¡Descarga Topic 4 CAPM Summary y más Apuntes en PDF de Administración de Empresas solo en Docsity!

Department of Business FINANCE I (102329) – Group 3 – 2012 - 13 Study Guide. Dr. Maria-Antonia Tarrazon & Dr. Joan Montllor

TOPIC 4. CAPITAL MARKET THEORY: THE CAPITAL ASSET PRICING MODEL

Summary

1. From the portfolio selection theory (or Markowitz’s model) and the separation theorem to the Capital Asset Pricing Model (CAPM)

Aim: The CAPM tries to explain the properties of a capital market in equilibrium.

Remember: In equilibrium means that price = value, or, in other words, that the expected rate of return = the required rate of return.

Previous hypothesis (H) and results (R):

- Investors choose their portfolio following Markowitz’s model (risk aversion + optimization of the return-risk relationship) (H)

- Investors can lend and borrow at the same interest rate, i.e. at the risk-free interest rate rf (H)

- The separation theorem holds (R) As a consequence of 1+2+3, there is only one efficient risky portfolio: P*.

The capital market:

H 1 : The portfolio selection model holds (in other words, 1+2+3 hold) H 2 : Homogeneous expectations or beliefs for all investors (new hypothesis) That investors have homogeneous expectations or beliefs means that they all analyze financial assets (i.e., stocks and the risk-free asset) in the same way and share the same view of the financial market and the same beliefs on the future evolution of asset prices. This means

that they all agree on rf and on E(Rj) , j and j,j’ for all stocks available within the financial

market^1. As a consequence of H 1 and H 2 , the optimal risky portfolio P* – valid for one investor – becomes the market portfolio M – valid for all investors operating in the capital market: P* M Properties of the market portfolio M :

- The market portfolio M is an optimally diversified risky portfolio that includes all risky assets (stocks) available in the capital market, each of them participating with the weight ( xj* ) that enables this optimal composition. Notice that this theoretical portfolio is different from its proxy in the real world, the market index or stock index, since the latter is designed with a selection of stocks chosen and weighted in such a way that the resulting portfolio is really representative for the whole stock exchange (see Topic 2).

As a consequence of H 1 + H 2 + the properties of M , the linear efficient frontier with lending and borrowing of Markowitz’s model becomes the CAPITAL MARKET LINE in the CAPM.

(^1) Notice that although this cannot be literally true, this assumption is a useful simplification in a context

(financial markets) where investors have access to similar sources of information.

Department of Business FINANCE I (102329) – Group 3 – 2012 - 13 Study Guide. Dr. Maria-Antonia Tarrazon & Dr. Joan Montllor

2. The CAPM: Hypothesis of the model

The CAPM is model that we owe to William SHARPE (1964) 2 , John LINTNER (1965)^3 and Jan MOSSIN (1966)^4. In 1990 professor Sharpe was awarded, jointly with professors Markowitz and Miller, the Nobel Prize in Economics.

In the CAPM individuals are as alike as possible, with two remarkable exceptions: their initial wealth and their risk tolerance (being all of them risk averse, some show less risk aversion than others).

The simplifying assumptions that lead to the basic version of the CAPM could be summarized as follows^5 :

- In the market there are many investors. Each of them owns an initial wealth which is small compared to the total endowment of all inverstors. Investors act as price-takers (which is the usual perfect competition assumption of microeconomics).

- The CAPM is a single-period model. If investors plan for only one period, their behaviour could be considered short-sighted or myopic, and myopic behaviour is, in general, suboptimal. Besides, a single-period model does not allow to refer to the term structure of interest rates (for the risk-free interest rate).

- Only investments in publicly traded financial assets are considered.

- Investors can lend and borrow any amount of money at a fixed rate, the risk-free interest rate.

- Investors pay no taxes on returns and no transaction costs (commissions and services charges) on trades in securities.

- Investors behave rationally and follow a mean-variance optimization criterion according to Markowitz’s model.

- Investors share homogeneous expectations or beliefs.

(^2) SHARPE, William F. “Capital asset prices: A theory of market equilibrium under conditions of risk”. Journal of

Finance. Vol. 19, num.3 (1964): 425-442. (^3) LINTNER, John. “The valuation of risk assets and the selection of risky investments in stock portfolios and

capital budgets”. Review of Economics and Statistics .Vol.47, num.1 (1965): 13-37. (^4) MOSSIN, Jan.“Equilibrium in a capital asset market”. Econometrica .Vol.34,num.4 (1966):261-297.

A fourth author, Jack TREYNOR, made also a contribution through an unpublished manuscript, “Toward a theory of the market value of risky assets”, in 1961. (^5) See, for example, BODIE, KANE and MARCUS, 5th (^) edition, subchapter 9.2.

Department of Business FINANCE I (102329) – Group 3 – 2012 - 13 Study Guide. Dr. Maria-Antonia Tarrazon & Dr. Joan Montllor

4. The Security Market Line (SML) (SECOND main result of the CAPM)

The SML expresses the required rate of return on stock j so that this stock becomes part of M. In other words, the SML expresses the required rate of return in a context of good diversification where the risk premium is a function of the level of systematic risk or coefficient beta:

Rrequired j = E(Rj) = rf + E(RM) – rf ]·j ( 2 )

That is to say:

Required (=expected in CAPM) return = risk-free interest rate + risk premium

Or, expressing all the components of equation (2):

Required return on stock j (= expected return in the CAPM since model in equilibrium)

Risk-free interest rate

Price of risk in the capital market (difference between expected return on the market porfolio and rf )

x Beta of stock j (or level of systematic risk of stock j )

Coefficient beta is the level of systematic risk and it is defined as:

2 M

j M jM 2 M

jM 2 M

j M j (^) σ

σ·σ ·ρ σ

σ σ

cov(R~,R~ ) β ( 3 )

where cov(R ~j,R~M) is the covariance between the return on stock j and the return on the market

portfolio M , and σ^2 M is the variance of the market portfolio. The covariance between stock j and M

depends on the volatility of each of these assets, j and M , and the correlation coefficient between

both, jM.

If a security has a coefficient beta higher than 1, this security is called an “aggressive” security, while if its coefficient beta is less than 1 (whether positive or negative, depending on the correlation

coefficient jM ) the security is called “defensive”. The reason for these two adjectives lays on the

relationship between the security j and the market portfolio M. If the security is “aggressive” it reacts to changes (whether positive or negative) more intensively than M, while if the security is “defensive” its return increases or decreases less intensively than the market return.

For drawings of the SML, see, for example:

- Bodie/Kane/Marcus, 5th^ edition, Figures 9.5, 9.

- Brealey/Myers, 7th^ edition, Figures 8.7, 8.

- Ross/Westerfield/Jaffe, 7th^ edition, Figure 10.11 (and also 11.3, 11.4).

For drawings of coefficient beta, see, for example:

- Bodie/Kane/Marcus, 5th^ edition, Figure 10.

- Brealey/Myers, 7th^ edition, Figure 9.

- Ross/Westerfield/Jaffe, 7th^ edition, Figure 10.10, 11.1, 12.3.

Department of Business FINANCE I (102329) – Group 3 – 2012 - 13 Study Guide. Dr. Maria-Antonia Tarrazon & Dr. Joan Montllor

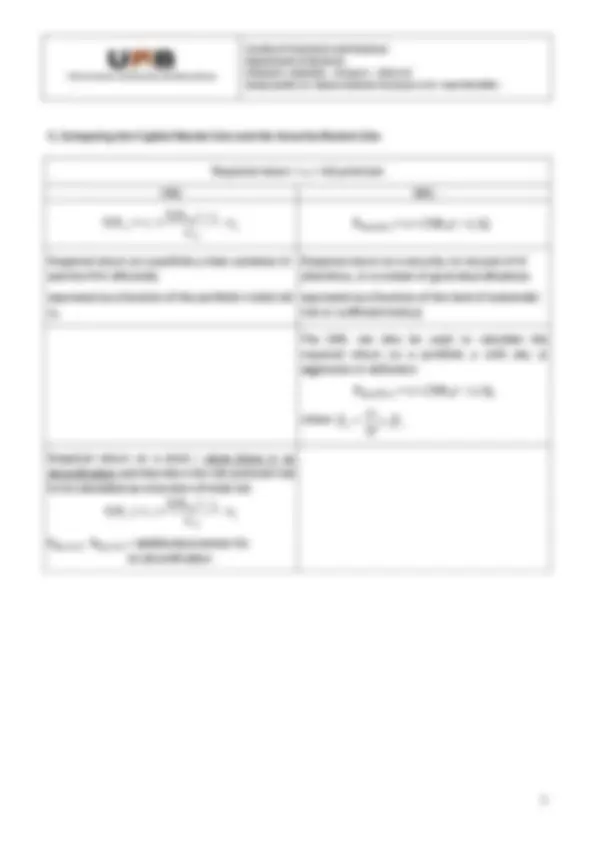

5. Comparing the Capital Market Line and the Security Market Line

Required return = rf + risk premium CML SML

p M

p f M f σ σ

E(R )r E(R )^ r Rrequired j = rf + E(RM) – rf ]·j

Required return on a portfolio p that combines M and the RFA efficiently

expressed as a function of the portfolio’s total risk

p

Required return on a security j to be part of M (therefore, in a context of good diversification) expressed as a function of the level of systematic

risk or coefficient beta j

The SML can also be used to calculate the

required return on a portfolio p with any ,

aggressive or defensive: Rrequired p = rf + E(RM) – rf ]·p

where

n

j 1

βp xj·βj

Required return on a stock j when there is no diversification and therefore the risk premium has to be calculated as a function of total risk:

j M

M f j f σ σ

E(R ) r E(R ) r

Rreq CML - Rreq SML = additional premium for no diversification

Department of Business FINANCE I (102329) – Group 3 – 2012 - 13 Study Guide. Dr. Maria-Antonia Tarrazon & Dr. Joan Montllor

7. Applications of the CAPM to financial management

Extrapolation of the SML to real investment analysis: company and project costs of capital

Up to here we have seen the SML in the context of a financial market in equilibrium. If we extrapolate now this result to the analysis of real assets (e.g.: a firm’s investment project), the SML helps to emphasize a key concept in financial management:

Key concept: The expected rate of return on any investment project (Eproject) has to be compared always with its cost of capital or required rate of return on that investment project (Rreq.project), never with the company cost of capital (Rreq.firm) which depends on the average beta of the firm’s assets (or projects).

This point is very important since firms often speak of a corporate discount rate (or any of its possible synonymous: firm’s overall or average cost of capital , hurdle rate , cutoff rate , or benchmark , all of them Rreq.firm). Unless all projects in the company are of the same risk, choosing the same discount rate or required rate of return for all of them is a mistake that can easily lead to incorrect acceptance or rejection of projects. The comparison between the company cost of capital rule and the required return according to the SML clearly establishes these two areas of wrong decisions.

For drawings, see, for example:

- Brealey/Myers, 7th^ edition, Figure 9.

- Ross/Westerfield/Jaffe, 7th^ edition, Figure 12.

Departing from the project’s initial investment (a 0 ) and comparing its expected return (Eproject) with its cost of capital (Rreq.project) we can calculate the project’s net present value (NPV) as (see Topic 1):

NPVproject = 0 req.project

0 project a R

a ·E ( 10 )

Then, if: RIGHT COMPARISON RIGHT ANALYSIS Eproject > Rreq.project NPV > 0 ACCEPTANCE Eproject = Rreq.project NPV = 0 indifference Eproject < Rreq.project NPV < 0 REJECTION if no further analysis through real options is needed

BIG ERROR: WRONG COMPARISON WRONG ANALYSIS: DANGER Eproject > Rreq.firm NPV > 0 Wrong acceptance if Rreq.project > Eproject > Rreq.firm Eproject = Rreq.firm NPV = 0 Wrong indifference since Rreq.project > Rreq.firm REJECTION Rreq.project < Rreq.firm ACCEPTANCE Eproject < Rreq.firm NPV < 0 Wrong rejection if Rreq.project < Eproject < Rreq.firm