CHAPTER

2 :WEALTH AND

INCOME

Financial Accounting I

Academic year 2023/2024

Instructor Laura Arranz Aperte

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

An in-depth explanation of financial accounting concepts, focusing on wealth and income. It covers topics such as assets, liabilities, equity, income, balance sheet, income statement, and the classification of assets and liabilities. Examples and exercises to help students understand the concepts.

Tipo: Esquemas y mapas conceptuales

1 / 40

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

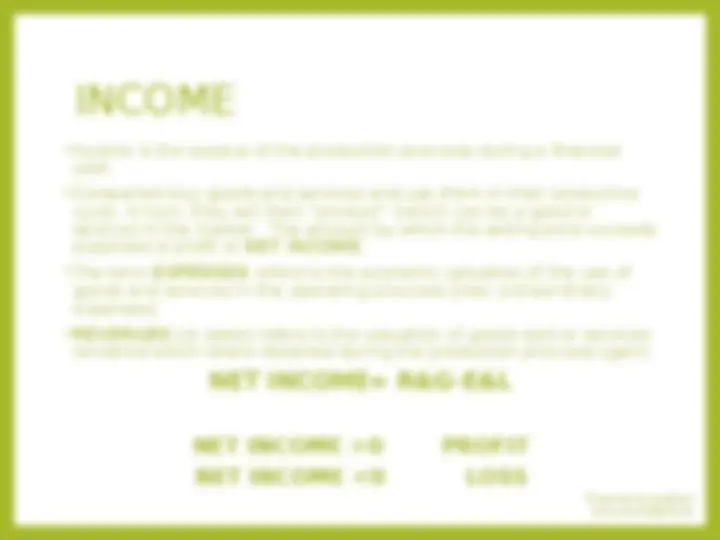

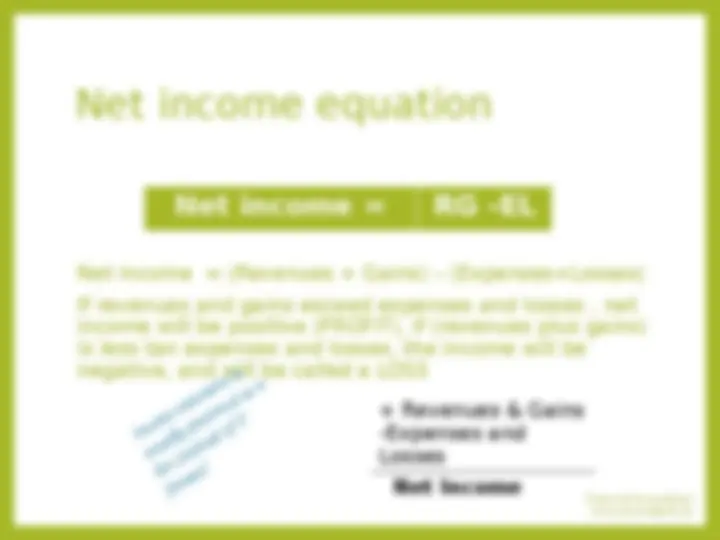

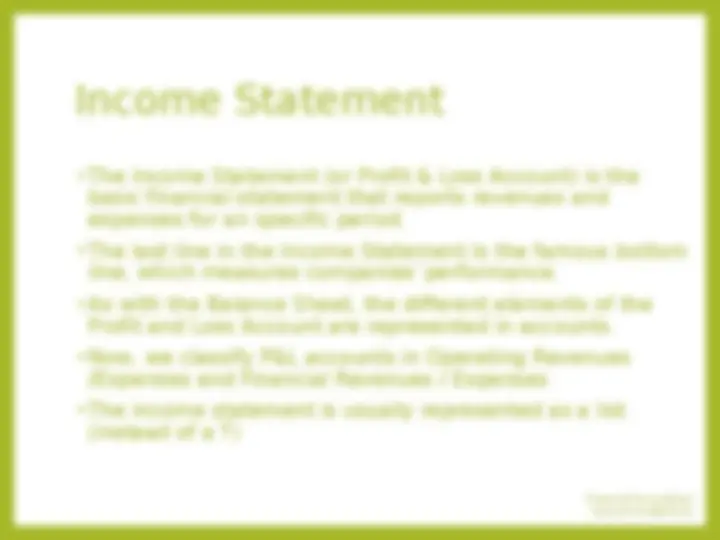

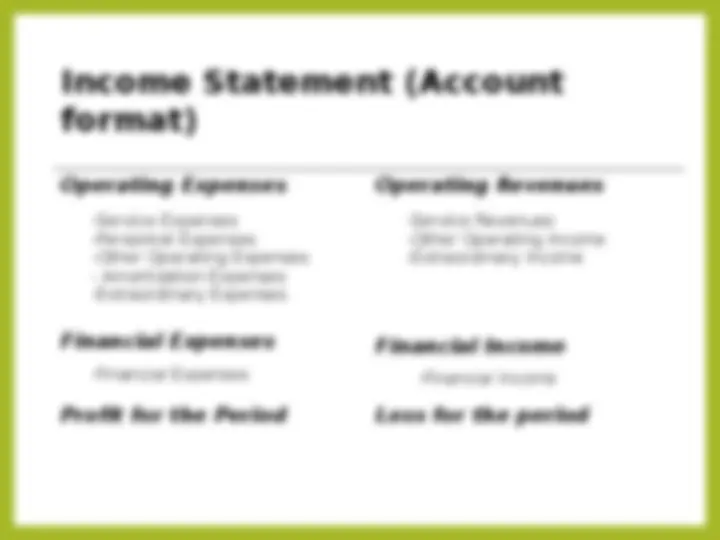

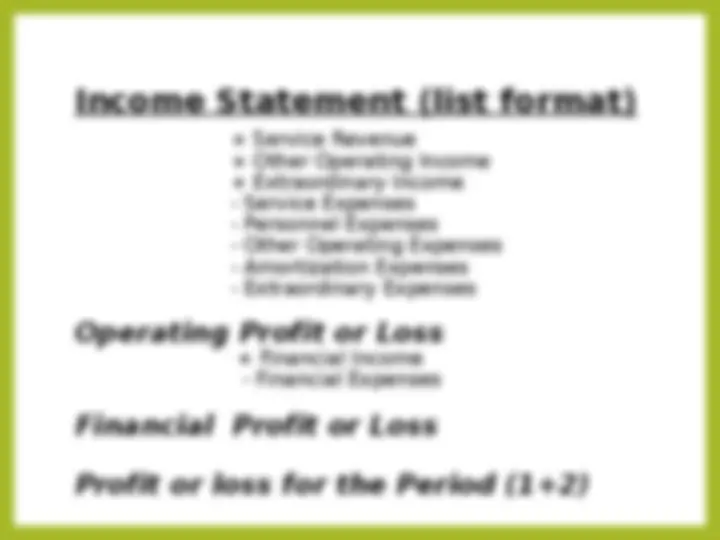

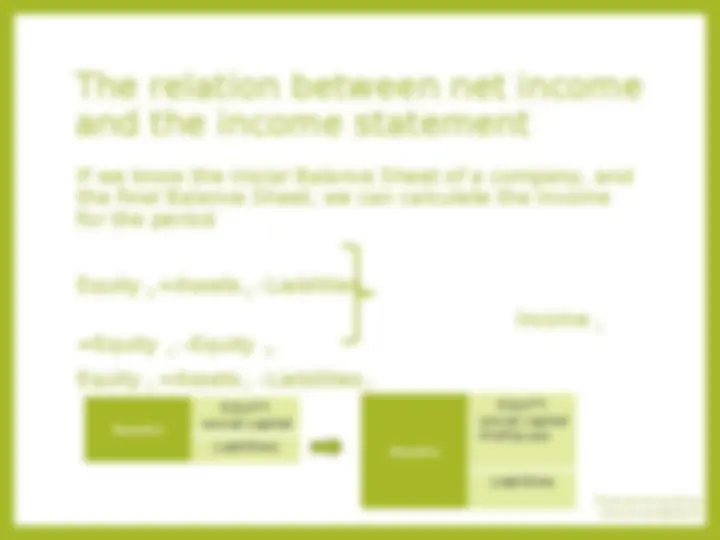

Wealth and Income Wealth (=Equity) = Assets – Liabilities

Balance Sheet Assets= Liabilities + Equity Income Statement Net Income = Revenues

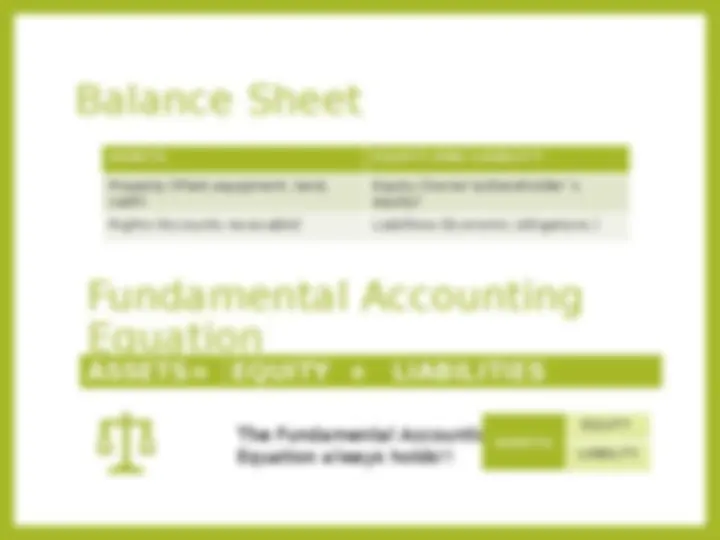

Balance Sheet

Fundamental Accounting Equation ASSETS= EQUITY + LIABILITIES The Fundamental Accounting Equation always holds!!

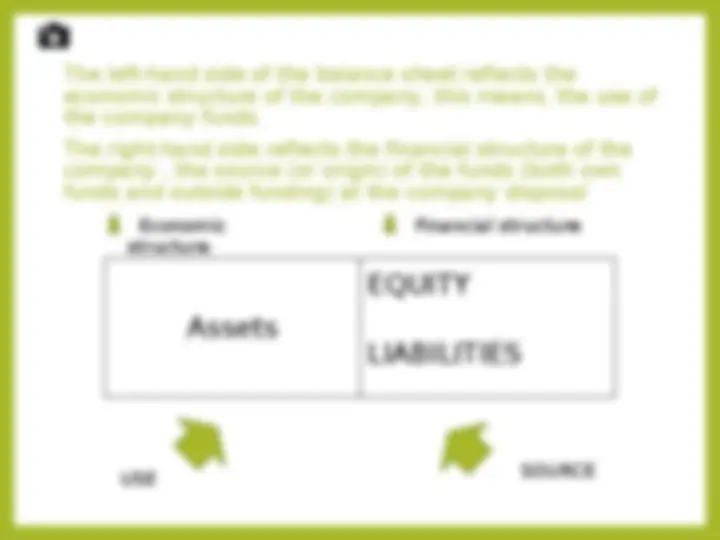

The left-hand side of the balance sheet reflects the economic structure of the company, this means, the use of the company funds. The right-hand side reflects the financial structure of the company , the source (or origin) of the funds (both own funds and outside funding) at the company disposal Assets EQUITY LIABILITIES Economic structure Financial structure USE SOURCE

The elements of the Balance Sheet and the Accounts

Current Assets + Non Current Assets =Total ASSETS

Financial Accounting I [email protected]

Moving to the left side of the BS we have two categories 1- LIABILITIES: Economic obligations and amounts owed to outsiders relating to loans, debts to suppliers etc, As with assets, liabilities can be classified into current and non current Total liabilities = current liab + non current liab Liabilities can also be classified into trade /financial liabilities 2- Shareholders equity (=wealth) Sh equity section is what the business is worth after all liabilities have been paid off Financial Accounting I [email protected]

Balance Sheet Accounts NON-CURRENT ASSETS Fixed Assets or long term assets This assets can be tangible/ intangible/ fixed investments -Accumulated Amortization (Depreciation) A representation of the use of the fixed assets along the years CURRENT ASSETS Short term trade debtors Trade receivables (accounts receivables) Short term financial debtors Current investment Cash EQUITY Capital Resources : Capital Profit/Loss NON-CURRENT LIABILITIES Long term creditors CURRENT LIABILITIES Short term trade creditors (accounts payable) Short term financial creditors Financial Accounting I [email protected]

Exercise 2 a company has the following elements at the beginning of a year:

Fixed-Assets 320,000 Capital resources Capital 180, B) CURRENT ASSETS 160,000 C) CURRENT LIABILITIES 300, Short-term trade debtors/receivables 100,000 Short-term trade creditors/payables 150, Cash 60,000 Short-term financial creditors/payables 150,

Example 2. On January 1st, Luis describes his financial situation. He has 400 euros in a current account in a bank, and a credit to a friend that amounts to 20 euros (the friend will return the money within two months). Luis owns a motorcycle that cost 3.000 €, of which 500 will be paid within 14 months Identify the following elements of the BS (1) Assets (2) Rights (3) Liabilities (4) Net equity (=net wealth)? (5) Balance Sheet? Assets= 3.400 € (= Bank account 400 + Motocycle 3.000) Total Legal rights (financial assets) = 20 € (=Loan to a friend) Liabilities = 500 (=Debt for the motorcycle) Total obligations = Net Equity = Assets –Liabilities = (3.400 +20)-500 = 2.920 € Financial Accounting I [email protected]

Balance Sheet Assets Equity & Liabilities Tangible Assets 3.400 Total Liabilities 500 Legal Rights 20 Net Equity 2. 0 Total Assets 3420 Total Equity and Liabilities

0 The balance sheet must always balance: Total Assets = Equity & Liabilities 3.420 = 500 + 2. Financial Accounting I [email protected]

Short-term trade debtors (ASSETS) are sometimes called “Accounts receivable” Short-term trade creditors (LIABILITIES) are called “Accounts payable” Financial Accounting I [email protected]

Example 3 The financial status of a sole proprietorship company is as follows:

Fixed-Assets 650,000 Capital resources Capital 584, B) CURRENT ASSETS 4,500 B) NON-CURRENT LIABILITIES - Cash 4,500 Long-term creditors/payables C) CURRENT LIABILITIES 70, Short-term trade creditors/payables 70,