¡Descarga Accounting and Information systems y más Apuntes en PDF de Administración de Empresas solo en Docsity!

Topic 1: Accounting and Information

Systems

Topic 1

a

Accounting and Information Systems

Topic 1: Accounting and Information

Systems

Course Syllabus

Accounting and Information Systems

The Accounting Equation

The Recording Process

The Accounting Cycle

Inventories

Accounting of Basic Transactions

Topic 1: Accounting and Information

Systems

Evaluation

a

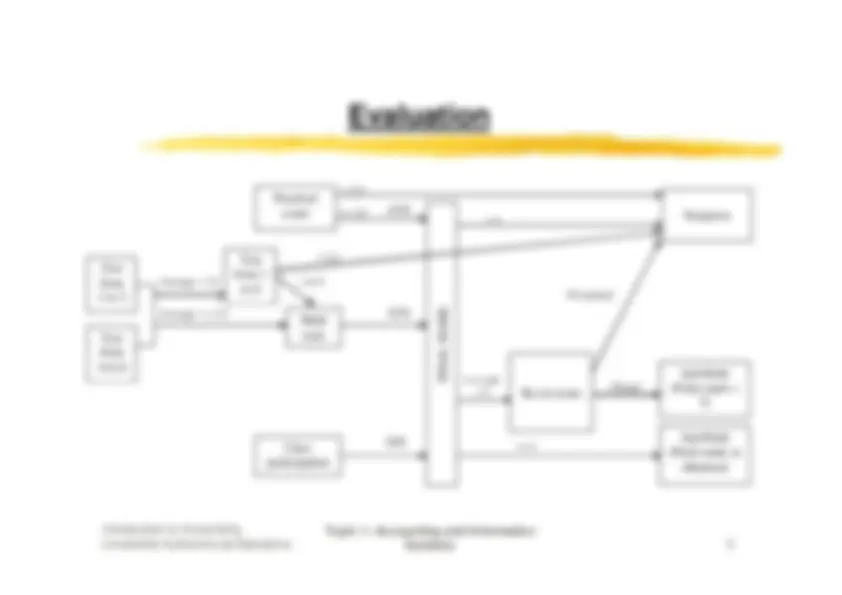

10% of the final mark: Class participation

a

45% of the final mark: Mean of two theoretical tests

a

45% of the final mark: Practical exam

Dates: a

th

of March: First theoretical test

a

st

of May: Second theoretical test

a

th

of June: Practical exam

a

th

of June: Re-sit exam

Topic 1: Accounting and Information

Systems

Evaluation

Introduction to AccountingUniversitat Autònoma de Barcelona

< 3,

= 5

= 3,

=3,

Average < 3,5Average > = 3,

Passed

Not passed

< 4

= 4 and

< 5

< 3,

Test from 1 to 3

Test from 4 to 6

Test

from 1

to 6

Mark

tests

Class

participation

FINAL MARK

Re-sit exam

Aprobado

(Final mark as

obtained) Aprobado

(Final mark =

Suspenso

Practical

exam

Topic 1: Accounting and Information

Systems

Topic 1: Accounting and Information Systems

a

Accounting Concept.

a

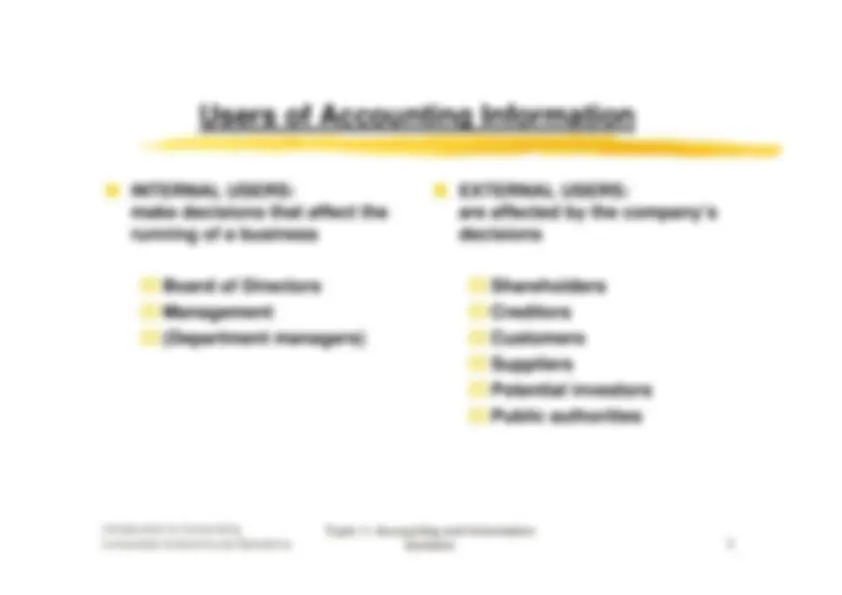

Users of Accounting Information.

a

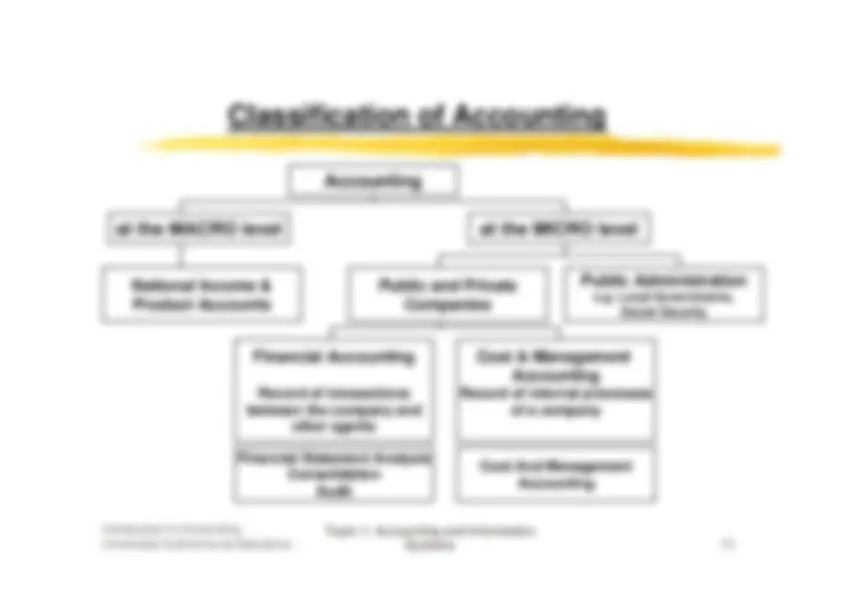

Classification of Accounting.

a

Stages in the Accounting Cycle.

a

The Financial Statements.

a

Limitation of Accounting Data.

a

Requirements for Accounting Information.

Topic 1: Accounting and Information

Systems

Accounting as an Aid to Decision Making

a

Accounting …

`

is an information system that

`

measures business activities,

`

processes information, and

`

communicates financial information.

`

is useful to anyone who must make judgments and decisions that haveeconomic consequences.

Event

Accountant’s

Analysis and

Recording

Financial

Statements

Users

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 1: Accounting and Information

Systems

Classification of Accounting

Accounting

at the MACRO level

at the MICRO level

National Income &

Product Accounts

Public and Private

Companies

Public Administration

e.g. Local Governments,

Social Security

Financial Accounting

Record of transactions

between the company and

other agents

Cost & Management

Accounting

Record of internal processes

of a company

Financial Statement Analysis

Consolidation

Audit

Cost And Management

Accounting

Topic 1: Accounting and Information

Systems

Financial versus Management Accounting

Financial

Accounting

Management

Accounting

Users

External parties(e.g. shareholders,creditors, ...)

Internal parties(e.g. managers, executive,...)

Regulations

Constrained by laws, rules(e.g. Directives de la U.E.,CÒDI DE COMERÇ, Llei deS.A., Pla General deComptabilitat)

No constraints (relevantand in time)

Application

Compulsory

Voluntary

Time span

At least once a year.Information is punctual.

Flexibledaily, weekly, quarterly, ...

Type ofinformation

Financial data

Financial and Nonfinancialdata

Topic 1: Accounting and Information

Systems

International Accounting Standards (IAS) –

Situation in Spain

a

01/01/2005: Compulsory use of IAS/IFRS for consolidatedstatements of listed companies.

a

The ICAC (Instituto de Contabilidad y Auditoria de Cuentas) isadapting the Plan General de Contabilidad to the IAS.

a

From 2008 all companies have to apply a new Plan General deContabilidad adapted to the IAS.

Topic 1: Accounting and Information

Systems

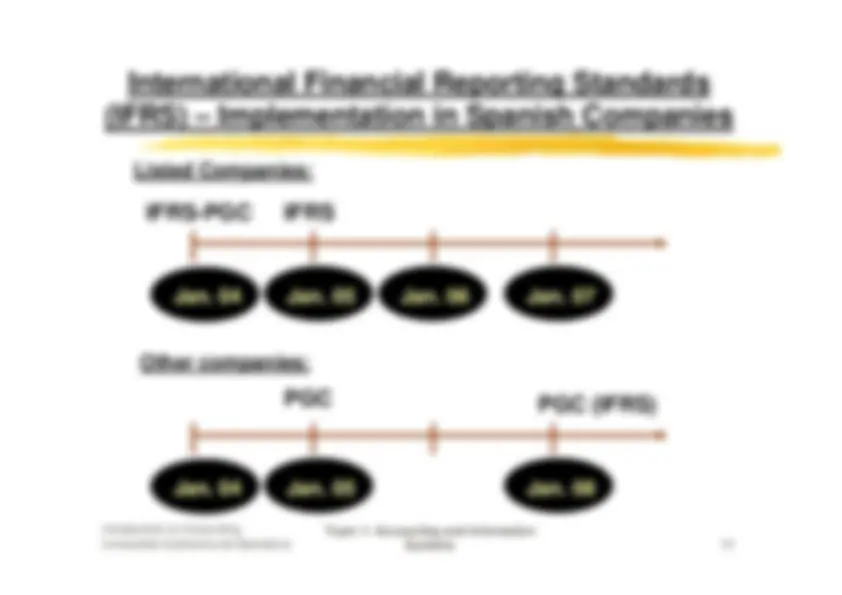

International Financial Reporting Standards

(IFRS) – Implementation in Spanish Companies

Jan. 04

Jan. 05

Jan. 06

Jan. 07

Listed Companies:

IFRS-PGC

IFRS

Jan. 04

Jan. 05

Jan. 08

Other companies:

PGC

PGC (IFRS)

Topic 1: Accounting and Information

Systems

Stages in the Accounting Process

1. Data collectionIdentify relevantaccountingtransactions

Checks,

invoices

contracts,

certificates,

notes...

2. Data preparation

and processing

Valuation inmonetary units

Recording

Classification andAggregation

Journal

Ledger

3. Information •

Financial Statements

Auditing

Communication

Analysis

Balance Sheet,Income Statement,Statement of Cash-Flows, Statement ofShareholders’ Equityand Notes

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 1: Accounting and Information

Systems

The Basic Financial Statements

a

Balance Sheet:Information on the financial condition of a business at a certain moment (end of a period).

a

Income Statement:Information on the income (profit or loss) of a business during a certain period. It reflectsthe wealth generated by the company in a given period.

a

Statement of Cash-Flows:Information on the origin and use of cash in the company.

a

Statement of Shareholders’ Equity:Presents the individual components of Shareholders’ Equity and the changes during thelast year.

a

Notes:Information on the criteria, principles and norms used in the balance sheet and incomestatement. Other data on the company.

Topic 1: Accounting and Information

Systems

Requirements for Accounting Information

a

Content:

Relevance

Does it affect users’ decisions?

Reliability

Is it representationally faithful, neutral, free from material error,

prudent and complete?

a

Presentation:

Comparable

Inter- and intra-company comparisons

Understandable

Presented as understandably as possible

a

Information must also be:

Material

Timely