normalized

reinvestment rate of 53.72% and return on capital of

9.91% for the next few years, its growth rate will be

5.32 percent.

Expected Growth Rate = 53.72% * 9.91% = 5.32%

€

EBIT (1 - t) (BV of Equity + BV of Debt - Cash)

= 7,030 (1 -.38) (30,753 + 16,892 - 3,670)

= 9.91%

241

IV. Gepng Closure in ValuaEon

241

¨ Since we cannot esEmate cash flows forever, we esEmate cash flows for a

“growth period” and then esEmate a terminal value, to capture the value

at the end of the period:

¨ When a firm’s cash flows grow at a “constant” rate forever, the present

value of those cash flows can be wriqen as:

Value = Expected Cash Flow Next Period / (r -‐ g) where, r = Discount rate (Cost of Equity or Cost of Capital) g = Expected growth rate forever.

¨ This “constant” growth rate is called a stable growth rate and cannot be

higher than the growth rate of the economy in which the firm operates.

Value =

CF

t (1+r)t^

Terminal Value

t=1 (1+r)^ N

t=N ∑

243

Choosing a Growth Period: Examples

243

244

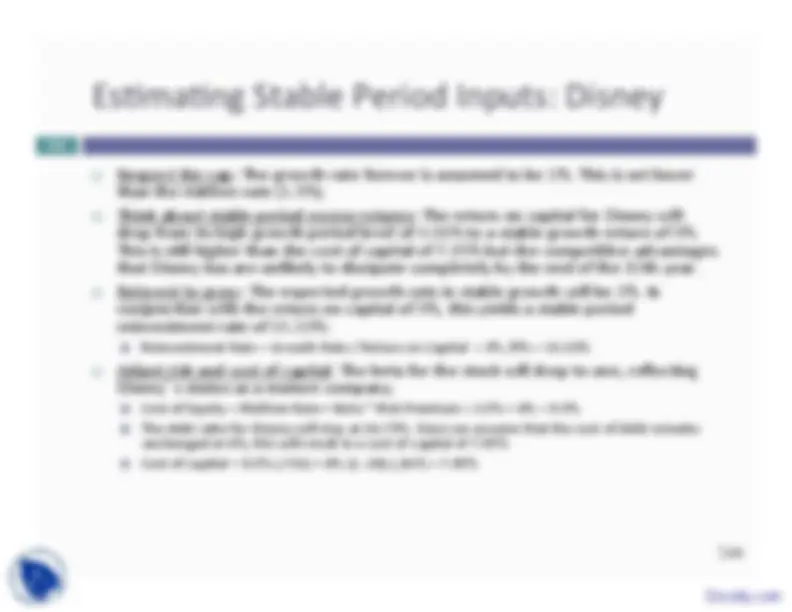

EsEmaEng Stable Period Inputs: Disney

244

¨ Respect the cap: The growth rate forever is assumed to be 3%. This is set lower than the riskfree rate (3.5%). ¨ Think about stable period excess returns: The return on capital for Disney will drop from its high growth period level of 9.91% to a stable growth return of 9%. This is sEll higher than the cost of capital of 7.95% but the compeEEve advantages that Disney has are unlikely to dissipate completely by the end of the 10th year. ¨ Reinvest to grow: The expected growth rate in stable growth will be 3%. In conjuncEon with the return on capital of 9%, this yields a stable period reinvestment rate of 33.33%: ¤ Reinvestment Rate = Growth Rate / Return on Capital = 3% /9% = 33.33% ¨ Adjust risk and cost of capital: The beta for the stock will drop to one, reflecEng Disney’s status as a mature company. ¤ Cost of Equity = Riskfree Rate + Beta * Risk Premium = 3.5% + 6% = 9.5% ¤ The debt raEo for Disney will stay at 26.73%. Since we assume that the cost of debt remains unchanged at 6%, this will result in a cost of capital of 7.95% ¤ Cost of capital = 9.5% (.733) + 6% (1-‐.38) (.267) = 7.95%

246

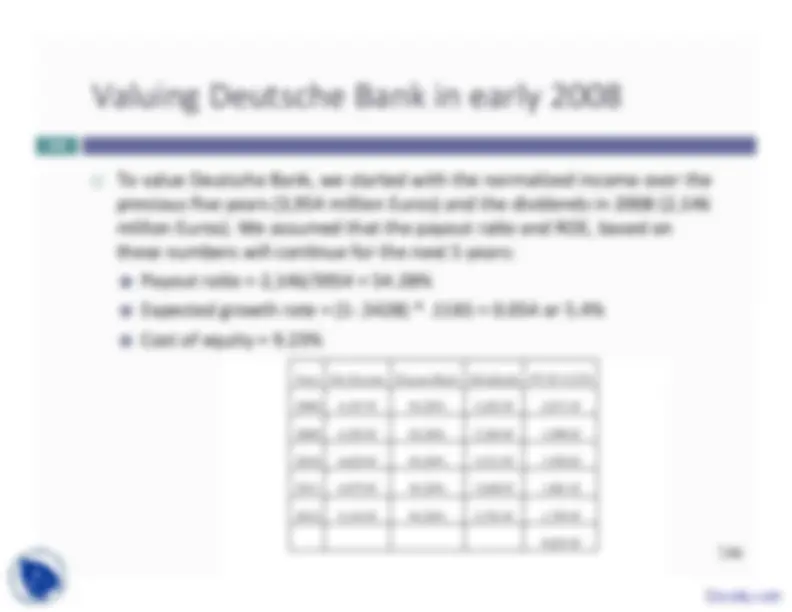

Valuing Deutsche Bank in early 2008

246

¨ To value Deutsche Bank, we started with the normalized income over the

previous five years (3,954 million Euros) and the dividends in 2008 (2,

million Euros). We assumed that the payout raEo and ROE, based on

these numbers will conEnue for the next 5 years:

¤ Payout raEo = 2,146/3954 = 54.28%

¤ Expected growth rate = (1-‐.5428) * .1181 = 0.054 or 5.4%

¤ Cost of equity = 9.23%