¡Descarga The Accounting equation y más Apuntes en PDF de Administración de Empresas solo en Docsity!

Topic 2: The Accounting Equation

Topic 2: The Accounting Equation

a

The Accounting Equation

a

The Balance Sheet

a

The Profit and Loss Account

a

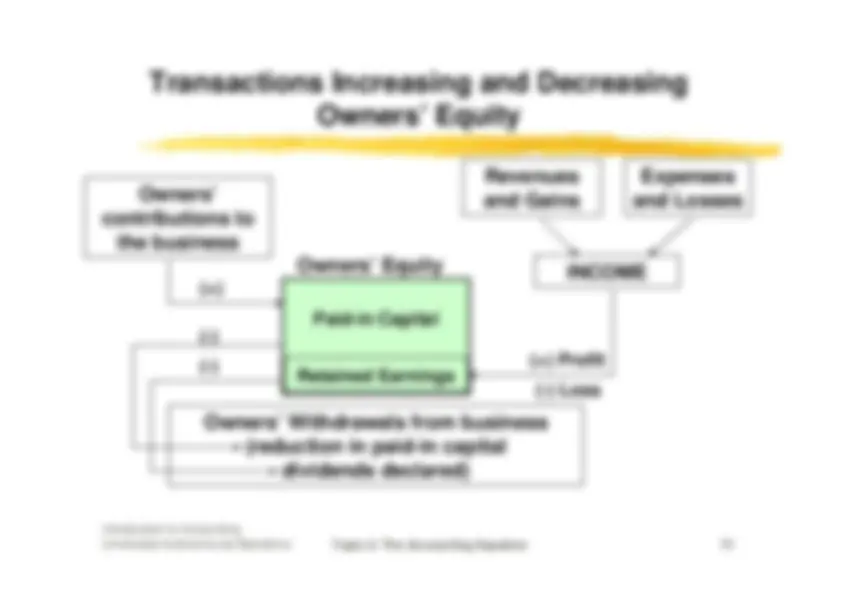

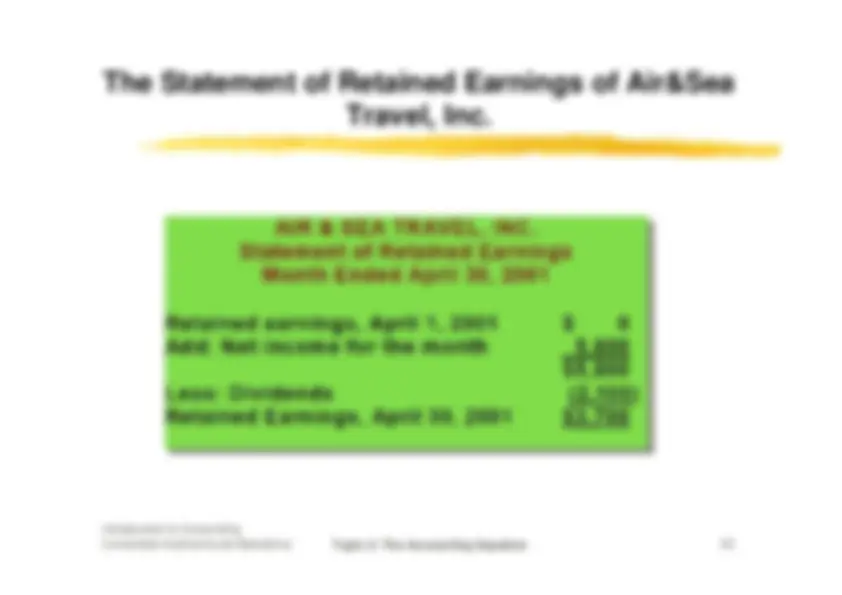

The Statement of Retained Earnings

a

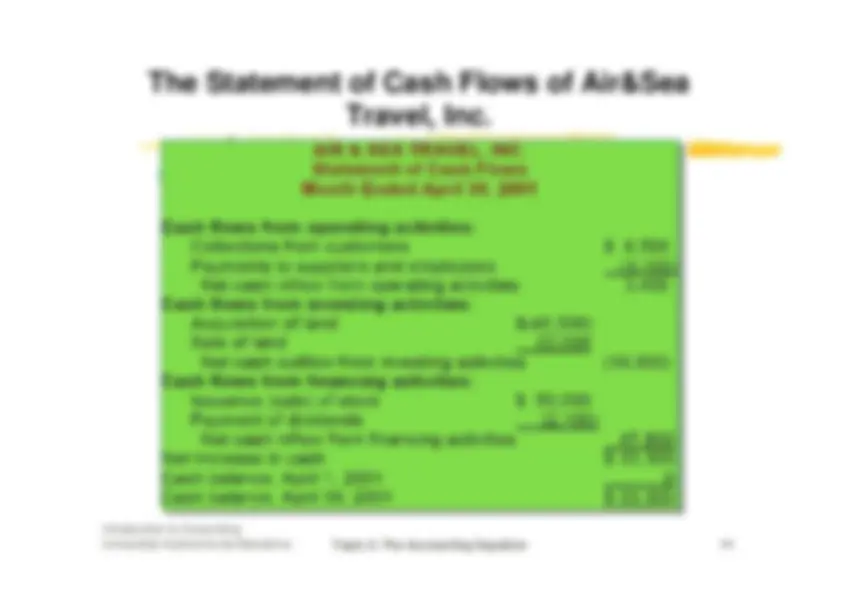

The Statement of Cash Flows

a

Analysis of Business Transactions

Topic 2: The Accounting Equation

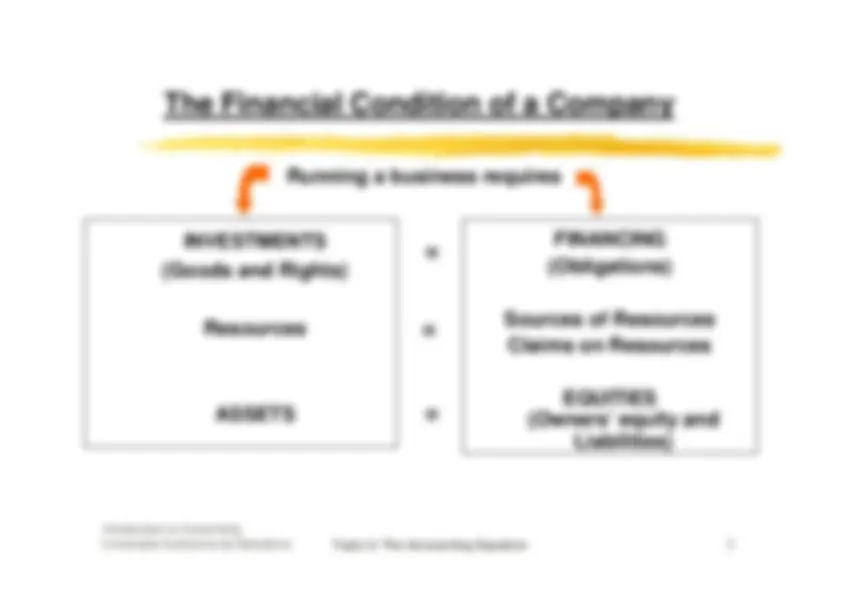

The Financial Condition of a Company

Making Investments a

Land and Buildings

a

Equipment, Machinery

a

Vehicles, Trucks

a

Computers

a

Patents, trade marks,contractual rights, computersoftware

a

Financial investments insecurities

a

Inventories

a

Accounts receivable (Credits tocustomers)

a

Cash and Checking account

Obtaining Financing a

Funds from owners (owners’ orshareholders’ equity)

a

Subsidies

a

Bank Loan (short- or long-term)

a

Accounts payable to ...(Credits from suppliers, banks,employees, ...)

a

Taxes payable

Running a business requires

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 2: The Accounting Equation

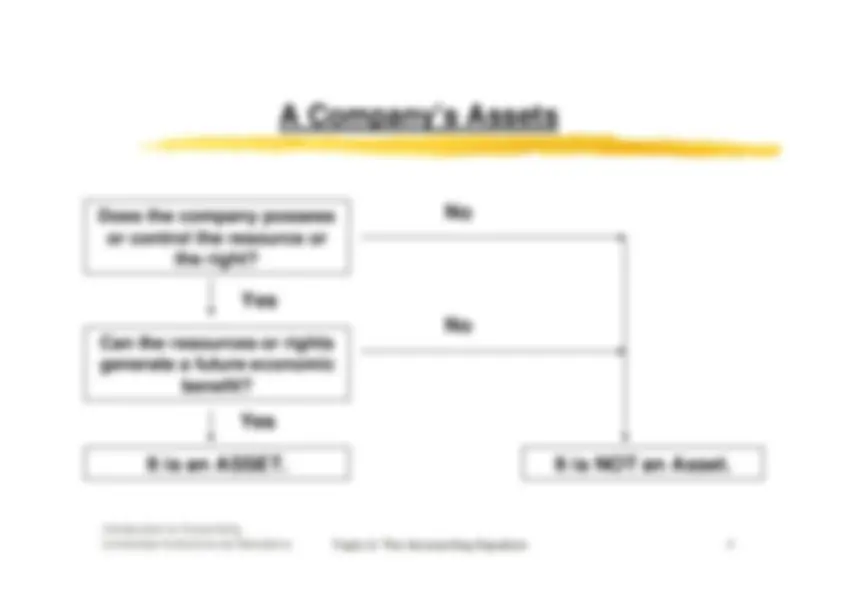

A Company’s Assets

Can the resources or rightsgenerate a future economic

benefit?

Yes

It is an ASSET.

Yes

It is NOT an Asset.

Does the company possess

or control the resource or

the right?

No No

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 2: The Accounting Equation

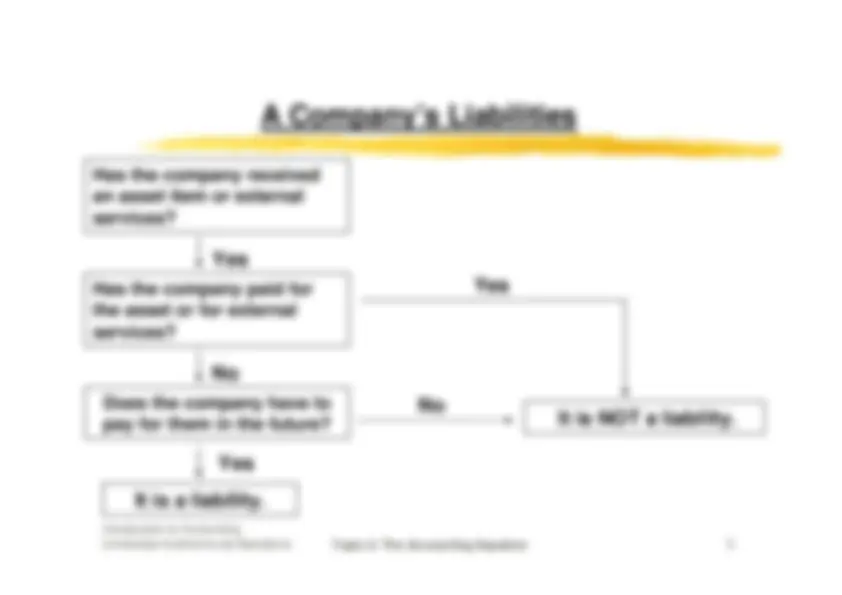

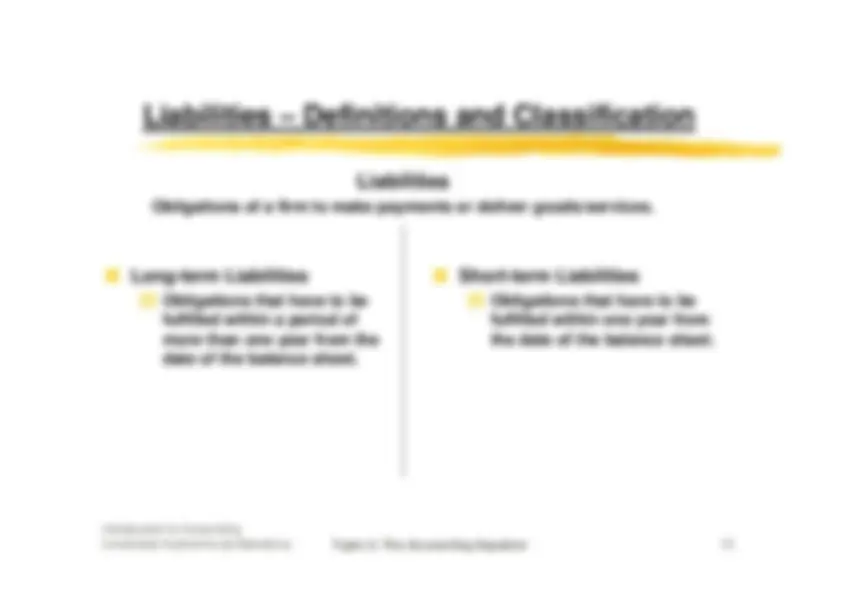

A Company’s Liabilities

Has the company receivedan asset item or externalservices?

Yes

Has the company paid forthe asset or for externalservices?

No

Does the company have topay for them in the future?

It is a liability.

Yes

It is NOT a liability.

Yes

No

Topic 2: The Accounting Equation

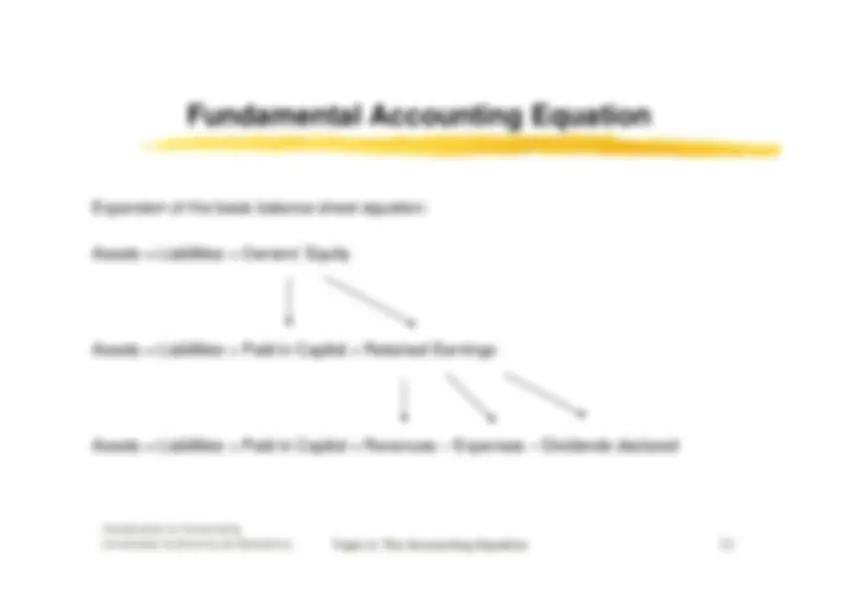

The Balance Sheet and

The Balance Sheet Equation

Assets

Liabilities

Owners’ Equity

(Net worth)

INVESTING

How are the funds

used?

Resources

Assets

FINANCING

Where do the funds

come from?

Sources of Resources

Equities

(Liabilities and Owners’

Equity)

Balance Sheet on Dec. 31, 2…

Assets

Equities

Topic 2: The Accounting Equation

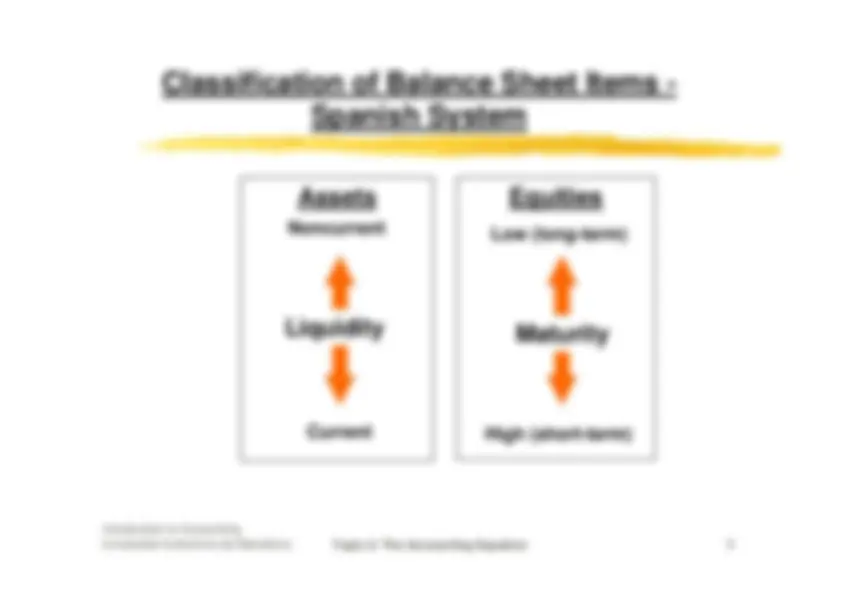

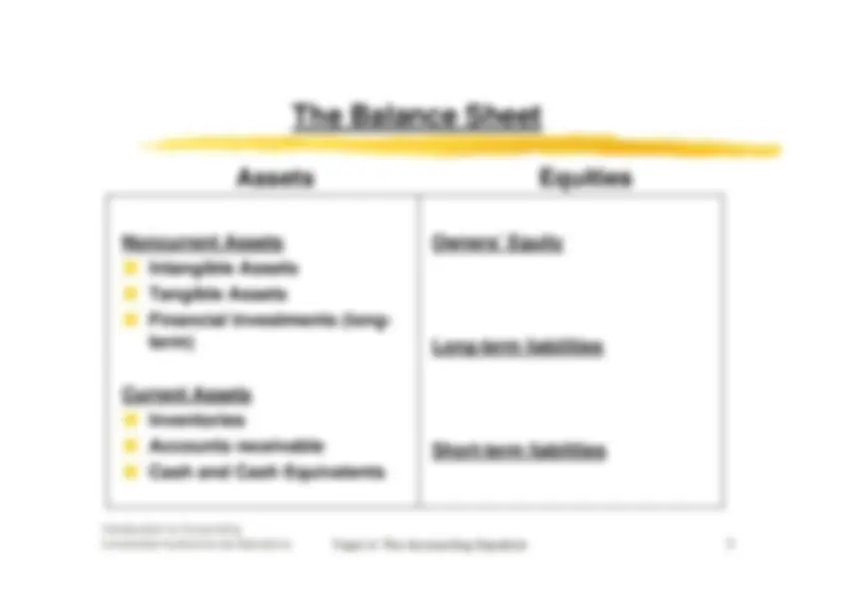

Classification of Balance Sheet Items -

Spanish System

Assets

Equities

Noncurrent

Current

Low (long-term) High (short-term)

Liquidity

Maturity

Topic 2: The Accounting Equation

El Balance de Situación

ACTIVO

No corriente a

Intangible

a

Material

a

Financiero

Corriente a

Existencias

a

Realizable

a

Disponible

FONDOS PROPIOS Y

PASIVO

Neto o No ExigibleExigible (Pasivo) a largo plazoExigible (Pasivo) a corto plazo

Topic 2: The Accounting Equation

a

Noncurrent Assets

`

Resources held and used forseveral years.

a

Current Assets

`

Resources expected to beturned into cash, sold orconsumed within less than oneyear from the date of thebalance sheet.

Assets – Definitions and Classification

Assets

Resources of a firm that are expected to provide future benefits to the firm.

Topic 2: The Accounting Equation

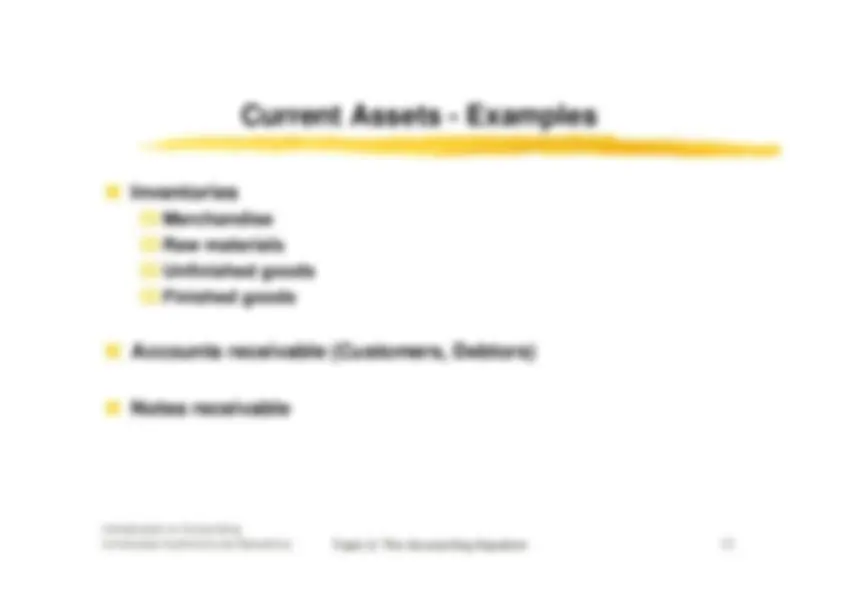

Current Assets - Examples

a

Inventories

`

Merchandise

`

Raw materials

`

Unfinished goods

`

Finished goods

a

Accounts receivable (Customers, Debtors)

a

Notes receivable

Topic 2: The Accounting Equation

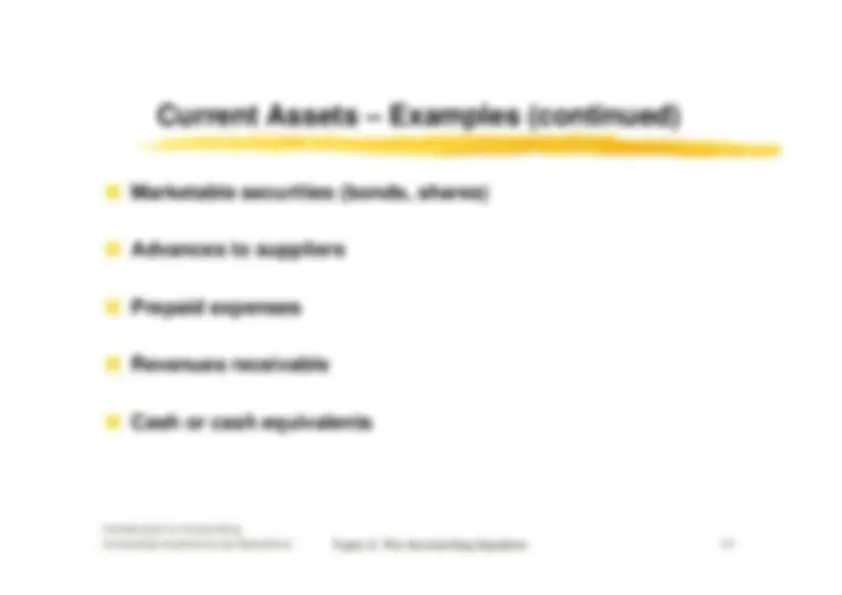

Current Assets – Examples (continued)

a

Marketable securities (bonds, shares)

a

Advances to suppliers

a

Prepaid expenses

a

Revenues receivable

a

Cash or cash equivalents

Topic 2: The Accounting Equation

Liabilities - Examples

a

Accounts payable to …

a

Suppliers, Creditors

a

Notes payable

a

Advances from customers

a

Unearned revenues

a

Expenses payable

a

Bonds payable

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 2: The Accounting Equation

Valuation of Assets and Liabilities

a

Assets

At Acquisition Price orProduction Costs

Lower of cost or Market Rule

Acquisition Price higher thanMarket Value

Æ

Market Value

Acquisition Price lower than MarketValue

Æ

Acquisition Price

a

Liabilities

At Repayment Price

Recognize all obligationsalready established andthose which can only beestimated

Introduction to AccountingUniversitat Autònoma de Barcelona

Topic 2: The Accounting Equation

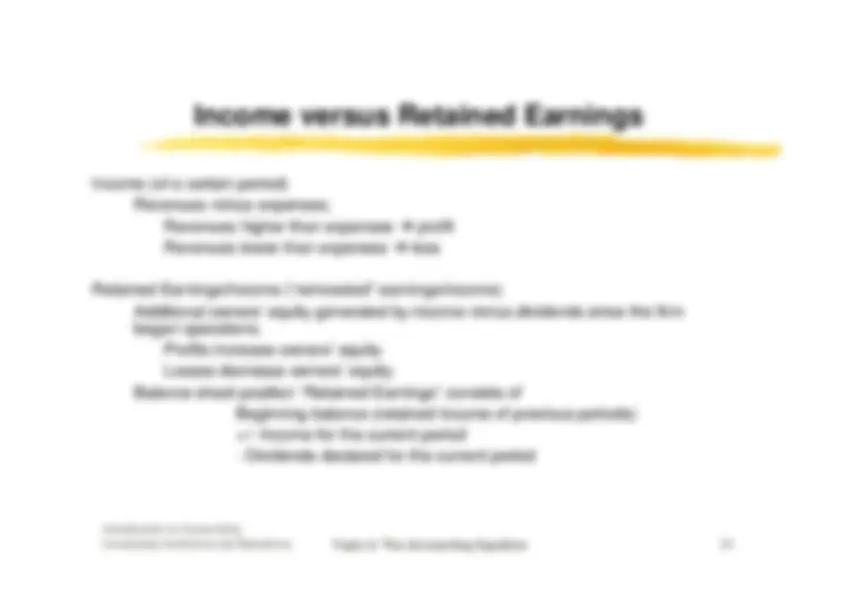

The Accounting Time Period

Performance is measured over discrete time periods1.

Calendar year versus fiscal yearFiscal year: year that does not end on December 31, chosen according to low pointin annual business activity.

Interim periods – quarterly, monthly basis

Topic 2: The Accounting Equation

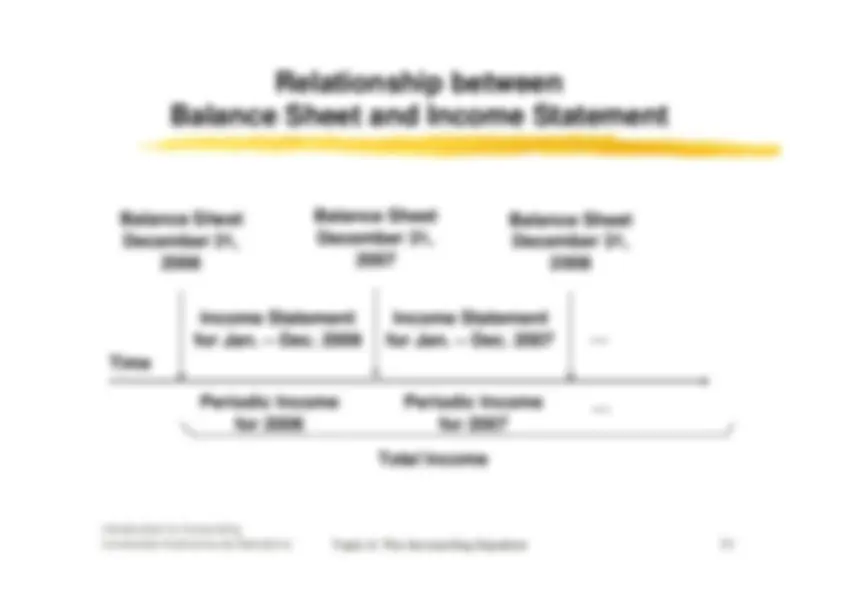

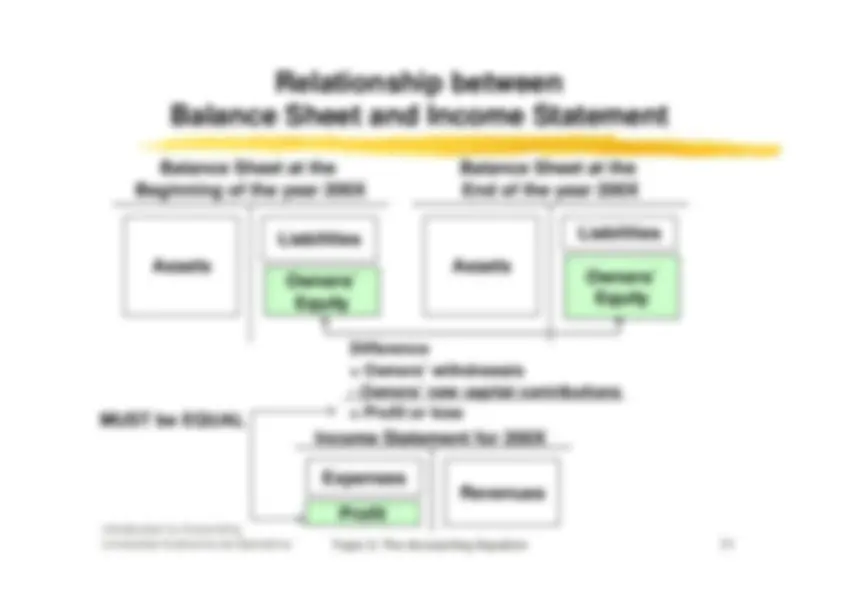

Relationship between

Balance Sheet and Income Statement

Time

Balance Sheet December 31,

Balance Sheet December 31,

Balance Sheet December 31,

Income Statement for Jan. – Dec. 2006

Income Statement for Jan. – Dec. 2007

Periodic Income

for 2006

Periodic Income

for 2007

Total Income