¡Descarga The accounting cycle y más Apuntes en PDF de Administración de Empresas solo en Docsity!

Topic 4: The Accounting Cycle

Topic 4: The Accounting Cycle

Accounting Principles

The Accounting Cycle

Opening Stage

Development Stage

Adjustment Stage (Deferrals, Accruals, Depreciation)

Closing Stage

Topic 4: The Accounting Cycle

Accounting Principles

Going-concern Assumption The firm is a

going concern

- one that will continue in operation

indefinitely. Partially justifies acquisition cost principle rather than liquidation or exit value basis.

Accrual Basis of Accounting Method of recognizing revenues when goods are sold/delivered orservices are rendered independently of payment; expenses whenoccurred independently of payment. Note: Accrual vs. Cash accounting In cash accounting, transactions are recorded when cash is received (revenues) or paid (expenses)

Topic 4: The Accounting Cycle

Accounting Principles

Relative Significance Principle Accounting reports should disclose enough information in order notto mislead careful readers about financial matters. Specialdisclosures about changes in expectations, changes in significantcontractual relations, or new activities can be found in the body of thefinancial statements, in the auditor’s opinion, or in the notes to thestatements.

Topic 4: The Accounting Cycle

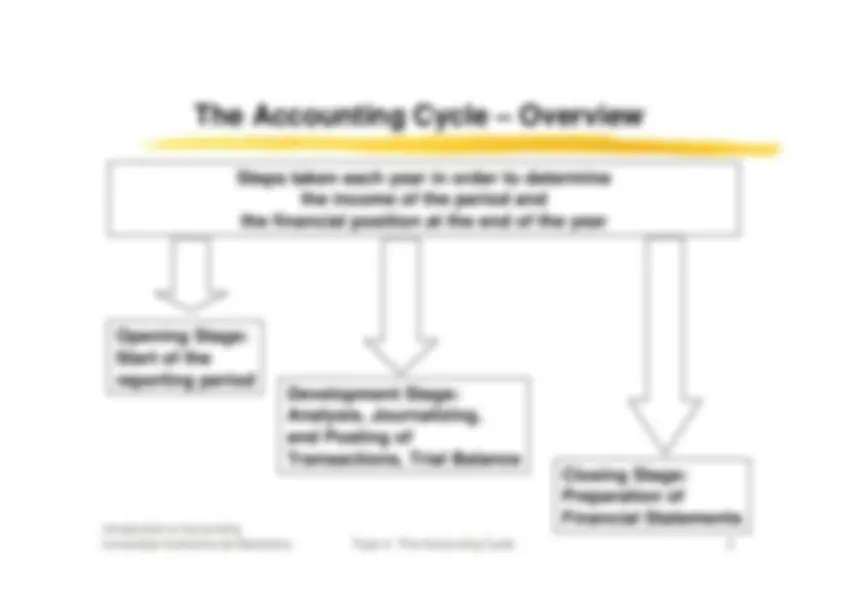

The Accounting Cycle – Overview

Steps taken each year in order to determine

the income of the period and

the financial position at the end of the year

Opening Stage: Start of the reporting period

Development Stage: Analysis, Journalizing, and Posting of Transactions, Trial Balance

Closing Stage: Preparation of Financial Statements

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 4: The Accounting Cycle

Development of the

Accounting Cycle

Beginning from the starting balances: Recording of the transactions during the

Period in the journal and the ledger

to

The Journal

The Ledger A

o^

OE

o

L

o

t

A

u

A

t

OE

u

OE u

L

t

L

t

A

u

OE

u

L

ExpensesLosses

u

A

t

OE t

L

Revenues

Gains

Dr.

Cr.

E Lo

R G

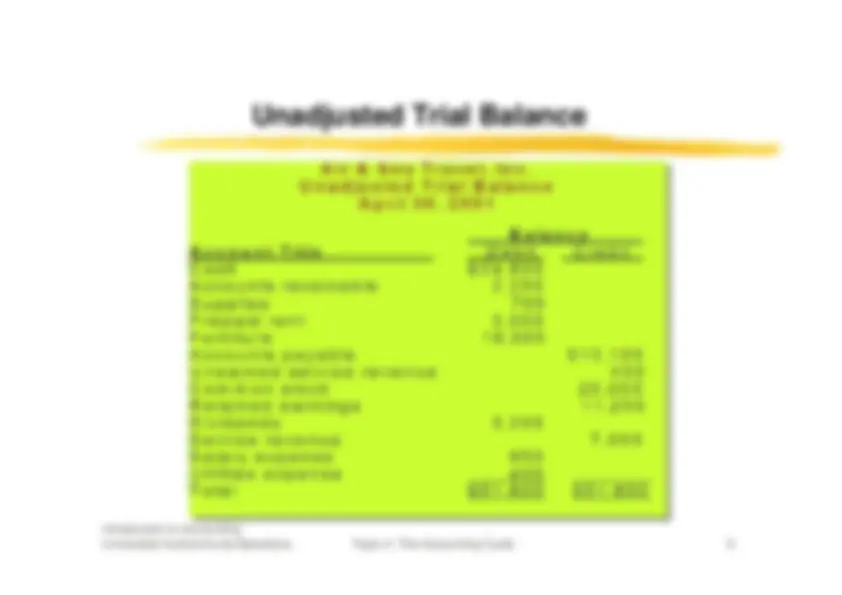

Unadjusted Trial Balance (sums and balances) (before adjustments and corrections)

Dr. … Debit side (“Debitor”), Cr. … Credit Side (“Creditor”) E … expenses, Lo … losses, R … revenues, G … gains

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 4: The Accounting Cycle

Adjustments

Operations before the “final” closing

Recording some transactions in order to adjust the financial positionat the end of the period (Depreciation/Amortization, Periodification, Regulation of the Inventories, Reclassifications)

to

The Journal

The Ledger A

o^

OE

o

L

o

t

A

u

A

t

OE

u

OE u

L

t

L

t

A

u

OE

u

L

ExpensesLosses

u

A

t

OE t

L

Revenues

Gains

Dr.

Cr.

E Lo

R G

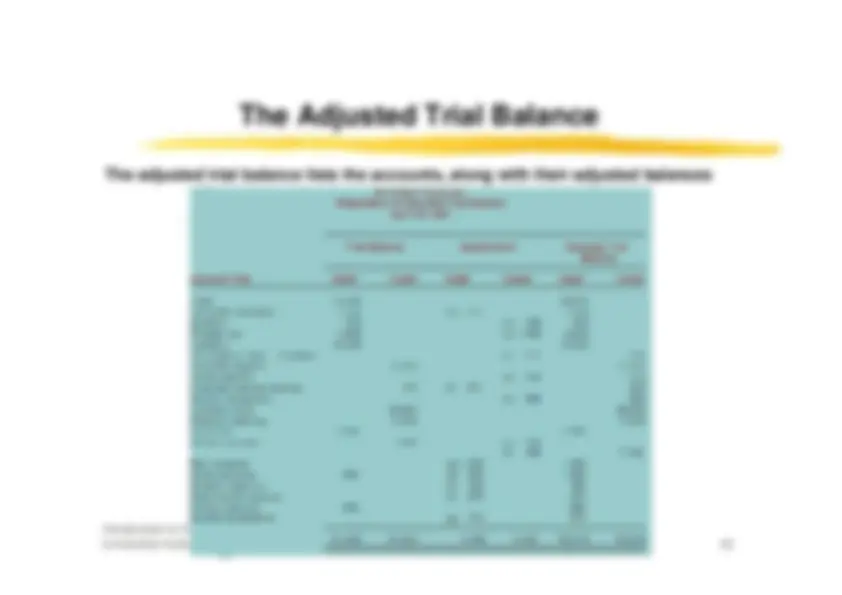

Adjusted Trial Balance (sums and balances) (after adjustments andcorrections)

Topic 4: The Accounting Cycle

Adjustments for Revenues and Expenses

Matching Principle of Revenues and Expenses

Matching the related expenses and revenues of a period.

Revenues of the Period

Expenses of the Period necessary

to generate the revenues

Topic 4: The Accounting Cycle

Adjustments for Revenues and Expenses

Adjusting entries can be grouped into three basiccategories:

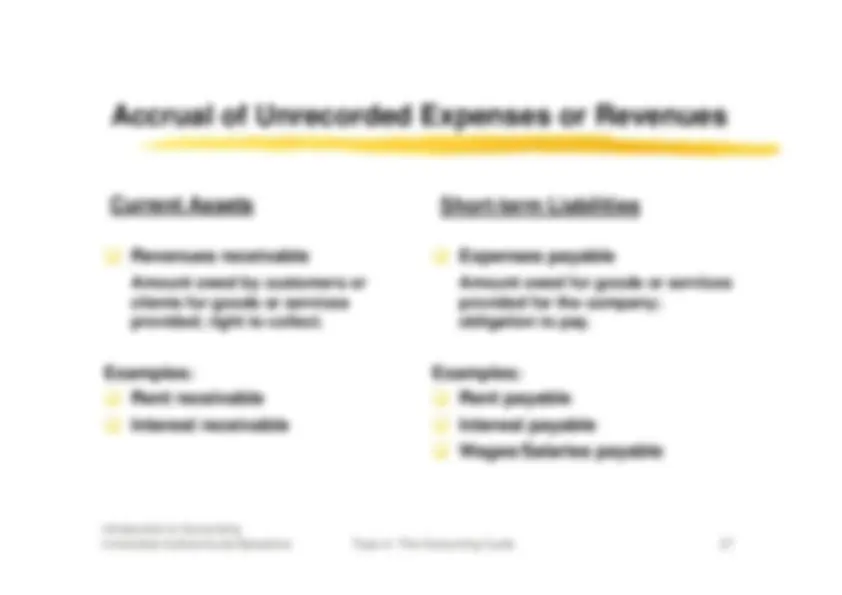

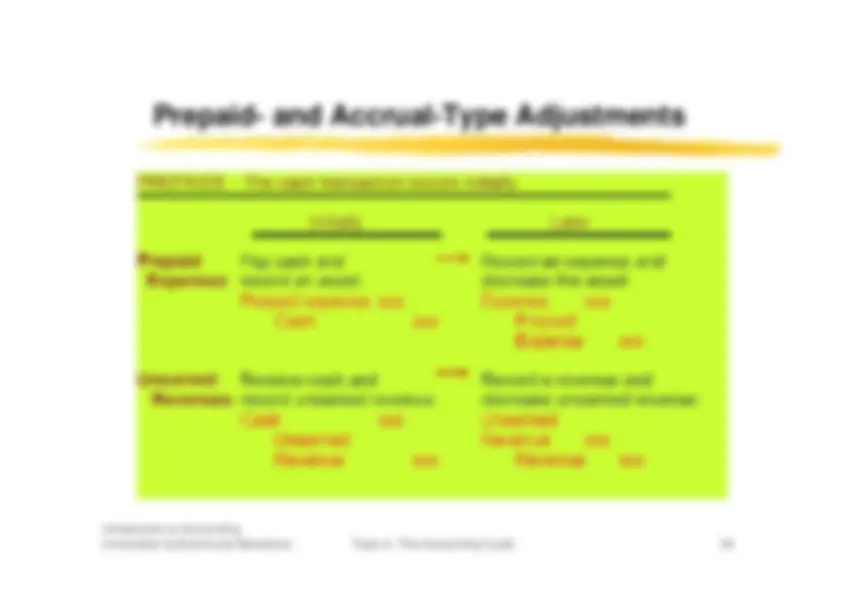

Deferrals (prepaid expenses, unearned revenues)

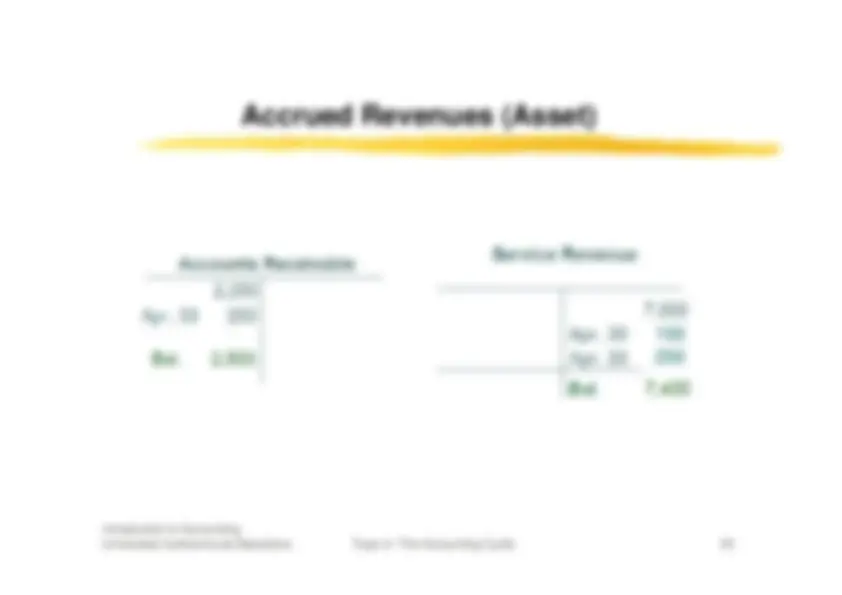

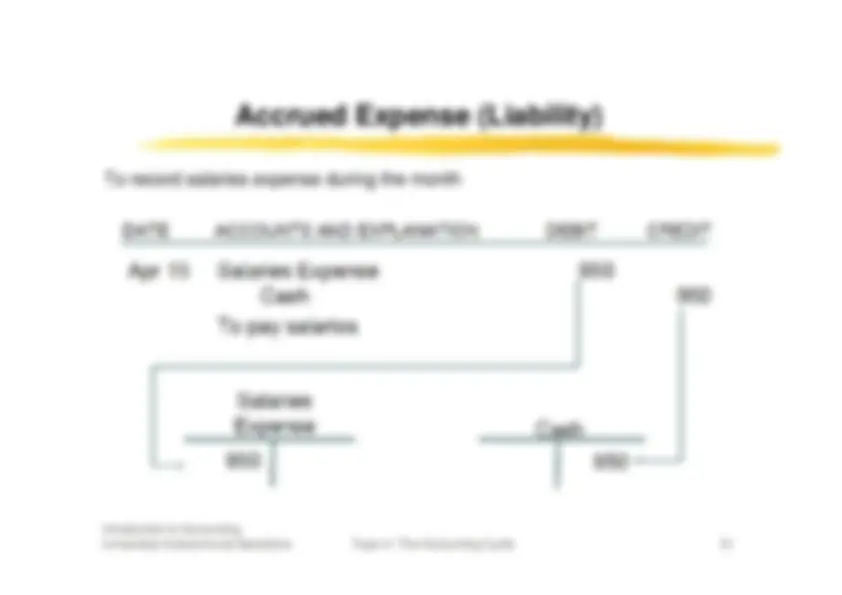

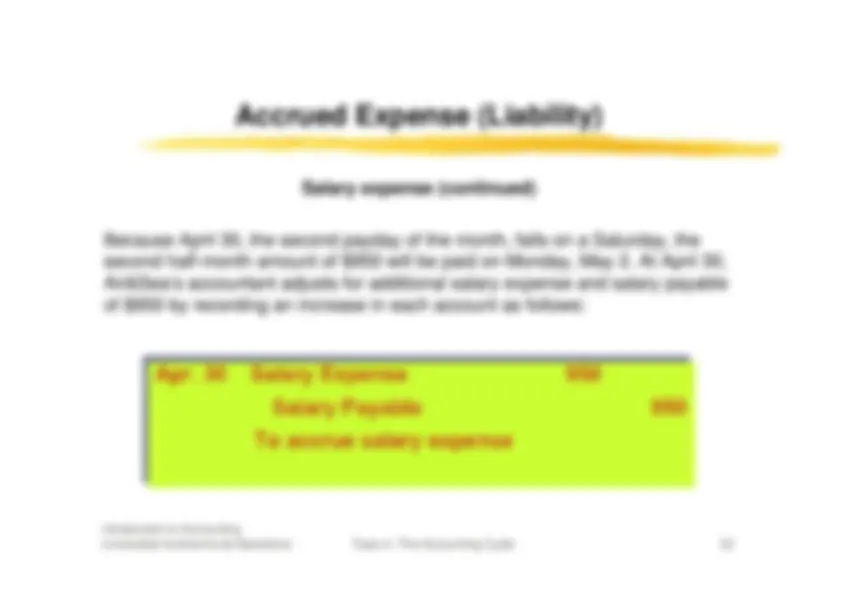

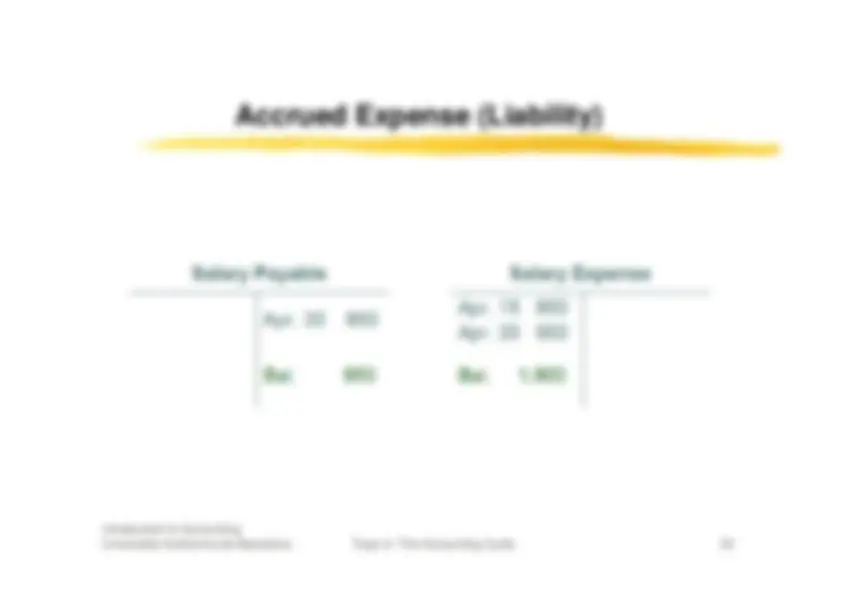

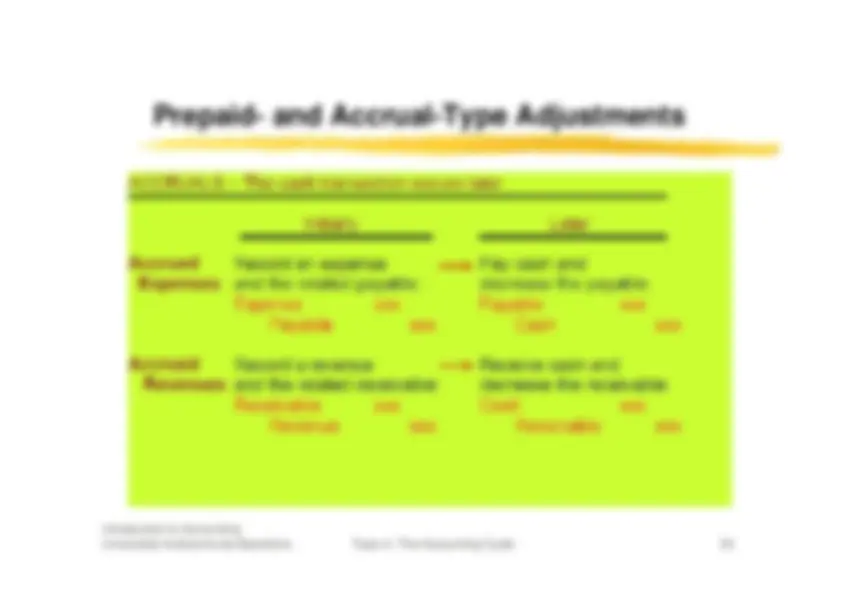

Accruals (accrued expense, accrued revenue)

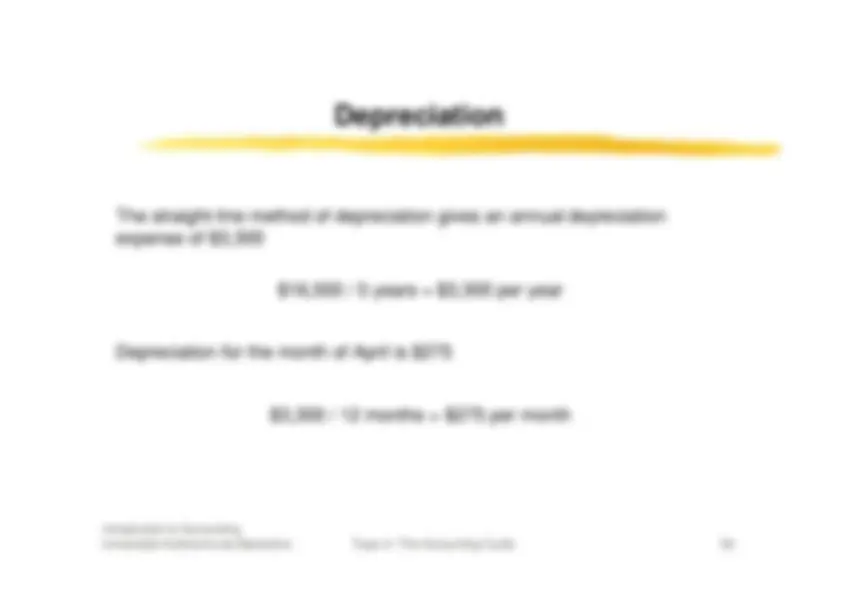

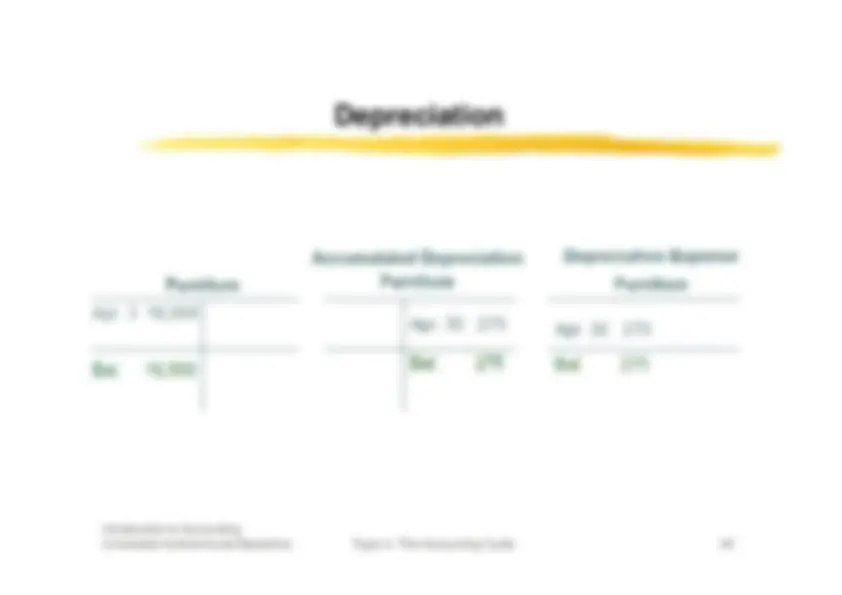

Depreciation

Topic 4: The Accounting Cycle

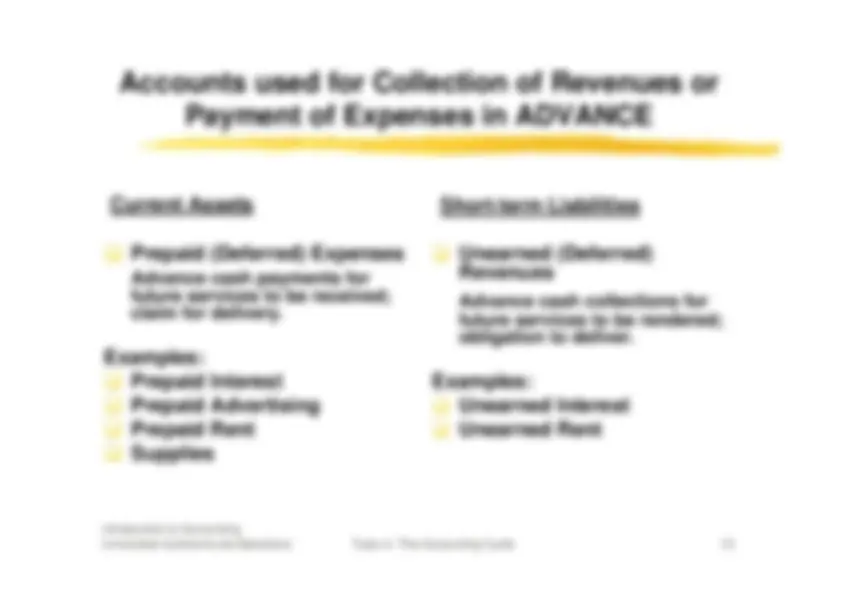

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

Prepaid (Deferred) ExpensesAdvance cash payments forfuture services to be received;claim for delivery.

Examples:

Prepaid Interest

Prepaid Advertising

Prepaid Rent

Supplies

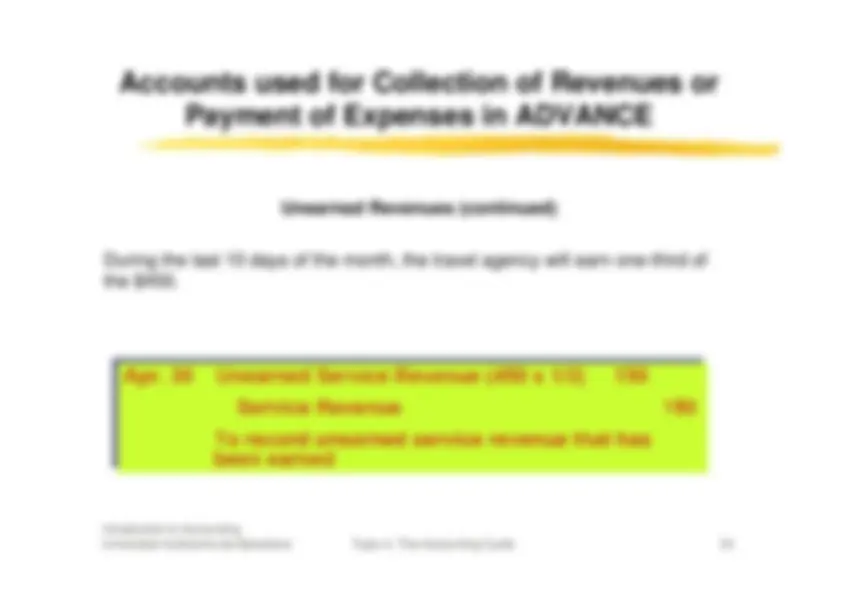

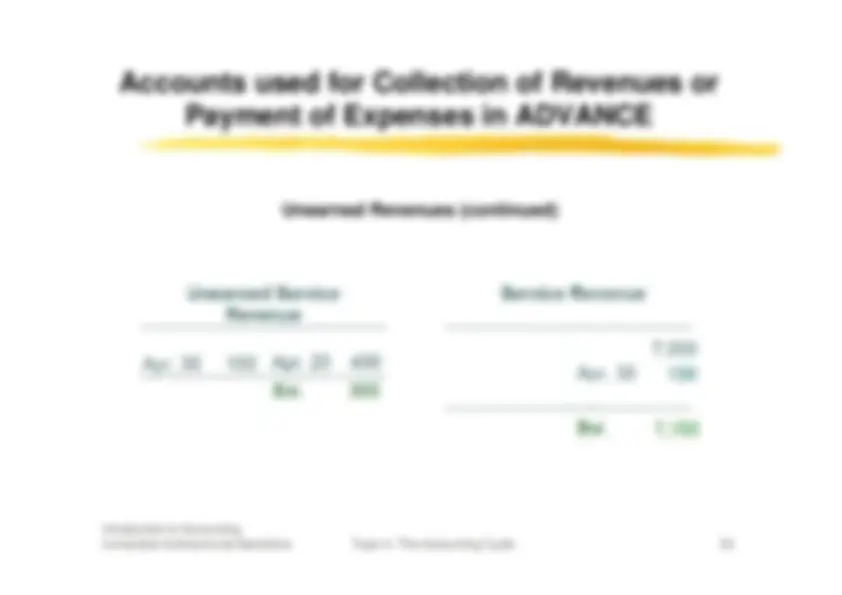

Unearned (Deferred)RevenuesAdvance cash collections forfuture services to be rendered;obligation to deliver.

Examples:

Unearned Interest

Unearned Rent

Current Assets

Short-term Liabilities

Topic 4: The Accounting Cycle

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

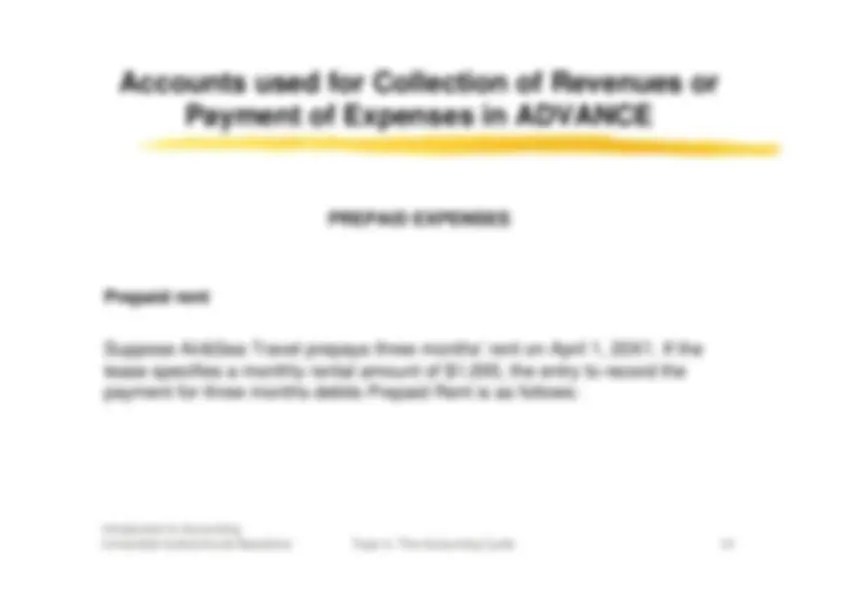

PREPAID EXPENSES

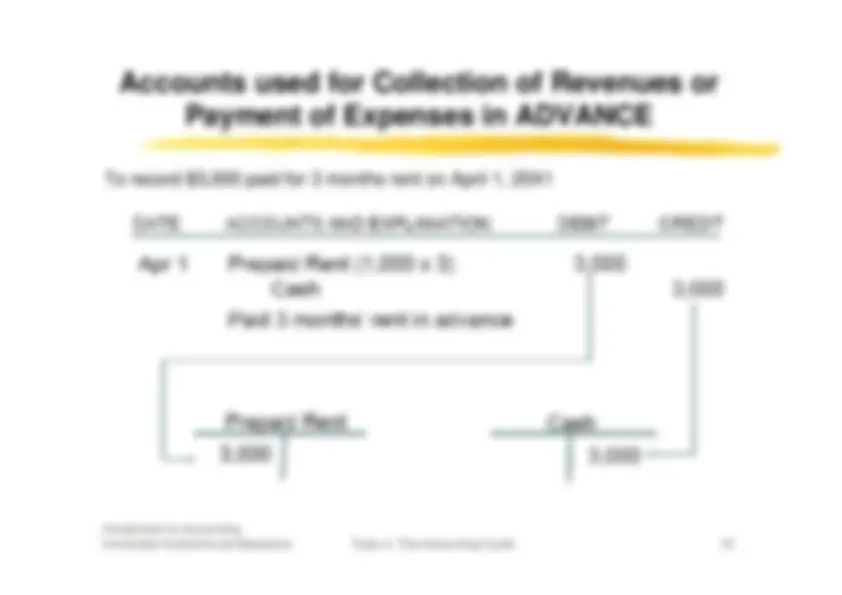

Prepaid rent Suppose Air&Sea Travel prepays three months’ rent on April 1, 20X1. If thelease specifies a monthly rental amount of $1,000, the entry to record thepayment for three months debits Prepaid Rent is as follows:

Topic 4: The Accounting Cycle

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

PREPAID EXPENSES (continued)

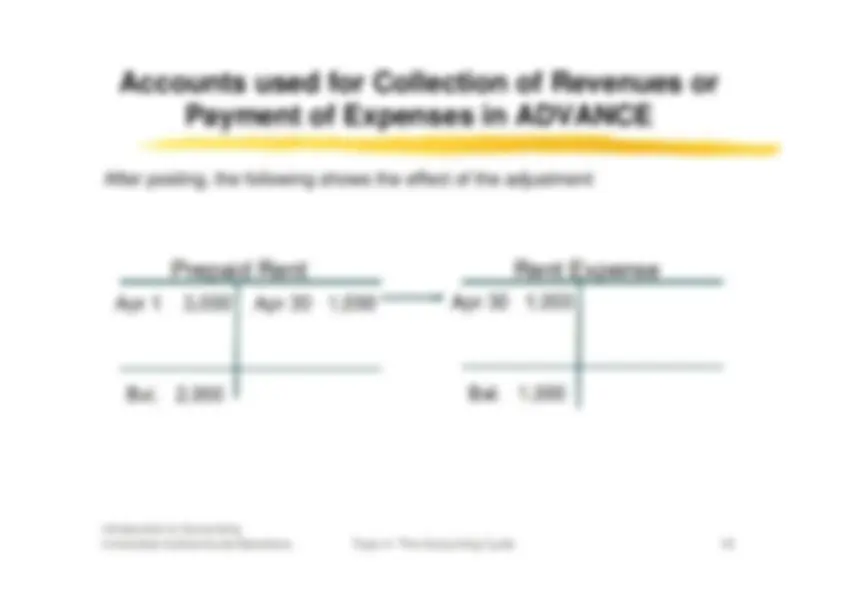

Prepaid rent (continued) At April 30, Prepaid rent is adjusted to remove one month’s expense from theasset account.

Topic 4: The Accounting Cycle

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

To adjust for one month’s rent expired at April 30

Topic 4: The Accounting Cycle

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

PREPAID EXPENSES

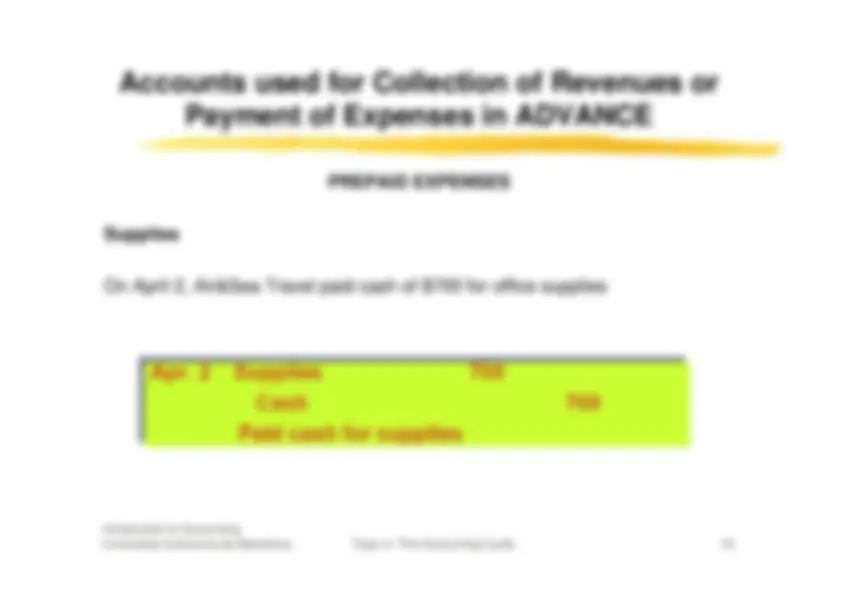

Supplies On April 2, Air&Sea Travel paid cash of $700 for office supplies

Topic 4: The Accounting Cycle

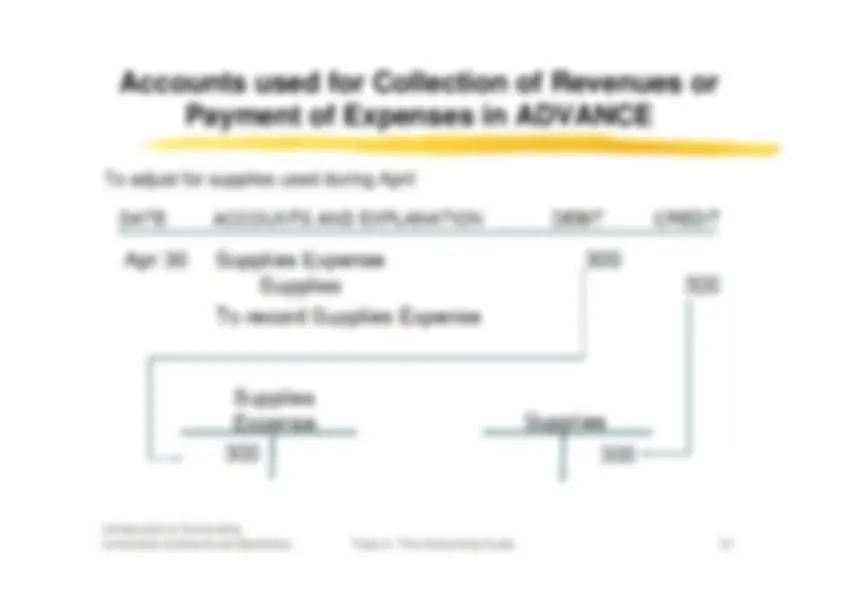

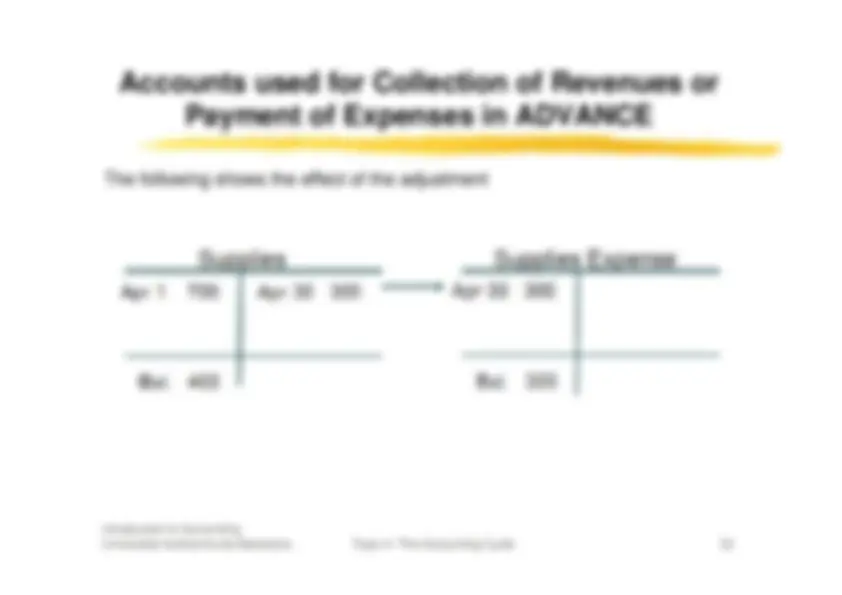

Accounts used for Collection of Revenues or

Payment of Expenses in ADVANCE

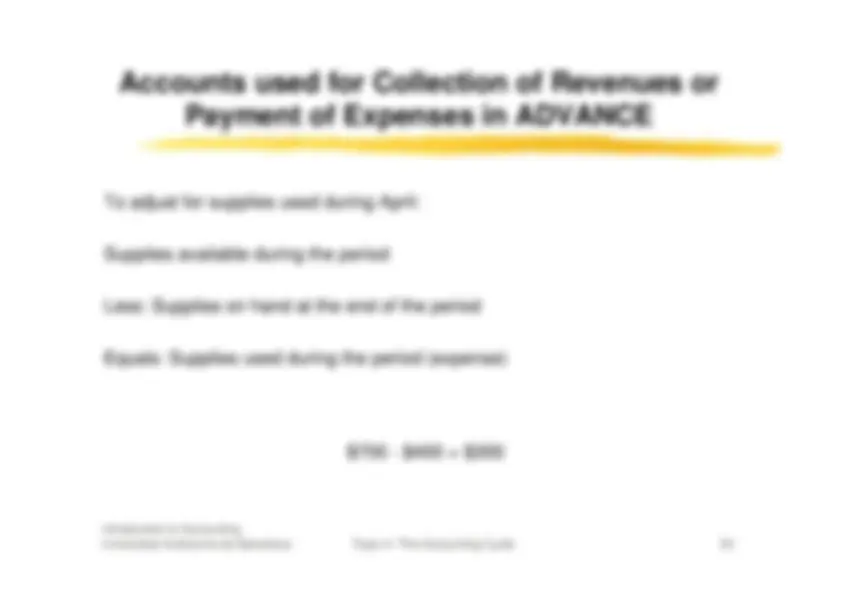

To adjust for supplies used during April: Supplies available during the period Less: Supplies on hand at the end of the period Equals: Supplies used during the period (expense)