Consolidated accounts, Lesson 1 1

CONSOLIDATED ACCOUNTS

Lesson 1

Jose López Gracia

[email protected], 4D08

Department of Accounting

University of Valencia

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Prepara tus exámenes

Prepara tus exámenes y mejora tus resultados gracias a la gran cantidad de recursos disponibles en Docsity

Prepara tus exámenes con los documentos que comparten otros estudiantes como tú en Docsity

Encuentra los documentos específicos para los exámenes de tu universidad

Estudia con lecciones y exámenes resueltos basados en los programas académicos de las mejores universidades

Responde a preguntas de exámenes reales y pon a prueba tu preparación

Consigue puntos base para descargar

Gana puntos ayudando a otros estudiantes o consíguelos activando un Plan Premium

Comunidad

Pide ayuda a la comunidad y resuelve tus dudas de estudio

Ebooks gratuitos

Descarga nuestras guías gratuitas sobre técnicas de estudio, métodos para controlar la ansiedad y consejos para la tesis preparadas por los tutores de Docsity

Asignatura: Consolidació comptable, Profesor: Carlos Vidal, Carrera: Administració i Direcció d'Empreses, Universidad: UV

Tipo: Apuntes

1 / 12

Esta página no es visible en la vista previa

¡No te pierdas las partes importantes!

Consolidated accounts, Lesson 1

Jose López Gracia [email protected], 4D08Department of AccountingUniversity of Valencia

Consolidated accounts, Lesson 1

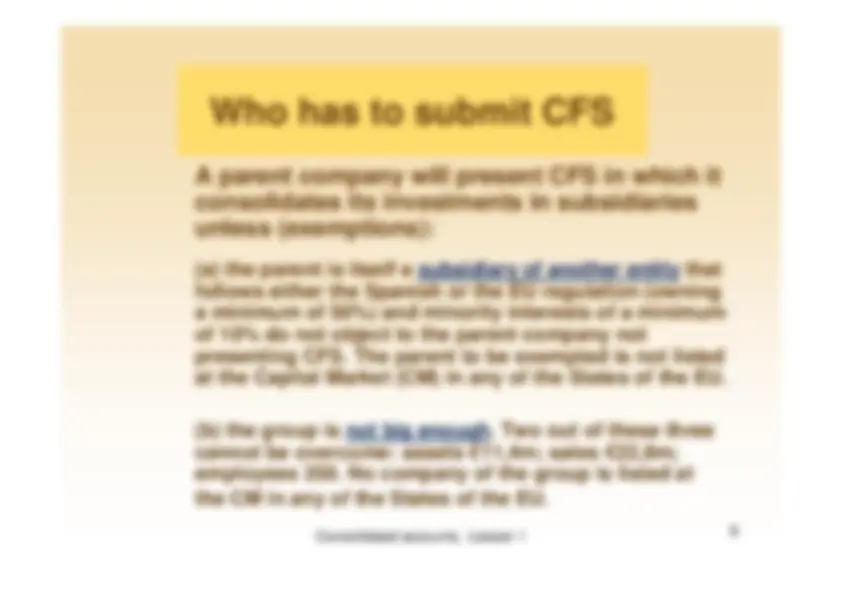

When do consolidated financialstatements (CFS) have to be

prepared?

Consolidated accounts, Lesson 1

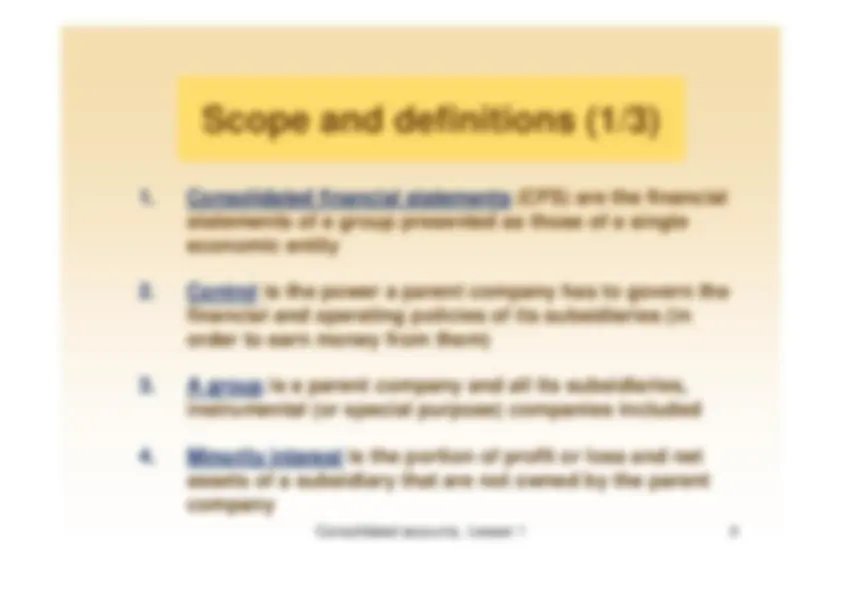

Consolidated financial statements (CFS) are the financialstatements of a group presented as those of a singleeconomic entity

2.^

Control is the power a parent company has to govern thefinancial and operating policies of its subsidiaries (inorder to earn money from them)

3.^

A group is a parent company and all its subsidiaries,instrumental (or special purpose) companies included

4.^

Scope and definitions (1/3)Minority interest is the portion of profit or loss and netassets of a subsidiary that are not owned by the parentcompany

Consolidated accounts, Lesson 1

1.^

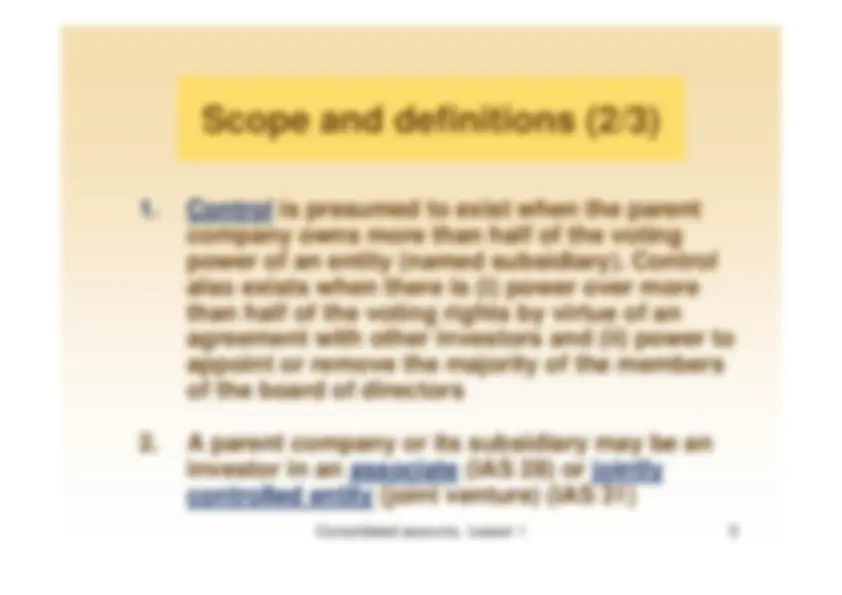

Control is presumed to exist when the parentcompany owns more than half of the votingpower of an entity (named subsidiary). Controlalso exists when there is (i) power over morethan half of the voting rights by virtue of anagreement with other investors and (ii) power toappoint or remove the majority of the membersof the board of directors

2.^

Scope and definitions (2/3)A parent company or its subsidiary may be aninvestor in an associate (IAS 28) or jointlycontrolled entity (joint venture) (IAS 31)

Consolidated accounts, Lesson 1

1.^

DirectExample: Company A has 70% of B

2.^

IndirectEx.: A has 80% of B and B has 60% of C

3.^

TriangularEx.: A has 60% of B and 30% of C and B has 25% of C

Types of relationship

Consolidated accounts, Lesson 1

^

Face share is the direct share an entity ownsin the investee’s equity ^

Effective share is the result of multiplying twoor more face shares in an indirect relationship ^

Face, effective and controlControl share is the face share correspondingto the last link in a control chain

share (or percentage)

Consolidated accounts, Lesson 1

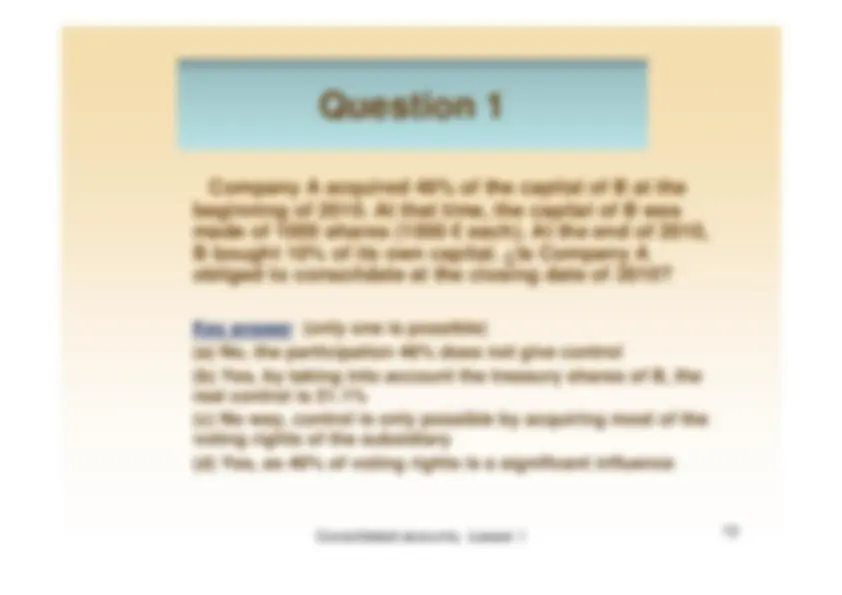

Company A acquired 46% of the capital of B at thebeginning of 2010. At that time, the capital of B wasmade of 1000 shares (1000 € each). At the end of 2010,B bought 10% of its own capital. ¿Is Company Aobliged to consolidate at the closing date of 2010?Key answer (only one is possible)(a) No, the participation 46% does not give control(b) Yes, by taking into account the treasury shares of B, thereal control is 51.1%(c) No way, control is only possible by acquiring most of thevoting rights of the subsidiary(d) Yes, as 46% of voting rights is a significant influence

Question 1

Consolidated accounts, Lesson 1

Company A acquired 30% of the capital of B in June2010. Furthermore, A achieved the power to name most ofthe BOD of B. At the end of 2010, B bought 20% of theshares of C´s capital. Additionally, B agreed with othershareholders of C to get the power to govern company C.C is 100% owner of D. ¿Who are the companies making upthe group to be consolidated at the closing date of 2010?Key answer (only one is possible)(a) A, B, C, D(b) A, B (Company C is an associate, D is not controlled)(c) No group (B, C and D are just associates)(d) A, B, C (D is not a subsidiary of A)

Question 2