Lesson 03

Cash Flow & Equity

Statement

Financial Statements

Analysis

2017/18

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Financial Statement Analysis, Profesor: , Carrera: Administració i Direcció d'Empreses - Anglès, Universidad: UAB

Tipo: Apuntes

1 / 14

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

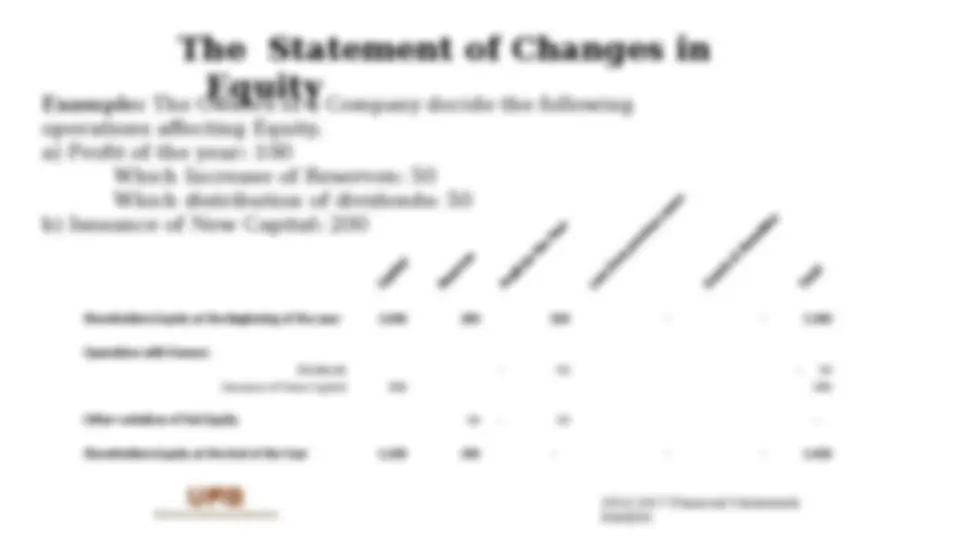

2016-2017 Financial Statements Analysis Equity, is what the company “owes” to its owners. (^) The role of the statement of changes in equity is to provide a reconciliation of opening and closing equity in a specific period. (^) It provides details of the various equity accounts that are impacted by the period’s total income. (^) It also provides information about the effects of transactions with owners (distributions and capital contributions).

Shareholders Equity at the Beginning of the year 1.000 200 100 - - 1. Operations with Owners Dividends - 50 - 50 Issuance of New Capital 200 200 Other variations of Net Equity 50 - 50 - Shareholders Equity at the End of the Year 1.200 250 - - - 1. Example: The Owners of a Company decide the following operations affecting Equity. a) Profit of the year: 100 Which Increase of Reserves: 50 Which distribution of dividends: 50 b) Issuance of New Capital: 200

2016-2017 Financial Statements Analysis

2016-2017 Financial Statements Analysis

2016-2017 Financial Statements Analysis

Capital Share Premium Retained Earnings Profi t for the year Grants & Donations Other Variations in Net Equity Total Equity Shareholders Equity 01.01.201 5^1 .000^1. Profit for the Year * 1 0.000 € Operations with Owners Dividends -2.000 € New Capital Other Variation of Net Equity 8.000 € -8.000 € 1 0.000 € Shareholders Equity 31.12.201 5 1 .000 - 8.000 - 1 0.000 - 1 9. Profit for the Year * 20.000 € Operations with Owners Dividends -4.000 € New Capital 5.000 € 1 0.000 € Other Variation of Net Equity 1 6.000 € -16.000 € Shareholders Equity 31.12.201 6 6.000^1 0.000^ 24.000^ -^1 0.000^ -^ 50.

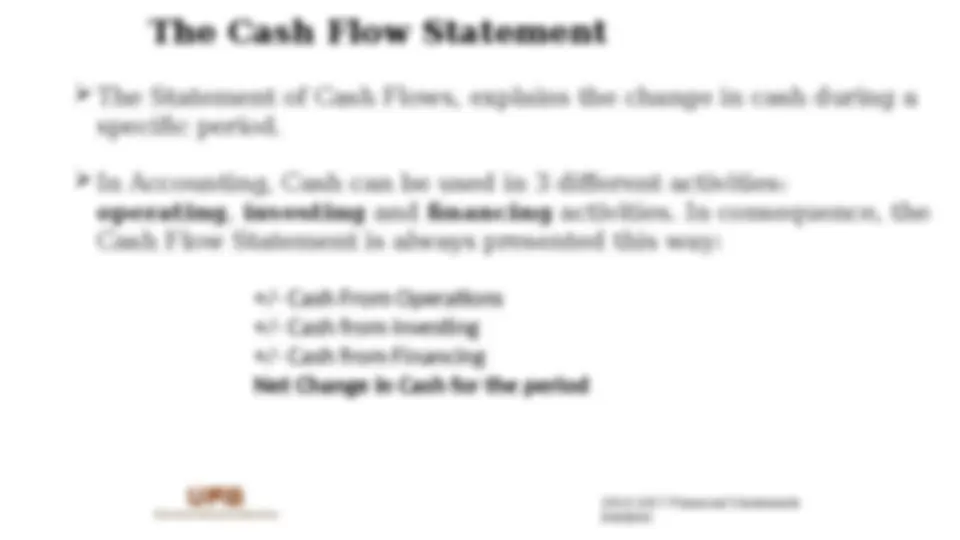

(^) A potentially and promising profitable business can fail due to a temporary cash problem. (^) Cash Planning and Cash Management are vital to the success and survival of every business. (^) Cash ≠ Profit. The Income Statement shows how much profit has been earned, but this does not necessarily mean that the organization will have cash. (^) The Cash Flow Statements gives information about the Cash inflows and the Cash outflows of a company, and the business phase where it stands.

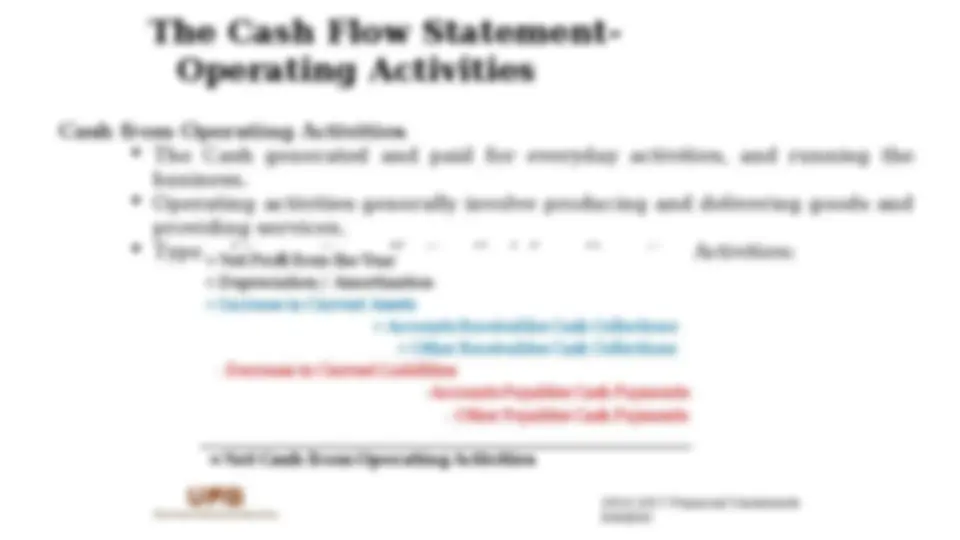

Cash from Operating Activities (^) The Cash generated and paid for everyday activities, and running the business. (^) Operating activities generally involve producing and delivering goods and providing services. (^) Types of transactions affecting Cash from Operating Activities:

2016-2017 Financial Statements Analysis

Cash from Investing Activities (^) The Cash involved in acquiring assets which will generate profits and cash flows in the future. (^) Purchase and Sale of Non-Current Assets, such as: Property, Plant, Equipment, Long-term Investments. (^) Types of transactions affecting Cash from Investing Activities:

2016-2017 Financial Statements Analysis

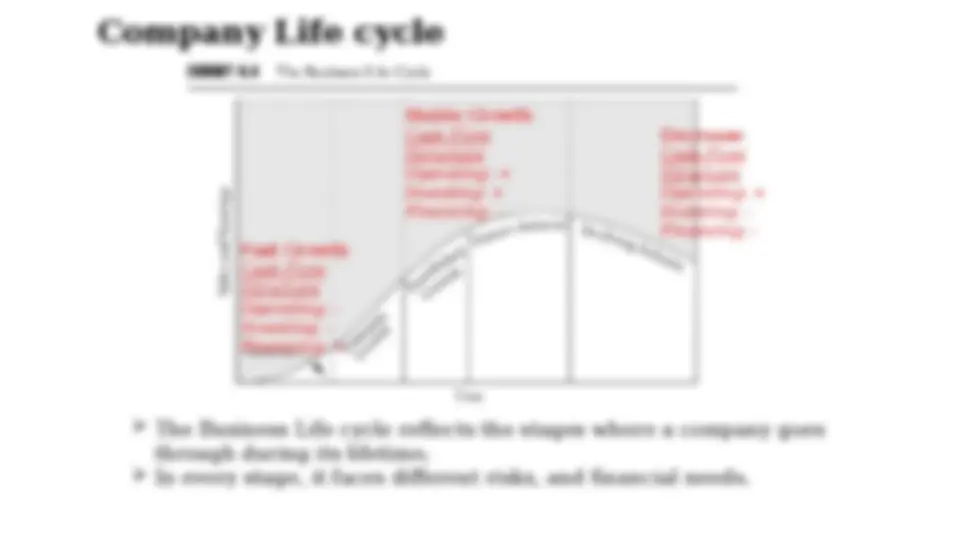

(^) The Business Life cycle reflects the stages where a company goes through during its lifetime. (^) In every stage, it faces different risks, and financial needs. Fast Growth Cash Flow Structure Operating: - Investing: - Financing: + Stable Growth Cash Flow Structure Operating: + Investing: + Financing: - Decrease Cash Flow Structure Operating: + Investing: - Financing: -

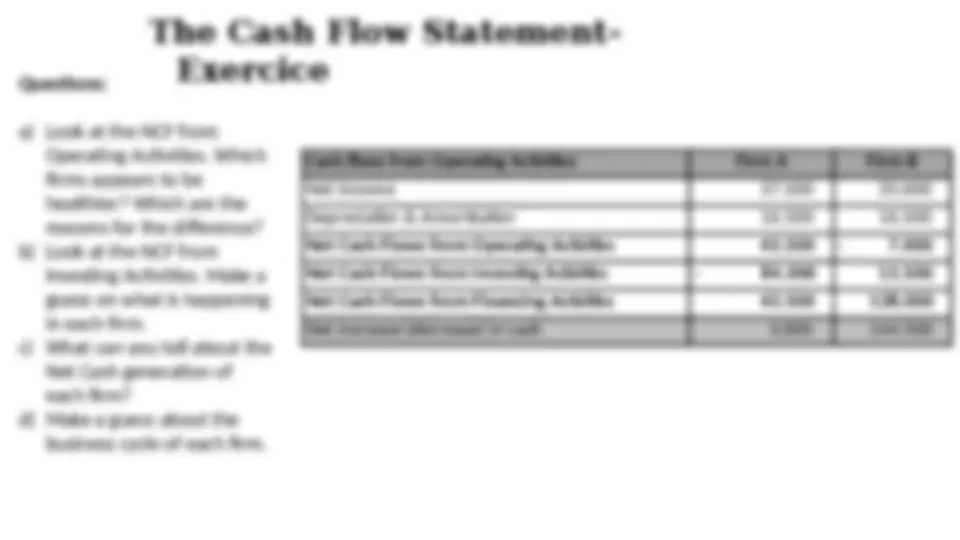

Cash flows from Operating Activities: Firm A Firm B Net Income 37.500 35. Depreciation & Amortization 16.500 16. Net Cash Flows from Operating Activities 43.500 - 7. Net Cash Flows from Investing Activities - 84.000 13. Net Cash Flows from Financing Activities 43.500 138. Net increase (decrease) in cash 3.000 144. Questions: a) Look at the NCF from Operating Activities. Which firms appears to be healthier? Which are the reasons for the difference? b) Look at the NCF from Investing Activities. Make a guess on what is happening in each firm. c) What can you tell about the Net Cash generation of each firm? d) Make a guess about the business cycle of each firm.