CHAPTER 4:

Book-keeping

© Ediciones Pirámide

BEYOND FIGURES: Introduction to Financial Accounting

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO-

MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA,

A. (2012).

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Contabilidad Financiera, Profesor: maria del mar camacho, Carrera: Administración y Dirección de Empresas, Universidad: UCM

Tipo: Apuntes

1 / 26

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO- MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA, A. (2012).

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

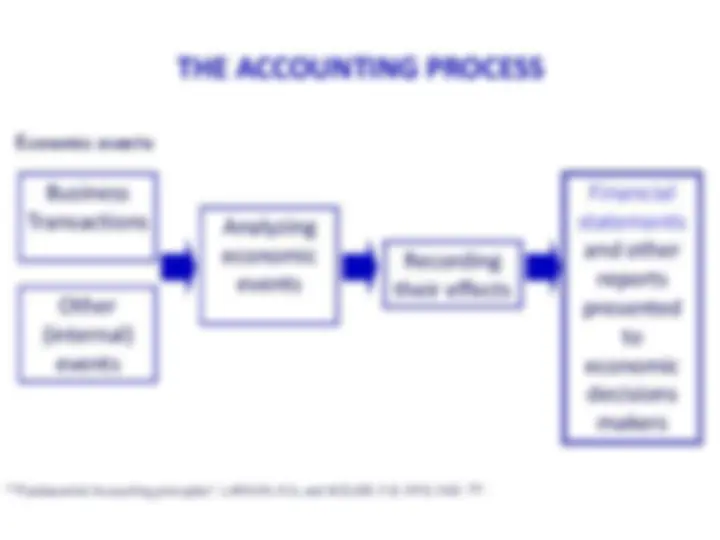

THE ACCOUNTING PROCESS

Economic events

*“Fundamental Accounting principles”, LARSON, K.D. and MILLER, P.B. 1993, PAG. 77.

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Example of JOURNAL

The form of GENERAL JOURNAL or JOURNAL :

There is no single standard form of Journal. Each entry has to be organized according to its date (chronologically).

TRADITIONAL FORM: Date (Oct. 1)

AMERICAN FORM:

Oct. 1 Wages 5, Cash 5,

5,000 Wages Cash 5,

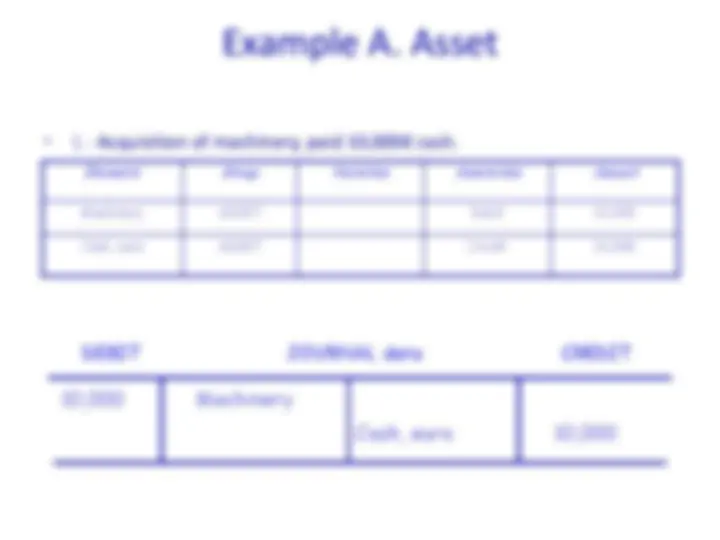

RULE: Each transaction generates two effects in the firm’s equity (double entry system book-keeping): an origin and a destination of resources that must record “at the same time” in the Journal and the Ledger of the firm.

There is another compulsory accounting book: INVENTORIES AND FINANCIAL STATEMENTS BOOKS with the initial balance sheet, Quarterly trial balance and the Financial Statements. © Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

4.2. How the accounts work

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

DEBIT Name of an account CREDIT

entry on the left side of entry on the right side of any account any account to CHARGE to CREDIT Balance debit or credit

4.2. How the accounts work

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

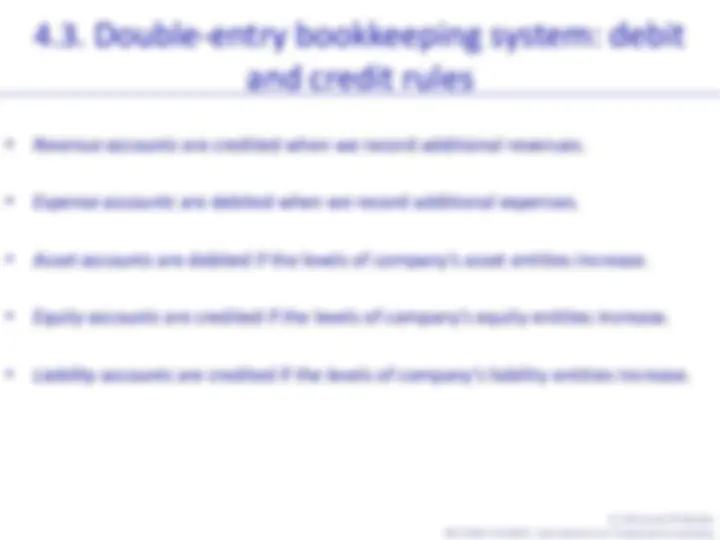

4.3. Double-entry bookkeeping system: debit

and credit rules

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Initial value Increases

Debit Account of Asset Credit

Decreases

AGREEMENT OF CREDIT AND DEBIT: accounts of EXPENSES and REVENUES

It starts and increases by DEBIT registries Unilateral working. These accounts can’t have entries at the right side of the accounts.

It starts and increases by CREDIT registries Unilateral working. These accounts can’t have entries at the left side of the accounts

When recording a transaction, in the Journal (to journalize) and Ledger (to post), we have to “imagine the answers” to 5 questions:

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

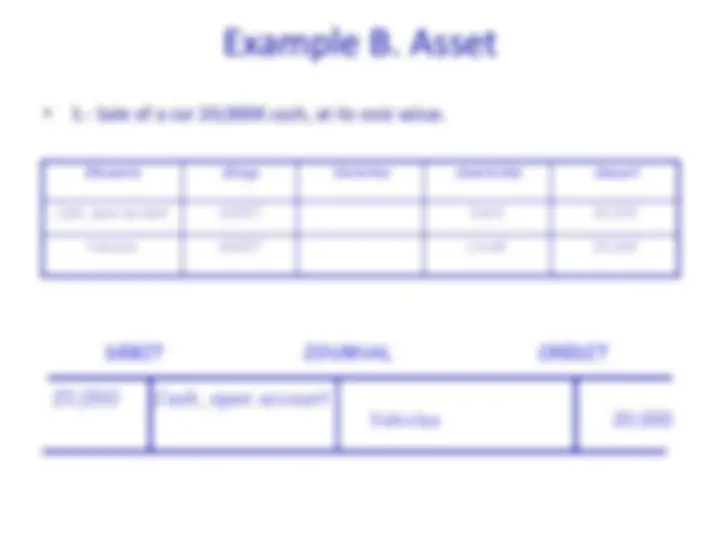

Example B. Asset

Elements Group Variation Annotation Amount

Cash, open account ASSET Debit 20, Vehicles ASSET Credit 20,

DEBIT JOURNAL CREDIT

20,000 Cash, open account Vehicles 20,

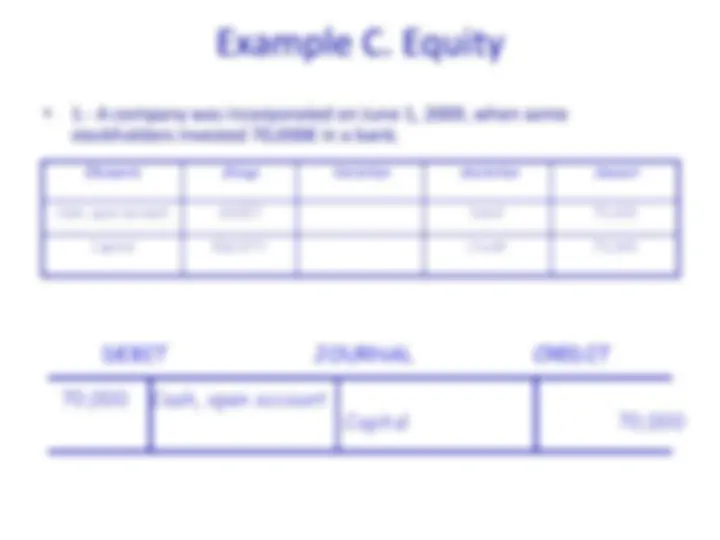

Example C. Equity

Cash, open account ASSET Debit 70, Capital EQUITY Credit 70,

DEBIT JOURNAL CREDIT

70,000 Cash, open account Capital 70,