CHAPTER 2:

Conceptual

Accounting

Framework

© Ediciones Pirámide

BEYOND FIGURES: Introduction to Financial Accounting

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO-

MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA,

A. (2012).

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Contabilidad Financiera, Profesor: maria del mar camacho, Carrera: Administración y Dirección de Empresas, Universidad: UCM

Tipo: Apuntes

1 / 40

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

BEYOND FIGURES: Introduction to Financial Accounting^ © Ediciones Pirámide

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO- MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA, A. (2012).

© Ediciones PirámideBEYOND FIGURES: Introduction to Financial Accounting

Have you ever played this game? Do you know this company? Do you think this company should launch into the Stock Market? What accounting standards do you think this company is using? What accounting standards should this company apply if it wants to quote in the Stock Market?

2.1. Accounting framework

2.2. The conceptual accounting framework: purpose and status

2.3. Accounting framework in Europe

2.4. Spanish accounting conceptual framework

2.5. Finnish accounting conceptual framework

BEYOND FIGURES: Introduction to Financial Accounting^ © Ediciones Pirámide

BEYOND FIGURES: Introduction to Financial Accounting^ © Ediciones Pirámide

© Ediciones Pirámide

OBJECTIVE

QUALITATIVECHARACTERISTICS

ENHANCEQUALITATIVE CHARACTERISTICS

CONSTRAINTS

ASSUMPTIONS

ELEMENTS

groups for their economic decision making^ Provide useful information to various user

Assets (^) Liabilities Equity Revenue Income- Expenses

Balance among qualitative characteristics^ Benefits versus^ costs

Accrual Accounting^ Concern^ Going

Understandability

representation^ Faithful^ Relevance

Verifiability Timeliness Comparability

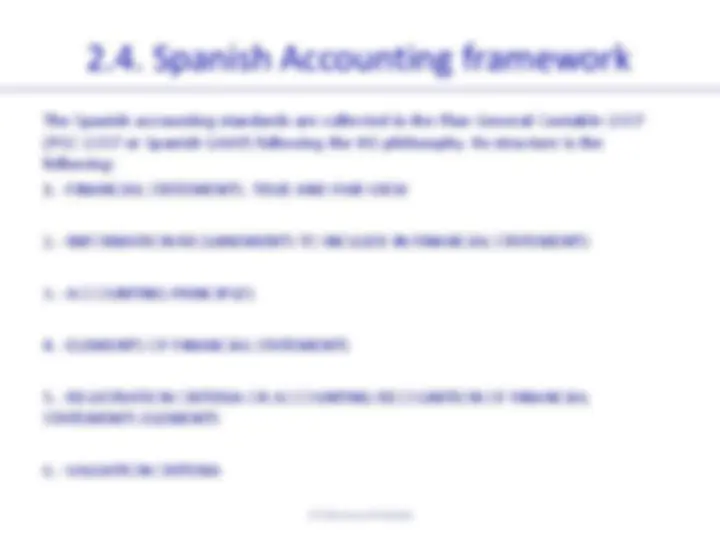

The Spanish accounting standards are collected in the Plan General Contable- (PGC-2007 or Spanish GAAP) following the IAS philosophy. Its structure is the following: 1.- FINANCIAL STATEMENTS. TRUE AND FAIR VIEW

2.- INFORMATION REQUIREMENTS TO INCLUDE IN FINANCIAL STATEMENTS

3.- ACCOUNTING PRINCIPLES

4.- ELEMENTS OF FINANCIAL STATEMENTS

5.- REGISTRATION CRITERIA OR ACCOUNTING RECOGNITION OF FINANCIAL STATEMENTS ELEMENTS

6.- VALUATION CRITERIA

© Ediciones Pirámide

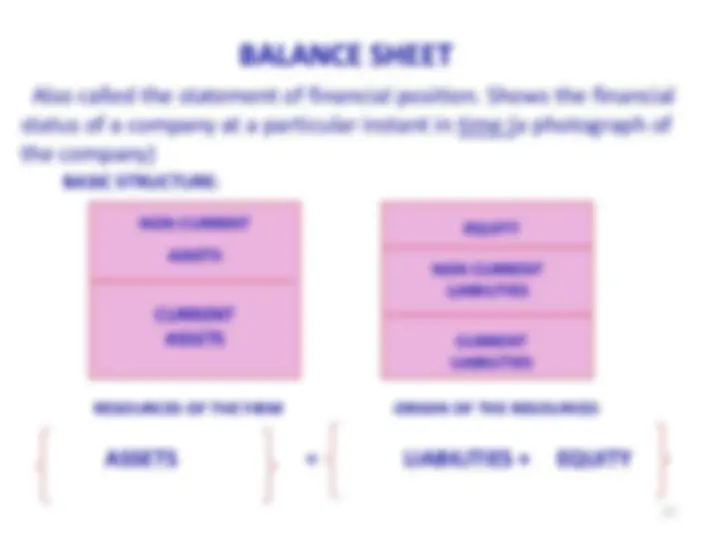

BALANCE SHEET

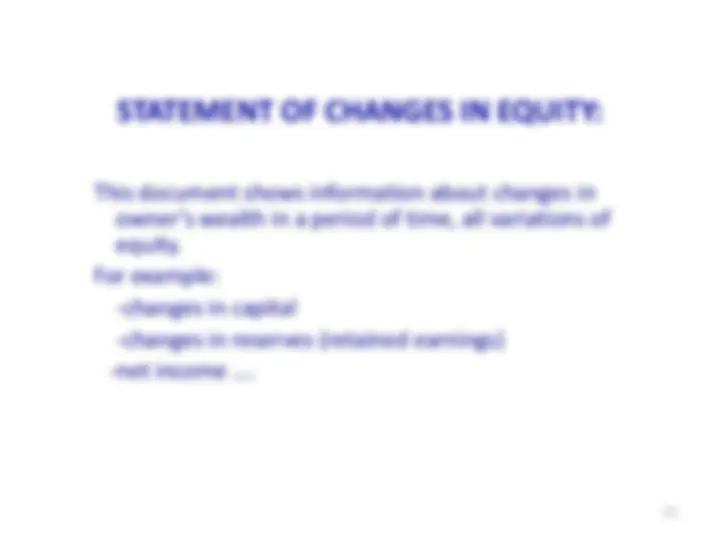

CHANGES IN EQUITY

INCOME STATEMENT

STATEMENT OF CASH FLOWS

EXPLANATORY NOTES

ASSETS LIABILITIES EQUITY REVENUES^ EXPENSES

Fuente: Rodriguez y otros (2005, 35)

FINANCIAL SITUATION INCOME

F

F

S

S

E L

10

PART 2. INFORMATION REQUIREMENTS FOR FINANCIAL STATEMENTS

RELEVANT: useful to make decisions. “ The Financial Statements should show all the RISKS the company is facing”

RELIABILITY: without mistakes and biases.

“… the company should include in its financial statements all the data that can determine a decision making, without omission or misstatement…”

COMPARABILITY: over time and between companies.

(look in www.iasb.org the IASB taxonomy for XBRL)

INTEGRITY, CONSISTENCY AND CLARITY: full information, consistency

11

EXAMPLE: When a company is under liquidation (to close down), then, it does not have to apply this requirement of going concern. It has to apply liquidation cost, not market price.

13

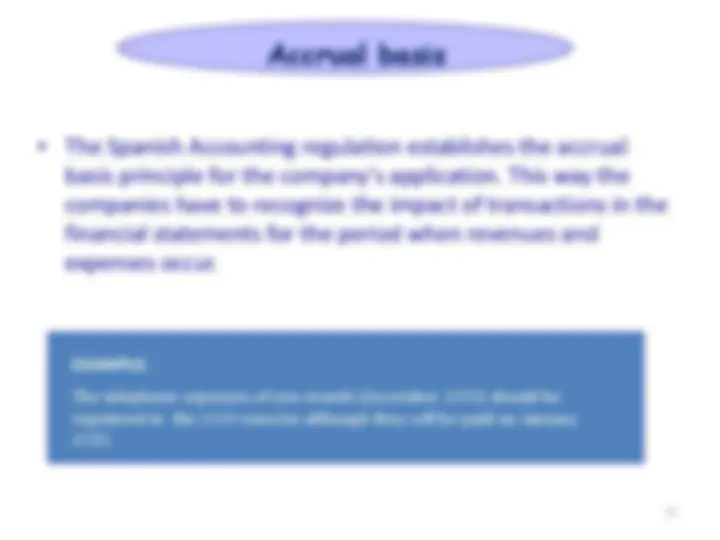

EXAMPLE: The telephone expenses of one month (December 2009) should be registered in the 2009 exercise although they will be paid on January

14

EXAMPLE: A company has a land that cost 100,000 €. a) If its market value is now 120,000 € it cannot register a profit until it has been obtained, that is until the company has sold the land. b) If its market value is 90,000 €, the company must register the likely loss.

16

EXAMPLE: In order not to omit information, if company “A” is entitled to collect invoices, and has liabilities towards company “B”, they must appear as separate elements in the Balance Sheet.

17

ASSETS: Goods, rights, economic resources LIABILITIES: Obligations to pay NET EQUITY: difference between assets and liabilities. Owners’ wealth

REVENUES: increases in Equity EXPENSES: decreases in Equity

WEALTH FINANCIAL Situation

WEALTH ECONOMIC Situation

‡ partner's stock

19

20