CHAPTER 3:

Annual reports

© Ediciones Pirámide

BEYOND FIGURES: Introduction to Financial Accounting

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO-

MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA,

A. (2012).

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Contabilidad Financiera, Profesor: maria del mar camacho, Carrera: Administración y Dirección de Empresas, Universidad: UCM

Tipo: Apuntes

1 / 18

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

CAMACHO-MIÑANO, M.M.; AKPINAR, M.; RIVERO- MENÉNDEZ, M.J.; URQUIA.GRANDE, E. and ESKOLA, A. (2012).

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Telefonica Corporation, a company that operates mainly in telecommunications, media and contact center industries, disclosures every year the following documents belonging to its Annual reports:

Discussion point! After reading the Telefonica corporation statements you will be able to answer the following questions:

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

3.2. Financial Statements (II)

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Income statement/ Comprehensive income

ΣRevenues − ΣExpenses =

Revenues > Expenses = Profits Revenues < Expenses = Losses

Increases in Equity (^) Decreases in Equity

Balance sheet/ statement of financial position

Based on the basic accounting equation: Assets = Liability + Equity

Assets: Resources owned or controlled by a business. Liabilities: Claims against assets by creditors. Debts. Equities: Owners’ wealth; it is the difference between assets and liabilities.

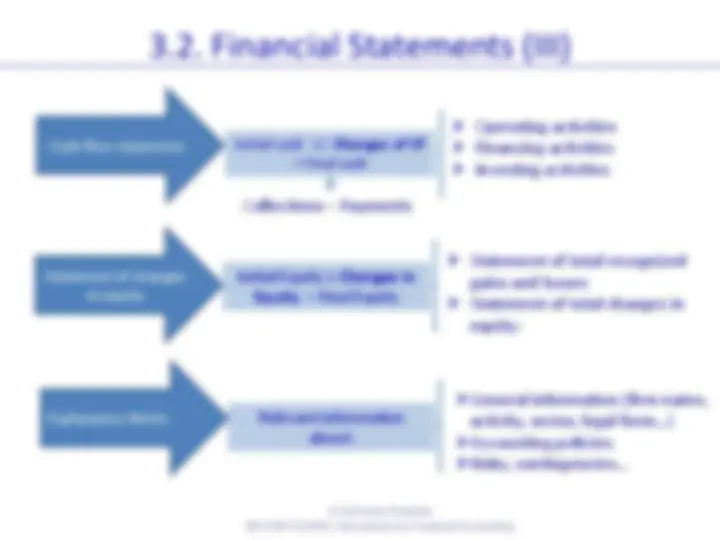

3.2. Financial Statements (III)

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Cash-flow statement Initial cash +/-^ Changes of CF = Final cash

Operating activities Financing activities Investing activities

Collections – Payments

Statement of changes in equity

Initial Equity ± Changes in Equity = Final Equity

Statement of total recognized gains and losses Statement of total changes in equity:

General information (firm name, activity, sector, legal form…) Accounting policies. Risks, contingencies…

Relevant information about:

Explanatory Notes

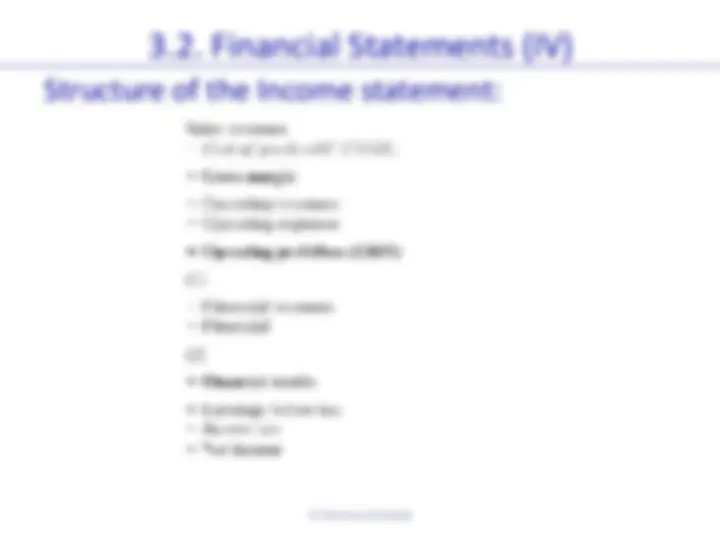

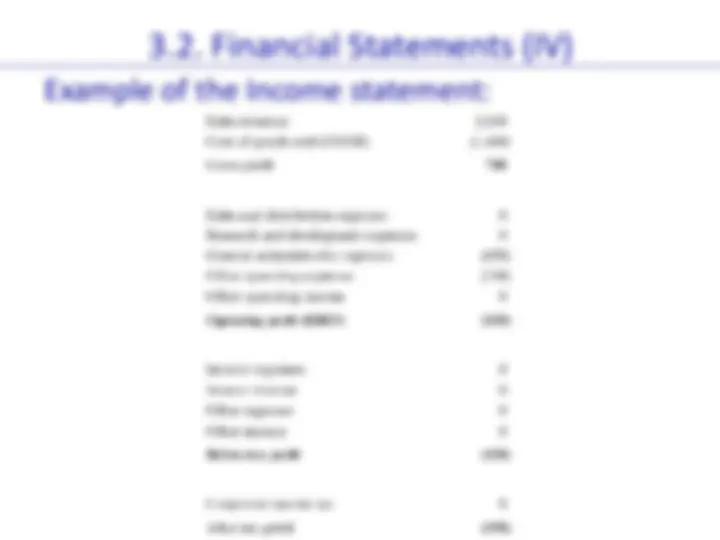

3.2. Financial Statements (IV)

Example of the Income statement:

© Ediciones Pirámide

3.2. Financial Statements (IV)

Structure of the Balance sheet:

© Ediciones Pirámide

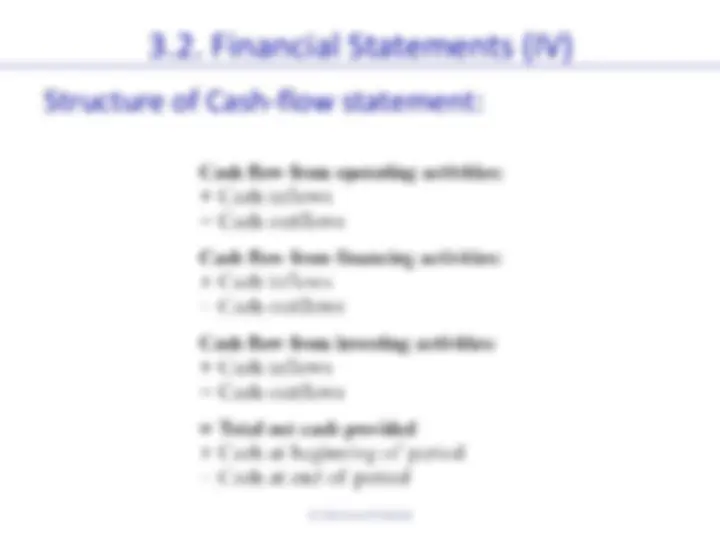

3.2. Financial Statements (IV)

Structure of Cash-flow statement:

© Ediciones Pirámide

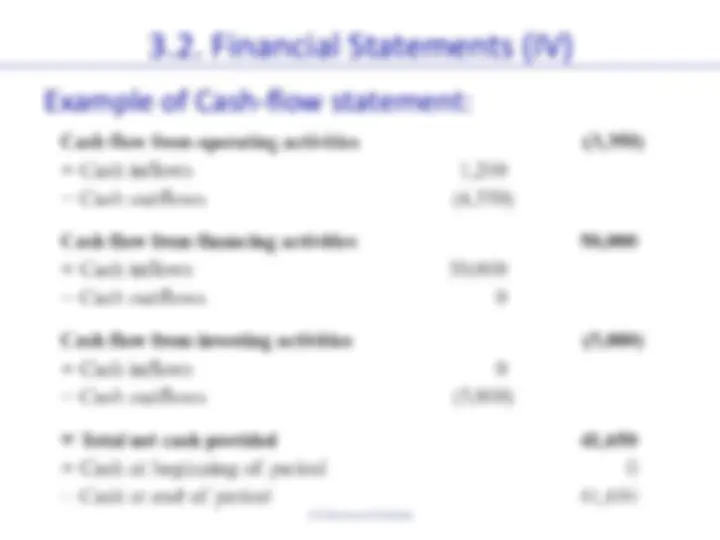

3.2. Financial Statements (IV)

Example of Cash-flow statement:

© Ediciones Pirámide

3.3. Other reports (I)

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

Auditing reports

Review of the financial statements of a firm. Kinds of opinions: unqualified, qualified, adverse and disclaimer report.

Management report

Management’s view about what happened in the past and also what management believes it is going to happen in the entity’s future, so it is quiet subjective.

Explain of the company’s policies, principles and actions that could have environmental impacts. Describes the investments made by the company to improve the social conditions of their employees.

Corporate social responsability report

Corporate governance report

Describes its process and policies to manage and organize its performance.

© Ediciones Pirámide BEYOND FIGURES: Introduction to Financial Accounting

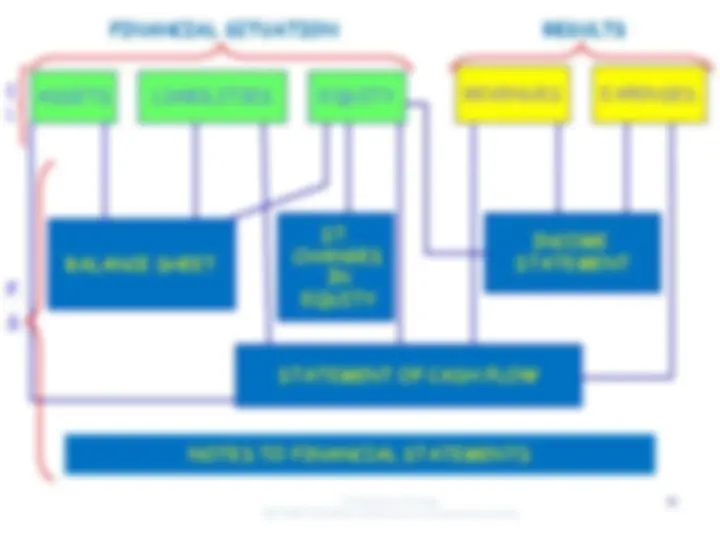

Annual report is an annual publication that: summarizes the corporation’s past performance and its future expectation during an accounting period. comprises the financial statements and also other documents such as: report from the chairman, audit report, management report, corporate responsibility report and corporate governance report. The financial statements include: balance sheet, income statement, cash flow statement, statement of changes in equity and explanatory notes. Balance sheet represents the firm’s wealth in a concrete moment. It is divided into current assets, non-current assets, owners’ equity, non-current liabilities and current liabilities. The income statement represents the firm’s wealth produced in a period of time. There are revenues and expenses. Cash-flow statement disclosure the changes made in cash during a period of time. Statement of changes in equity informs about changes produced in owner’s wealth during an accounting period. The explanatory notes disclosure the basis of preparation of financial statement, significant accounting policies and additional information to better understand the other financial statement documents.