THE$OBJECTIVE$IN$CORPORATE$

FINANCE$

“If$you$don’t$know$where$you$are$going,$it$does’nt$

maCer$how$you$get$there”$

2!

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Students of Communication, study E-Commerce as an auxiliary subject. these are the key points discussed in these Lecture Slides of E-Commerce : Decision Criteria, Contemporary Financial, Management, Real Options, Capital Budgeting, Net Present Value, Profitability Index, Internal Rate, Payback Period, Budgeting Criteria

Typology: Slides

1 / 11

This page cannot be seen from the preview

Don't miss anything!

2

3

5

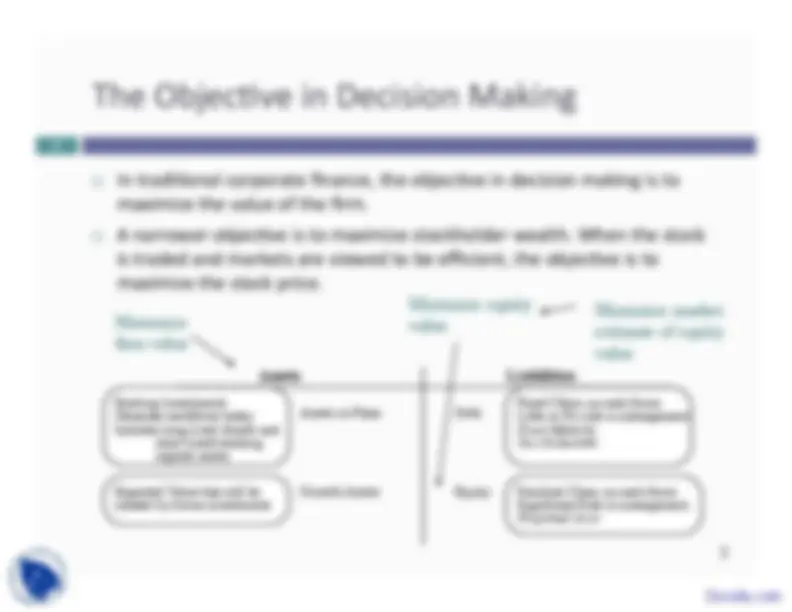

Assets Liabilities

Assets in Place Debt

Equity

Fixed Claim on cash flows Little or No role in management Fixed Maturity Tax Deductible

Residual Claim on cash flows Significant Role in management Perpetual Lives

Growth Assets

Existing Investments Generate cashflows today Includes long lived (fixed) and short-lived(working capital) assets

Expected Value that will be created by future investments

Maximizing Stock Prices is too “narrow” an

objecKve: A preliminary response

6

¨ Maximizing stock price is not incompaKble with

meeKng employee needs/objecKves. In parKcular:

¤ -‐ Employees are o\en stockholders in many firms

¤ -‐ Firms that maximize stock price generally are profitable firms that can afford to treat employees well.

¨ Maximizing stock price does not mean that

customers are not criKcal to success. In most

businesses, keeping customers happy is the route to

stock price maximizaKon.

¨ Maximizing stock price does not imply that a

company has to be a social outlaw.

8

STOCKHOLDERS

Maximize stockholder wealth

Hire & fire managers

Lend Money

Protect bondholder Interests

Reveal information honestly and on time

Markets are efficient and assess effect on value

No Social Costs

All costs can be traced to firm

9

STOCKHOLDERS

Managers put their interests above stockholders

Have little control over managers

Lend Money

Bondholders can get ripped off

Delay bad news or provide misleading information

Markets make mistakes and can over react

Significant Social Costs

Some costs cannot be traced to firm

The Annual MeeKng as a disciplinary venue

11

¨ The power of stockholders to act at annual meeKngs is diluted by three factors ¤ Most small stockholders do not go to meeKngs because the cost of going to the meeKng exceeds the value of their holdings. ¤ Incumbent management starts off with a clear advantage when it comes to the exercise of proxies. Proxies that are not voted becomes votes for incumbent management. ¤ For large stockholders, the path of least resistance, when confronted by managers that they do not like, is to vote with their feet.

¨ Annual meeKngs are also Kghtly scripted and controlled events, making it difficult for outsiders and rebels to bring up issues that are not to the management’s liking.

And insKtuKonal investors go along with

incumbent managers…

12