Télécharge Formules importantes - finance et plus Notes au format PDF de Finance sur Docsity uniquement!

FICHE - Financial Analysis and Management The Balance Sheet: ASSETS EQUITY AND LIABILTIES NON-CURRENT ASSETS Intangible assets Tangible assets Financial assets CURRENT ASSETS Inventories Receivables Marketable securities Cash

EQUITY

Capital Retained earnings Net income LIABILITIES Provisions Long term borrowing Trade payable Tax and social payable Sales revenue +stored = Total production -cost of row material used -other supplies & external expenses = Value added -salaries and charges (personal benefit expenses) -taxes other than income tax =EBITDA -depreciation & amortization +/- other income & expenses =EBIT +/- financial income +/-financial expenses =EBT -income taxe =NET INCOME Formules

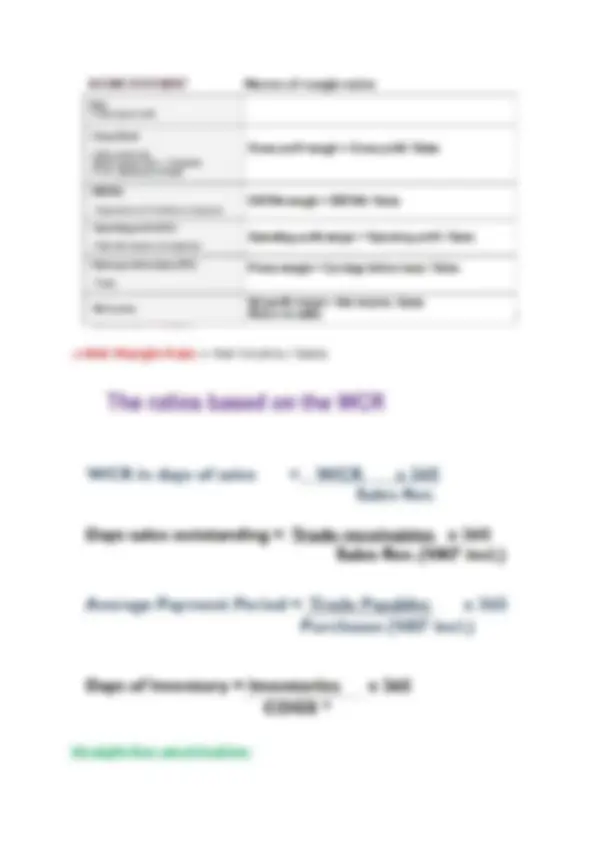

->Working Capital Requirement = Current assets save Cash - Current Liabilities WCR = Inventories + trade Receivables + other Receivables - Accounts payables - Tax and social payables - Other payables. ->(Net) Working Capital (N)WC = Current Assets - Currents Liabilities ->Working capital (WC) = long terme Ressources (Total equity+Financial and bank debts) - Non current assets ->Net Cash Position = (N)WC – WCR ->Market Value of Equity Ratio = Market Capitalization / Total Equity ->Market Value of Equity Ratio = Market value of Equity + (Net) Debt ->Market Capitalization = Share Price * Number of Outstanding Shares ->Total Equity = Book Value of Equity + Market Value of Debt - Financial Debt ->Debt to Equity Ratio = Total Debt / Total Equity ->Price to earning ratio = Market Price per Share ÷ Earnings per Share (EPS) ->Price to book ratio = Market Price per Share / Book Value per Share ->Economic Assets = Total Assets - Non-Economic Assets ->Net debt = Total debt /financial debt - Cash and Market securities ->Financial leverage = (Financial) debt / Equity The liquidity ratios: ->Current Ratio = Current Assets / Current Liabilities (Inventories + Account receivables + Other receivables + Cash and cash equivalents) / (Account Payables + Other liabilities + overdrafts ) ->Quick Ratio = Current Assets (less inventories) / Current Liabilities ->Cash Ratio = ( Cash + Marketable Securities ) / Current Liabilities ->Interest Coverage Ratio (ou DSCR) = EBIT / Interest Expenses ->Debt Ratio = Financial Debt / (Equity + Financial Debt) Attention à ne pas confondre avec la formule du Leverage (Voir cours mid-term page 1)

->Net Margin Rate = Net Income / Sales Straight-line amortization:

- ->The bank grants a loan of 10.000 € to INTER repayable over 5 years at

- Debt interests: 10000 x 0,05 =

- The total annuity for the 1st year = 2000 + 500 =

- The interests of the next year are: 8000 x 0,05 =

- The total annuity is then 2000 + 400 =

- ->The bank grants a loan of 10.000 € to INTER repayable over 5 years at Constant annuities:

- The annuity is the same every year = %.

- Interests 1st year = 10000 x 0,05 =

- Amortization 1st year = 2310 – 500 =

- The next year: Remaining debt =

- Interests = 8190 x 0,05 =409,

- Amortization = 2310 – 409,5 = 1900,

The cash position (treso) is higher if = The increase in the working capital is higher than the increase in the working capital requirement -> L’augmentation du fonds de roulement est supérieure à l’augmentation du besoin en fonds de roulement. From the following data related to a given manufacturing company, you should compute the EBITDA : -Sales revenue = 2000 -Purchases of raw materials = 550 -Change in raw materials inventories (Beginning invent. – ending invent.) = 200 -Wages and social charges = 800 -Production taxes = 250 (-depreciation and provision = 1100 -Financial expenses = 550.) =2000-550-200-800-250=200€ The working capital generally represents: = Surplus of long-term resources over the firm’s non-current assets -> Formule pour le working capital (Excédent de ressources à long terme sur (-) les actifs non courants de l’entreprise) If the EBIT of a given company has decreased by 2% in N, this may result from an increase in its depreciation due to significant investments achieved at the beginning of the year = Vrai Traduction :

Asset / Actif Bond / Obligation Current asset / Actif circulant (< 1 an) Cyclical asset / Actif cyclique Equity / Capitaux propres Functional balance-sheet / Bilan fonctionnel leased tangible assets / immobilisation corporelle en location Liability / Passif Liquidity / Liquidité Maturity / Echéance Net cash / Trésorerie nette Net working capital / Besoin en fond de roulement (BFR) Overdraft / Découvert bancaire Share capital / Capital social Short (long) -term loans / Prêts à CT (LT) Short (long) -term debt / Emprunt ou dette à (LT) CT Tax receivable / Créance fiscale Trade payable / Dette d'exploitation Trade receivable / Créance commerciale Payment period / Délai de paiement Property principle / Principe de propriété Retained profit / Réserve Securitization / titrisation Solvency / Solvabilité Working capital / Fond de roulement