Report on

Employer Firms

FEDERAL

RESERVE

BANKS of

MARCH 2016

2015

SMALL

BUSINESS

CREDIT

SURVEY

NEW YORK

ATLANTA

BOSTON

CLEVELAND

PHILADELPHIA

RICHMOND

ST. LOUIS

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An analysis of the Small Business Credit Survey Report on Employer Firms, focusing on outstanding debt, startup funding, and financing demand by state. The report includes data on the percentage of firms with outstanding debt, the amount of debt, collateral used to secure debt, and funding used during the first two years of operations. Additionally, the report examines the application rate, sources of financing advice, and factors influencing application decisions.

Typology: Slides

1 / 78

This page cannot be seen from the preview

Don't miss anything!

MARCH 2016

2015

SMALL

BUSINESS

CREDIT

SURVEY

i ACKNOWLEDGEMENTS iii EXECUTIVE SUMMARY

1 DEMOGRAPHICS

3 PERFORMANCE 4 EMPLOYMENT 5 BUSINESS CHALLENGES

6 FINANCING AND DEBT

7 DEMAND FOR FINANCING

8 NON-APPLICANTS 9 FINANCING SEARCH 10 CREDIT APPLICATIONS 11 CREDIT SOURCES 12 CREDIT OUTCOMES

13 FINANCING APPROVAL 14 LENDER SATISFACTION

15 FINANCING SHORTFALLS

17 METHODOLOGY

2015 SMALL BUSINESS CREDIT SURVEY | REPORT ON EMPLOYER F IRMS ii

This report is the result of the collaborative effort, input, and analysis of the following individuals. REPORT TEAM Brett Barkley, Federal Reserve Bank of Cleveland Claire Kramer Mills, Federal Reserve Bank of New York Maria Carmelita Recto, Federal Reserve Bank of New York Ellyn Terry, Federal Reserve Bank of Atlanta Emily Wavering, Federal Reserve Bank of Richmond

Kyan Bishop, Federal Reserve Bank of Atlanta Bonnie Blankenship, Federal Reserve Bank of Cleveland Jeanne Milliken Bonds, Federal Reserve Bank of Richmond Nathaniel Borek, Federal Reserve Bank of Philadelphia Brian Clarke, Federal Reserve Bank of Boston Chelsea Cruz, Federal Reserve Bank of New York Eileen Divringi, Federal Reserve Bank of Philadelphia Shannon McKay, Federal Reserve Bank of Richmond Drew Pack, Federal Reserve Bank of St. Louis E. Kathleen Ranalli, Federal Reserve Bank of Cleveland Javier Silva, Federal Reserve Bank of New York Ann Marie Wiersch, Federal Reserve Bank of Cleveland We thank all of the above for another successful collaboration. Our intention is to field the next survey in Q3 2016 when we expect even broader coverage. The views expressed here are those of the authors and do not necessarily represent the views of the Federal Reserve System.

Claire Kramer Mills, PhD Assistant Vice President and Community Affairs Officer Federal Reserve Bank of New York

2015 SMALL BUSINESS CREDIT SURVEY | REPORT ON EMPLOYER F IRMS iii

Despite the significance of small businesses to the U.S. economy and to local communi- ties, information on small business financing conditions is limited, leaving important knowledge gaps for policymakers and serviceproviders. Although several sources report aggregate lending volumes and lender per-ceptions, (^1) timely data about business owners’ financing decisions are rare. Furthermore, as previous studies have shown, credit demand, sources, and outcomes vary considerablywithin the small business sector. Since 2010, the Federal Reserve has helped to address this gap through regional surveys of business owners. Beginning in 2014, the Federal Reserve Banks of New York, Atlanta, Cleveland, and Philadelphia collaborated ona joint Small Business Credit Survey (SBCS) to cover much of the eastern region of theU.S. The collaboration has now expanded to include seven Reserve Banks: Atlanta,Boston, Cleveland, New York, Philadelphia, Richmond, and St. Louis. In 2015, the SBCS yielded 5,420 responses from busi- nesses in 26 states. Responses from the sample’s 3,459 employer firms are featured in this report.2, The SBCS offers insight on business condi-tions and the credit environment from the perspective of small business owners. Thisreport sheds additional light on three sub- segments of the small business population—startups, microbusinesses, and growing firmsand growth in local and regional economies. 4 —each of which affects employment

Overall, the 2015 survey finds that for employer firms: FINANCING SUCCESSIMPROVED IN 2015 Both firm performance and financing success rates improved year over year. Still,- half of applicant firms reported financingshortfalls between Q3 2014 and Q3 2015, meaning they were approved for less thanthe amount requested. Microbusinesses and startups had the largest unmet financ ing needs with 63% and 58%, respectively,- reporting a financing shortfall. SMALL BANKS ARE THECHOICE LENDER Traditional bank lending continues to be the primary source of financing for small businesses. Credit applicants were most successful and most satisfied with their borrowing experience at small banks. Smallbanks approved at least some of the amount requested for 76% of applicants, while largebanks approved 58% of applicants. Further, small banks earned a satisfaction score (the net percent satisfied with their overall experience) of 75 among approved firms compared to a score of 51 for large banks.

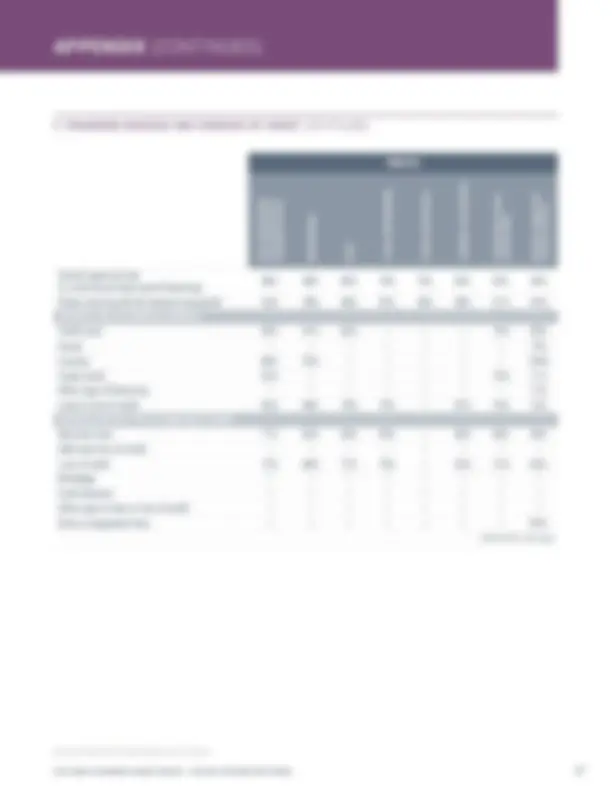

Overall, 20% of employer firms applied at an online lender. (^5) While the approval rate was relatively high for applicants (71% were approved for at least some credit), approved firms were not very satisfied with their experience. The satisfaction score was just 15—far below that of small and large banks.Dissatisfied firms reported concerns with high interest rates and unfavorable repay-ment terms. More detailed findings on employer firmsfrom the 2015 survey include: a. Cash flow is a common challenge for small firms. 22% of employer firms say managing cash flow is their top business challenge, above business costs and far above governmentregulations and taxes. Talent is an issue for growing firms. 24%say that finding/retaining qualified staff is their top challenge. b. The majority of employer respondents,63%, hold debt. Most debt is in small amounts and secured withpersonal assets. More than half hold $100K or less in debt. 63% of firms pledged personal assets or guarantee to secure debt. Use of personal assets as collateral is verycommon, even among larger and more mature firms. 58% of employer firms withmore than $10 million in revenues and 63% of firms that started 11 or more years ago used personal assets or guarantees to secure their financing.

1 See Office of Advocacy. "Small Business Lending in the United States," 2013. By Victoria Williams, Washington, D.C.: U.S. Small Business Administration, 2014.; "Federal Financial Institutions Examination Council (FFIEC) Consolidated Reports of Condition and Income" (Call Reports); and The Board of Governors of the 2^ Federal Reserve System. "Senior Loan Officer Opinion Survey on Bank Lending Practices."Employer firms are those reporting they have at least one employee, excluding the owner(s) and contract workers. 34 A subsequent report will focus on the self-employed respondents and is scheduled for release in Q2 2016.Startups are defined as firms 0-2 years of age. Microbusinesses are those with less than $100K in annual revenue. Growing firms are those reporting increased 5^ revenues and employment in the prior year, and that expect to maintain or increase the number of employees in the next 12 months.The questionnaire describes online lenders as nonbank online lenders including alternative and marketplace lenders.

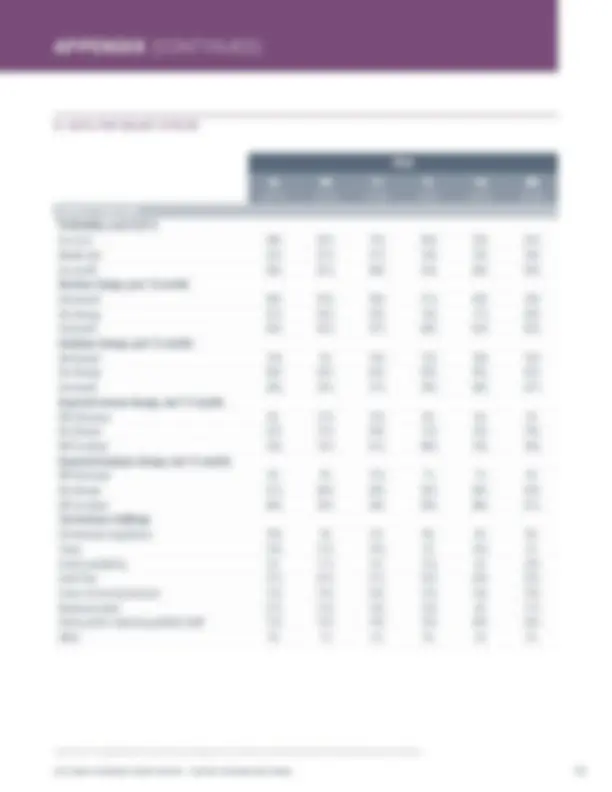

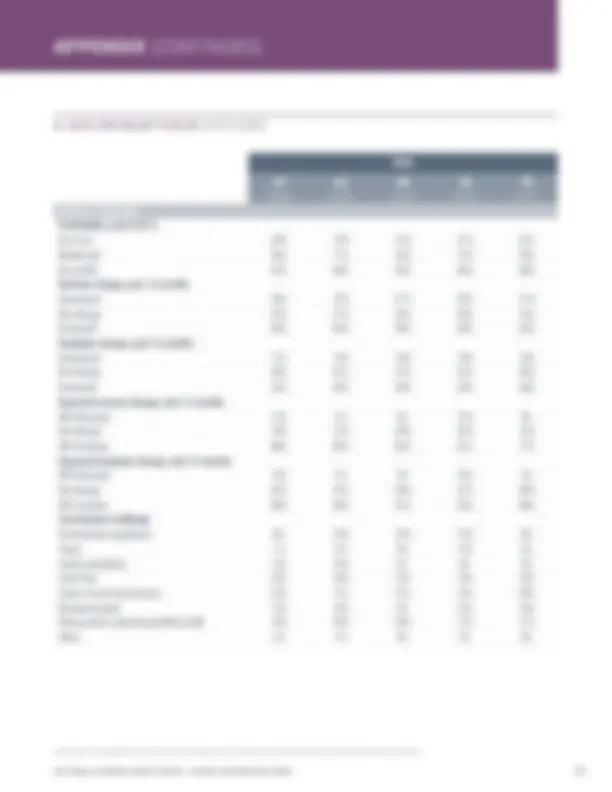

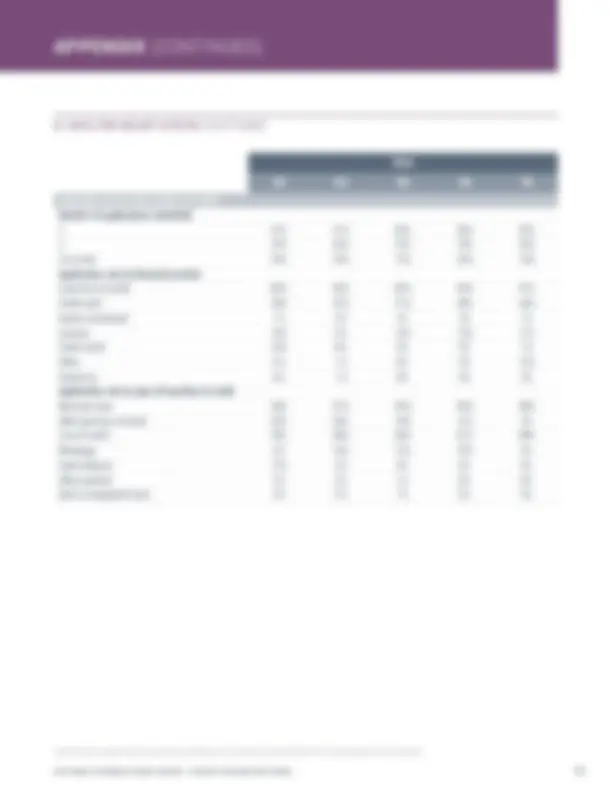

NUMBER OF EMPLOYEES (% of employer firms) N=3459 STATE DISTRIBUTION (% of employer firms) N=

INDUSTRY DISTRIBUTION (% of employer firms) N= Professional servicesand real estate Non-manufacturing goodsproduction and associated services Business support andconsumer services

Retail Healthcare and education Leisure and hospitality Finance and insurance Manufacturing

NYFL MANC GA OH PAAR TNAL CTIL INNJ KSMS MOSC VAKY LAME MDCA EMPLOYEES COTX

12 Source: Ewing Marion Kauffman Foundation. "The Importance of Young Firms for Economic Growth." By Jason Wiens and Chris Jackson. 2015.In this report, microbusinesses are defined as firms with <$100K in annual revenues. In the 2014 report, the definition included firms with up to $250K in annual revenues. 3 Source: The Aspen Institute, FIELD (Microenterprise Fund for Innovation, Effectiveness, Learning and Dissemination). "Microenterprise Development as Job Creation." By Elaine L. Edgecomb and Tamra Thetford. 2013. 45 Past 12 months. Approximately Q3 2014 through Q3 2015.Next 12 months. Q3 2015 through Q3 2016. 6 Source: Ewing Marion Kauffman Foundation. "The Importance of Young Firms for Economic Growth." By Jason Wiens and Chris Jackson. 2015.

Spotlight on key business types: Throughout the report, we highlight data on three groups of small businesses that affect employment and growth in local and regional economies. Understanding their challenges, credit needs, and credit experiences is important for their continued vitality.

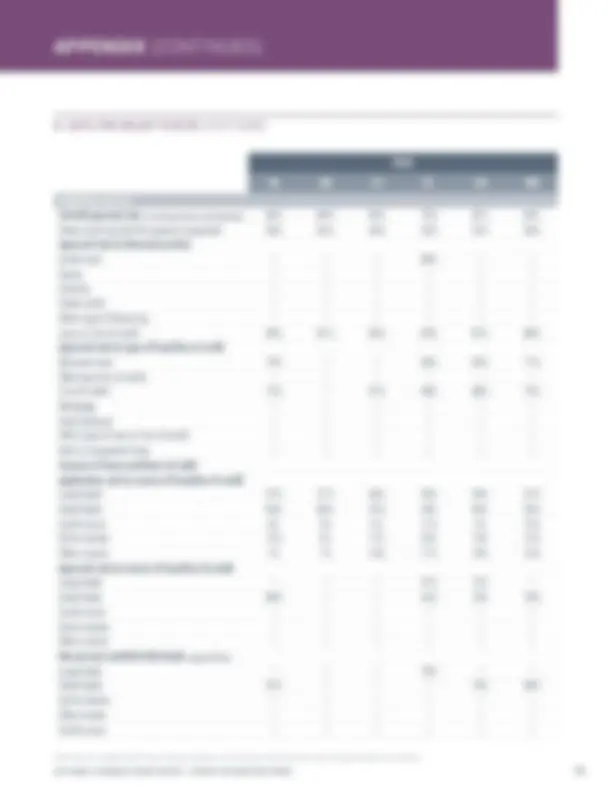

AGE OF FIRM (% of employer firms) N=3459 REVENUE SIZE OF FIRM (% of employer firms) N=

Startups New and young firms are the economy’s primary job creator. 1

Microbusinesses Microbusinesses create jobs for their owners and others—often workers disadvantaged in the broader labor market.2,

GROWING FIRMS (% of employer firms) N=

Defined as: Increased revenuesIncreased employees^44 Plan to increase or maintainnumber of employees 5

71% Not Growing 29% growing GrowthFirm

Growing Firms Growing small businesses are important enginesof dynamism in local economies—adding jobsand spurring innovation. 6

Small businesses are using contractors.

of employer firms use contract workers.

median number of contractors per employer firm.

12 Approximately Q3 2014 through Q3 2015.Expected change, Q3 2015 through Q3 2016.

CHANGE IN EMPLOYMENT (% of employer firms)

No change^ 51%

Decreased^ 14% Increased^ 34% 12 MonthsPast^1

45% Will increase

7%

Will decrease

12 MonthsNext^2

N=3386 N=

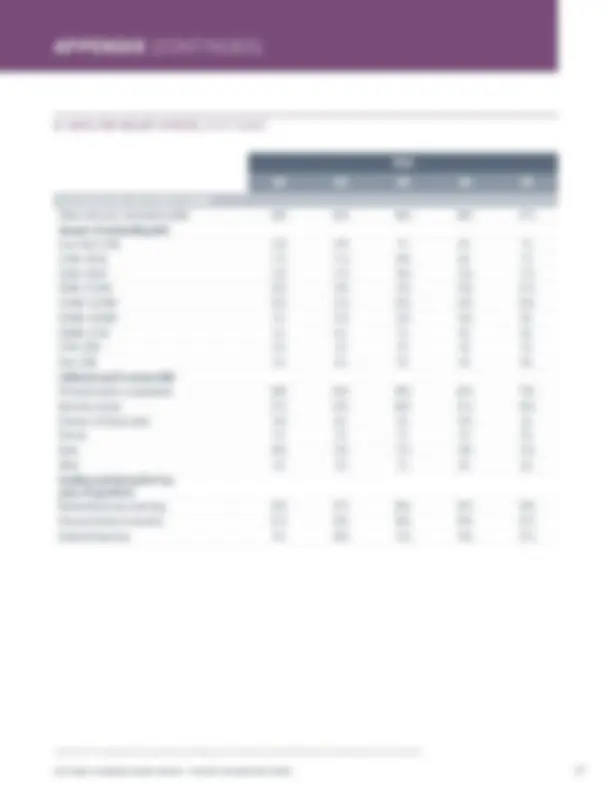

TOP BUSINESS CHALLENGE BY TYPE OF FIRM, In order of importance Past 12 Months^1 (% of employer firms)

Costs of running business

Growing N=803^2

Hiring and/or retaining qualified staff

Government regulations Taxes Credit availability Other^3

Startup (0–2 years) N=

Revenues/sales

Micro (<$100K) N= Cash flow 19% 17%

All firms N=

12 Approximately Q3 2014 through Q3 2015.Growing firms are defined as those with increased revenues over the past 12 months, increased employees over the past 12 months, 3 and plans to increase or maintain number of employees over the next 12 months.“Other” includes costs related to employee benefits, business climate, and market competition. Note: Because of rounding, percentages sum to >100%.

24% retaining staff is their top challenge to doing business. of growing employer firms reported that hiring and/or

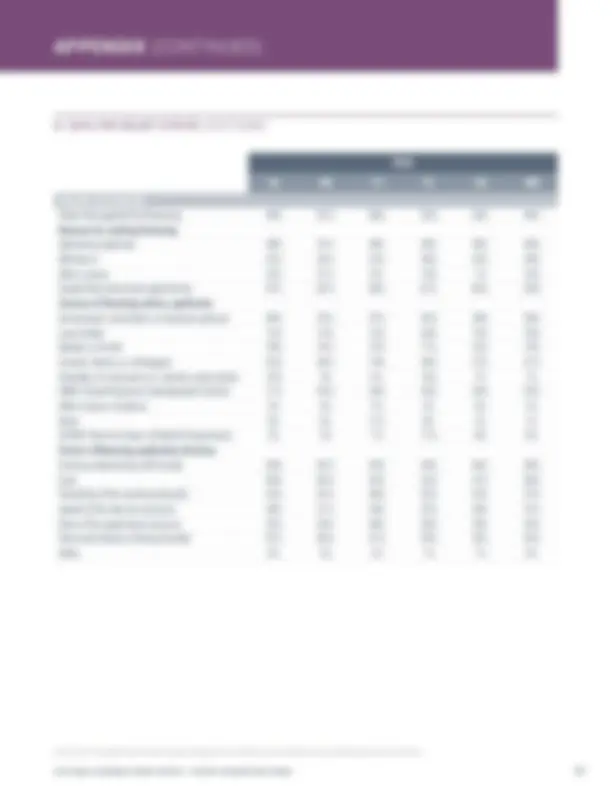

47% of employer firms applied for financing.

DEMAND FOR FINANCING (% of employer firms) N=

61% Expand business/new opportunity

37% Operating expenses

15% Other

24% Refinance

REASON(S) FOR APPLYING (% of applicants)^2 N=

53% Didn't Apply Applied^ 47% 12 MonthsPast^1

12 Approximately Q3 2014 through Q3 2015.Respondents could select multiple answers. 3 Growing firms are defined as those with increased revenues over the past 12 months, increased employees over the past 12 months, and plans to increase or maintain number of employees over the next 12 months.

61% of applicants were borrowing to expand their business or pursue a new opportunity.

DEMAND FOR FINANCING BY TYPE OF FIRM

Application rate (^) (% of employer firms) Expand business/new opportunity (^) (% of applicants) Operating expenses (^) (% of applicants)

All firms N=3454 Micro (<$100K) N=

Startup (0–2 years) N=

Growing N=949^3

Application rate

Reason(s) for applying

53% of employer firms did not apply for financing.

PRIMARY REASON FOR NOT APPLYING (% of non-applicants) N= 49% Sufficient financing

25% Debt averse 16% Discouraged 5% Other

3% 3% Search too difficultCredit cost high

53% Didn't Apply Applied^ 47%

25% of non-applicants did not apply because they were averse to taking on debt.

12 Months^ Past 1

12 Approximately Q3 2014 through Q3 2015.Growing firms are defined as those with increased revenues over the past 12 months, increased employees over the past 12 months, 3^ and plans to increase or maintain number of employees over the next 12 months.Discouraged firms are those that did not apply for financing because they believed they would be turned down.

DEMAND FOR FINANCING (% of employer firms) N=

DISCOURAGED AND DEBT AVERSE BY TYPE OF FIRM (% of non-applicants)

Discouraged^3 Debt averse

All firms N=1763 Growing N=401^2 Startup (0–2 years) N=152 Micro (<$100K) N=

Microbusinesses are less likely to seek financing, and more likely to be discouraged and debt averse.

12 Select answer choices shown. See appendix for more detail. Respondents could select multiple options.Growing firms are defined as those with increased revenues over the past 12 months, increased employees over the past 12 months, and plans to increase or maintain number of employees over the next 12 months.

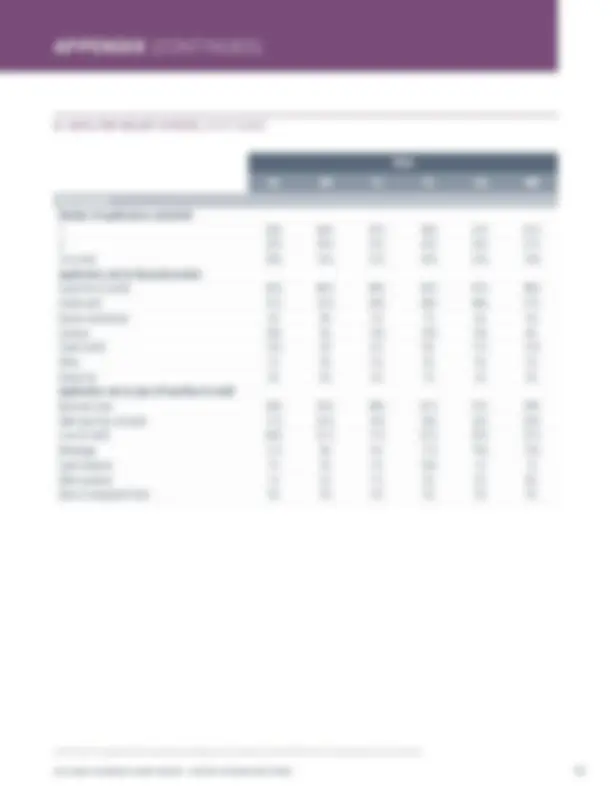

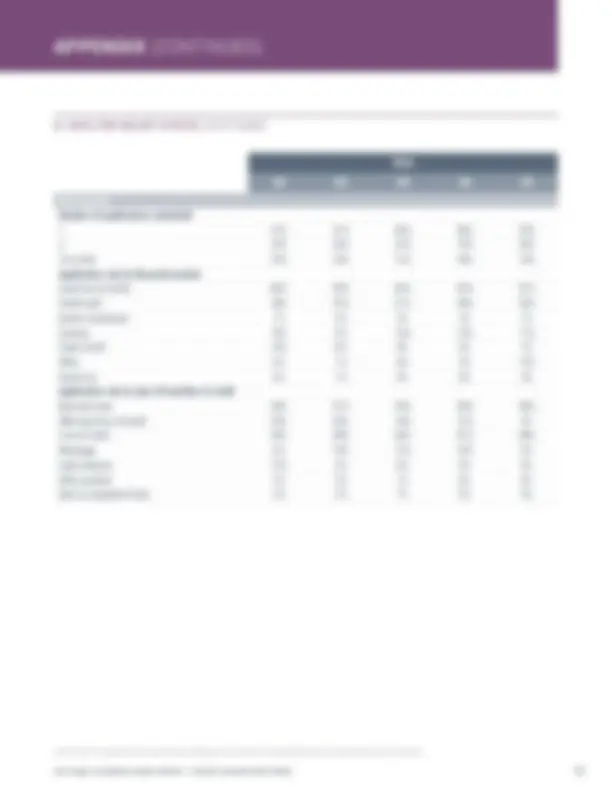

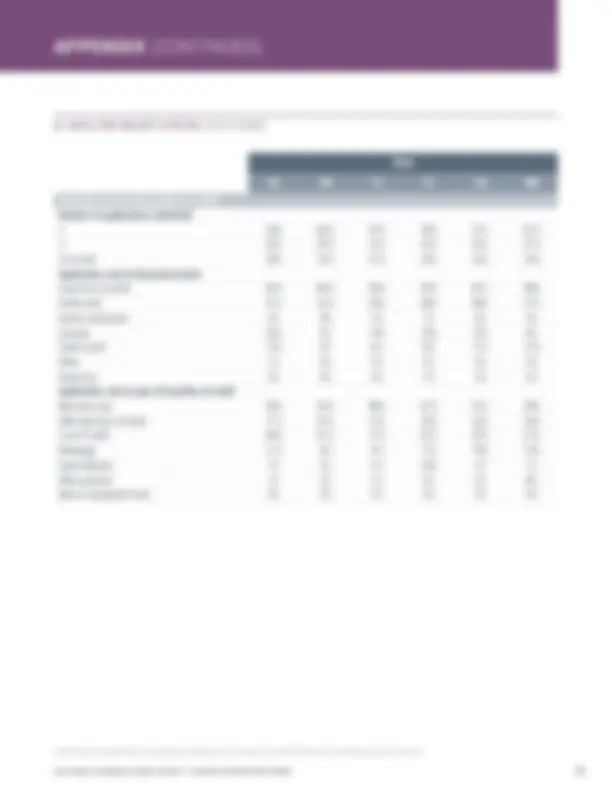

APPLICATIONS^1 FOR LOANS AND LINES OF CREDIT BY TYPE OF FIRM (% of loan/line of credit applicants)

All firms N=

Micro (<$100K) N=

Startup (0–2 years) N=

Growing N=490^2

Line of creditBusiness loan SBA loan/line of credit Commerical mortgage Merchant cash advance

Microbusinesses and startups are more likely toapply for SBA-backed loans or lines of credit and merchant cash advances than larger revenue firms.

Employer firms primarily base their application decisions on relationships with lenders and the price of credit.

TOP TWO FACTORS^1 INFLUENCING WHERE FIRMS APPLY Micro (<$100K) N=148 $100K–$1M N=635 $1M–S10M N=629 >$10M N=

12 Select answer choices shown. See appendix for more detail. Respondents could select multiple options."Online lenders" are defined as nonbank alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.

Banks are the dominant credit source overall but online lending is a noteworthy source for employer firms with less than $1 million in revenues.

CREDIT SOURCES^1 APPLIED TO BY REVENUE SIZE OF FIRM (% of loan/line of credit applicants)

All firms N=

Micro (<$100K) N=

Small bankLarge bank Online lender Credit union^2 53% 58% 1%6%

42% 52% 9% 20%

45% 59% 4% 11% 39% 52% 9% 22% 41%44% 14% 30%

Price

Perceived chance of being funded

Microbusinesses are more likely to make applicationdecisions based on perceived chance of funding. Existing relationship with lender

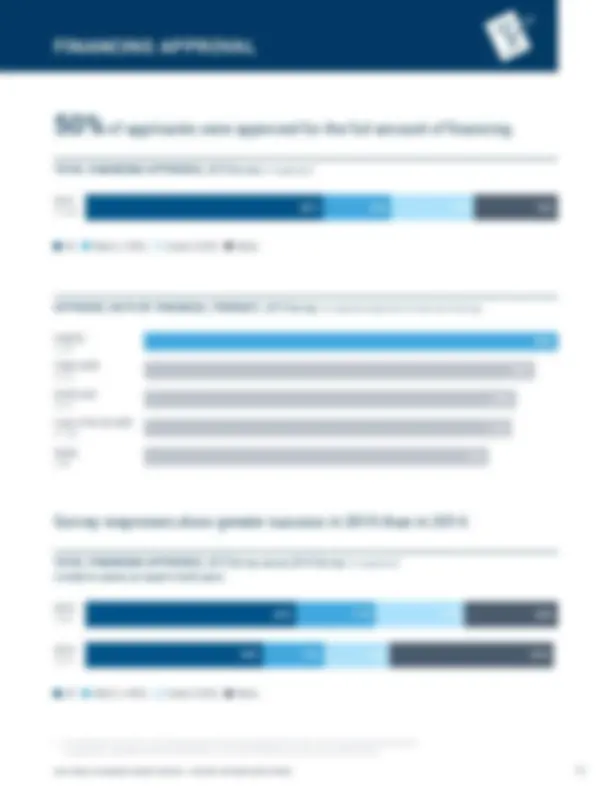

50% of applicants were approved for the full amount of financing.

1 Firms that were unsure how much they were approved for are excluded from the chart. In 2014, the approval rate pertainedto applications submitted in the first half of the year. In 2015, the time period was the previous twelve months.

TOTAL FINANCING APPROVED, 2015 Survey (% of applicants)^1

(^2015) N=1580 50% 14% 18% 18%

All Most (>=50%) Some (<50%) None

Survey responses show greater success in 2015 than in 2014.

All Most (>=50%) Some (<50%) None

TOTAL FINANCING APPROVED, Limited to states surveyed in both years 2015 Survey versus 2014 Survey (% of applicants)^1

APPROVAL RATE BY FINANCIAL PRODUCT, 2015 Survey (% of applicants approved for at least some financing) Leasing N= Trade credit N= Credit card N= Loan or line of credit N= Equity N=

Applicants that were approved for financing from small banks reported the highest satisfaction.

LENDER SATISFACTION SCORE 1 (% of firms approved at source) Small bank N= Credit union N= Large bank N= Online lender N=140^2 Other N=117^3

Dissatisfied firms reported issues with banks’ application processes and online lenders’ interest rates.

12 Satisfaction score is the share satisfied with lender minus the share dissatisfied."Online lenders" are defined as alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital. 34 "Other" includes government loan funds and community development financial institutions.Respondents could select multiple options. 5 Select answer choices shown due to low observation count.

SUCCESSFUL APPLICANTS' REASON(S) FOR DISSATISFACTION, (% of employer firms dissatisfied with lender)^4 Select Lenders^5

Online lender N= Small bank N= Large bank N=

Lack oftransparency

Long wait forcredit decision Difficult applicationprocess Unfavorablerepayment terms

High interest rate

33% 45%

32% 22%

22% 43%

51% 16% 18%

21% 51% 70%

52% 15% 15%