¡Descarga Profit maximization (chapter 4) y más Apuntes en PDF de Microeconomía solo en Docsity!

1 Perfectly Competitive Markets 2 Profit maximization 3 Marginal Revenue, Marginal Cost, and Profit Maximization 4 Choosing Output in the Short Run 5 The Competitive Firm’s Short-Run Supply Curve 6 The Short-Run Market Supply Curve 7 Choosing Output in the Long-Run 8 The Industry’s Long-Run Supply Curve

C H A P T E R 4

Profit Maximization

and Competitive Supply

CHAPTER OUTLINE

1

PRICE TAKING

Because each individual firm sells a sufficiently small proportion of total

market output, its decisions have no impact on market price.

● price taker Firm that has no influence over market price and thus takes the

price as given.

PRODUCT HOMOGENEITY

When the products of all of the firms in a market are perfectly substitutable with

one another—that is, when they arehomogeneous—no firm can raise the price

of its product above the price of other firms without losing most or all of its business.

In contrast, when products are heterogeneous, each firm has the opportunity to raise its price above that of its competitors without losing all of its sales.

The assumption of product homogeneity is important because it ensures that

there is a single market price, consistent with supply-demand analysis.

2

Do Firms Maximize Profit?

The assumption of profit maximization is frequently used in

microeconomics because it predicts business behavior reasonably

accurately and avoids unnecessary analytical complications.

For smaller firms managed by their owners, profit is likely to dominate

almost all decisions. In larger firms, however, managers who make day-

to-day decisions usually have little contact with the owners.

Firms that do not come close to maximizing profit are not likely to

survive. The firms that do survive make long-run profit maximization

one of their highest priorities.

3

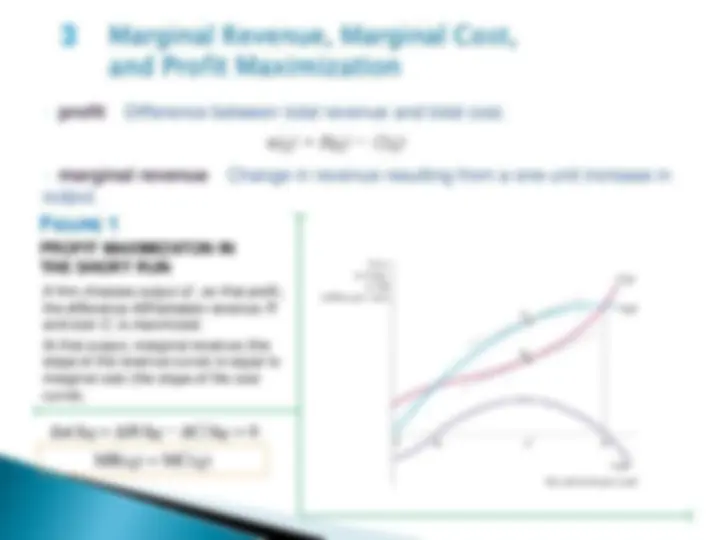

● profit Difference between total revenue and total cost.

π(q) = R(q) − C(q)

● marginal revenue Change in revenue resulting from a one-unit increase in

output.

A firm chooses output q *, so that profit, the difference AB between revenue R and cost C , is maximized. At that output, marginal revenue (the slope of the revenue curve) is equal to marginal cost (the slope of the cost curve).

Δπ/Δ q = Δ R /Δ q − ΔC/Δ q = 0

MR( q ) = MC( q )

PROFIT MAXIMIZATON IN

THE SHORT RUN

FIGURE 1

The demand curved facing an individual firm in a competitive market is

both its average revenue curve and its marginal revenue curve. Along this demand curve, marginal revenue, average revenue, and price are all equal.

Profit Maximization by a Competitive Firm

MC( q) = MR = P

Because each firm in a competitive industry sells only a small fraction

of the entire industry output,how much output the firm decides to sell

will have no effect on the market price of the product.

Because it is a price taker, the demand curve d facing an individual competitive

firm is given by a horizontal line.

A perfectly competitive firm should choose its output so that marginal

cost equals price:

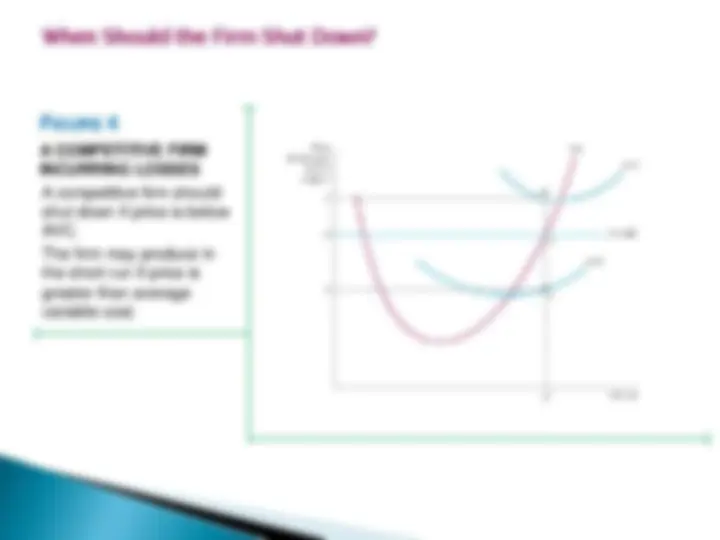

When Should the Firm Shut Down?

A COMPETITIVE FIRM

INCURRING LOSSES

FIGURE 4

A competitive firm should shut down if price is below AVC. The firm may produce in the short run if price is greater than average variable cost.

6

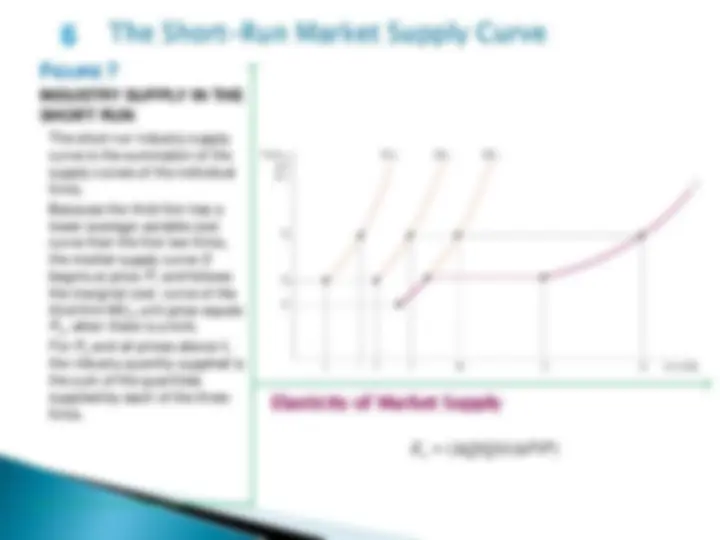

INDUSTRY SUPPLY IN THE

SHORT RUN

FIGURE 7

The short-run industry supply curve is the summation of the supply curves of the individual firms. Because the third firm has a lower average variable cost curve than the first two firms, the market supply curve S begins at price P 1 and follows the marginal cost curve of the third firm MC 3 until price equals P 2 , when there is a kink. For P 2 and all prices above it, the industry quantity supplied is the sum of the quantities supplied by each of the three firms.

Elasticity of Market Supply

E s = (Δ Q / Q )/(Δ P / P )

PRODUCER SURPLUS VERSUS PROFIT

PRODUCER SURPLUS FOR

A MARKET

FIGURE 9

Producer surplus = PS = R − VC

Profit = π = R − VC − FC

The producer surplus for a market is the area below the market price and above the market supply curve, between 0 and output Q*.

● long-run competitive equilibrium All firms in an industry are

maximizing profit, no firm has an incentive to enter or exit, and price is

such that quantity supplied equals quantity demanded.

When a firm earns zero economic profit, it has no incentive to exit the

industry.

Likewise, other firms have no special incentive to enter.

A long-run competitive equilibrium occurs when three conditions hold:

1. All firms in the industry are maximizing profit.

2. No firm has an incentive either to enter or exit the industry

because all firms are earning zero economic profit.

3. The price of the product is such that the quantity supplied by the

industry is equal to the quantity demanded by consumers.

LONG-RUN COMPETITIVE

EQUILIBRIUM

FIGURE 11

Initially the long-run equilibrium price of a product is $40 per unit, shown in (b) as the intersection of demand curve D and supply curve S 1. In (a) we see that firms earn positive profits because long-run average cost reaches a minimum of $30 (at q 2 ). Positive profit encourages entry of new firms and causes a shift to the right in the supply curve to S 2 , as shown in (b). The long-run equilibrium occurs at a price of $30, as shown in (a) , where each firm earns zero profit and there is no incentive to enter or exit the industry.

8 The Industry’s^ Long-Run Supply^ Curve

Constant-Cost Industry

● constant-cost industry Industry whose long-run supply curve is horizontal.

In (b) , the long-run supply curve in a constant-cost industry is a horizontal line SL. When demand increases, initially causing a price rise, the firm initially increases its output from q 1 to q 2 , as shown in (a). But the entry of new firms causes a shift to the right in industry supply. Because input prices are unaffected by the increased output of the industry, entry occurs until the original price is obtained (at

point B in (b) ).^ The long-run supply curve for a constant-cost

industry is, therefore, a horizontal line at a price

that is equal to the long-run minimum average

cost of production.

LONG-RUN SUPPLY IN A

CONSTANT COST INDUSTRY

FIGURE 13

8 The Industry’s^ Long-Run Supply^ Curve

Increasing-Cost Industry

● increasing-cost industry Industry whose long-run supply curve is upward sloping.

LONG-RUN SUPPLY IN AN

INCREASING COST INDUSTRY

FIGURE 14

In (b) , the long-run supply curve in an increasing-cost industry is an upward-sloping curve SL. When demand increases, initially causing a price rise, the firms increase their output from q 1 to q 2 in (a). In that case, the entry of new firms causes a shift to the right in supply from S 1 to S 2. Because input prices increase as a result, the new long-run equilibrium occurs at a higher price than the initial equilibrium.^ In an increasing-cost industry, the long-run industry supply curve is upward sloping.

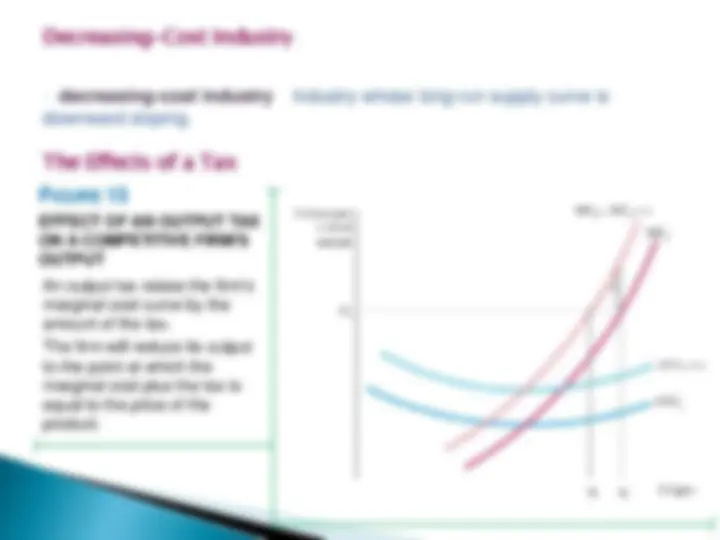

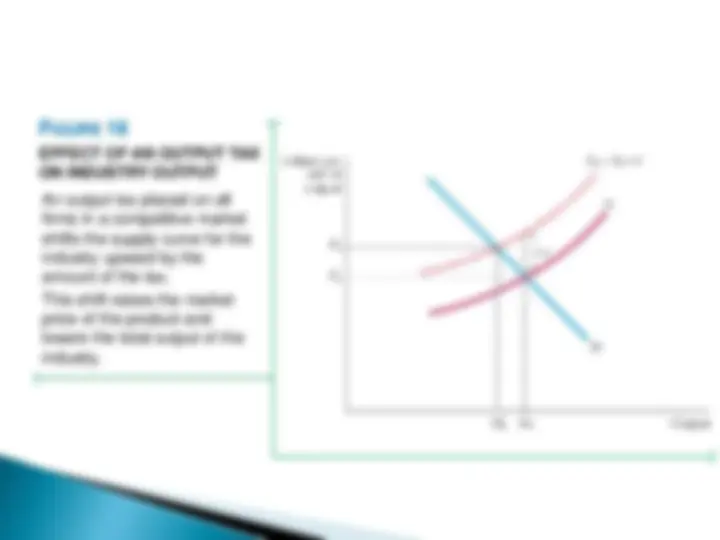

EFFECT OF AN OUTPUT TAX

ON INDUSTRY OUTPUT

FIGURE 16

An output tax placed on all firms in a competitive market shifts the supply curve for the industry upward by the amount of the tax. This shift raises the market price of the product and lowers the total output of the industry.

Long-Run Elasticity of Supply

The long-run elasticity of industry supply is defined in the same way as

the short-run elasticity: It is the percentage change in output (∆ Q/Q) that

results from a percentage change in price (∆ P/P).

In a constant-cost industry, the long-run supply curve is horizontal, and the long-run supply elasticity is infinitely large. (A small increase in price will induce an extremely large increase in output.) In an increasing-cost industry, however, the long-run supply elasticity will be positive but finite.

Because industries can adjust and expand in the long run, we would generally expect long-run elasticities of supply to be larger than short-run elasticities.

The magnitude of the elasticity will depend on the extent to which input costs increase as the market expands. For example, an industry that depends on inputs that are widely available will have a more elastic long-run supply than will an industry that uses inputs in short supply.