Baixe Memory 1997 - sec02 e outras Notas de estudo em PDF para Automação, somente na Docsity!

1996 FACTS 1997 FORECAST

Market Size: $25,130 million Market Size: $21,485 million

Shipments: 2,762 million Shipments: 3,064 million

ASP: $9.10 ASP: $7.

OVERVIEW

Dynamic random access memory or DRAM is the main memory component of most computers

and many electronic systems. From 1993-1995, industry observers were stunned and amazed as

the DRAM market displayed relentless growth. Helping the DRAM market grow at its acceler-

ated pace was the lack of sufficient memory production capacity available to meet the needs of the

vigorous PC market.

In 1996, a different scenario panned out for the DRAM market and its suppliers. In 1Q96, DRAM

prices for 4Mbit devices plunged and continued to drop through the balance of the year.

Furthermore, 16Mbit DRAM average selling prices (ASPs) also rapidly declined. Softer PC sales

and a rather sudden glut of worldwide production capacity turned the DRAM market from one

of the most lucrative to one of most difficult in which to participate.

For 1997, ICE anticipates another soft year for the DRAM market. Although unit demand will

remain strong and bit volume will continue to grow nicely, excess capacity will further erode aver-

age selling prices. This will keep the market from growing at the rapid pace it experienced just a

few years ago.

THE DRAM MARKET

The DRAM market has been through many up and down cycles as shown in Figure 2-1, but few

suppliers recalled demand being so strong over such a long period of time as during the recent

past few years. For the already huge DRAM market to grow by such large percentages over a sev-

eral year period was quite remarkable.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

However, as the graph shows, good times don’t last forever. Excess capacity and plunging aver-

age selling prices resulted in a 38 percent decline in the 1996 DRAM market. Following that dis-

astrous year, there is good news and bad news.

The bad news is that ICE forecasts another double-digit decline in for the 1997 DRAM market (–

percent). Back to back double-digit declines would be a first for the DRAM market. The good

news is that recent DRAM market history shows that negative growth has lasted one or, at the

most, two years, while positive growth periods have been three or four-plus years in duration. At

the end of these growth spurts, the DRAM industry has always greatly increased in size.

Shown in Figure 2-2 is ICE’s complete DRAM market forecast for the 1992-2002 time period.

Displayed are the market size, units shipments, ASPs, and price per megabit for several densities.

The quarterly DRAM market shown in Figure 2-3 details the strong quarterly growth period in

the DRAM market. DRAM manufacturers must look back fondly upon 1994 and 1995 when

everything was up, up, up! There was no end in sight to the outstanding growth—until 1Q96. As

noted in the chart, average selling prices fell steeply and fell quickly.

2-2^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Dollars (MIllions) Percent Change

Year

Source: ICE, "Memory 1997" 20870D

Total Market ($M) Percent Change

Upward Growth Period

Average Length

Size of Market at End of Cycle 1978- 1982- 1986- 1992-

3 Years 3 Years 4 Years 4 Years

4.4X

5.91X

5.65X

6.18X

4.4X 5.91X 5.65X 6.18X

(FCST)

Figure 2-1. DRAM Market History

It appears the overall DRAM market stabilized in the latter half of 1996 and into 1Q97. While the

market did stabilize, ICE forecasts further erosion of the market in 1997, but at a much more

gradual pace.

The total DRAM market for the period 1992-2002 is shown in Figure 2-4. Following four years of

outstanding growth, the long-anticipated “recovery” in the market hit in 1996. ICE forecasts that

it will take the DRAM market a few more years (to the year 2000) to be at least the size it was in

1995. From 1997 to the year 2002, ICE forecasts the DRAM market to have a cumulative average

annual growth rate of 31 percent.

Excess capacity will remain a fact of life for the DRAM suppliers in 1997. The potential for price

wars will continue as companies seek to grow or maintain their share of the market. As the decade

closes, however, ICE believes DRAM supply and demand will be better balanced. Early into the

2000’s, ICE forecasts that demand will once again outstrip supply, causing the market to grow at

an accelerated pace.

2-4^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Dollars

Units

ASP

Millions of Units, Dollars

ASP ($)

Source: ICE, "Memory 1997" 20881A

1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96 2Q963Q96 4Q96 1Q

Market ($M) Units (M) ASP ($)

Quarter/Year

Figure 2-3. Quarterly DRAM Market

Displayed in Figure 2-5 is the DRAM market by density. In terms of dollar volume, the 16Mbit

density was the largest in 1996 and is forecast to remain the biggest market in 1997 and 1998.

However, ICE believes that market demand for the 64Mbit generation will develop in 1997 and

grow rapidly to challenge the 16Mbit market beginning in 1998. Meanwhile, the 4Mbit density is

forecast to quietly slip closer to the obsolete phase in the product lifecycle—a distant “memory”

of a grand time in the DRAM market.

DRAM UNIT SHIPMENTS

Shown in Figure 2-6 are quarterly DRAM shipments beginning in 1994 and continuing through

1Q97. During the 13-quarter span, total DRAM shipments increased 89 percent. 4Mbit devices,

which accounted for 61 percent of total shipments in 1Q94, represented 36 percent of shipments

in 1Q97. Meanwhile, shipments of DRAMs with densities greater than 4Mbit grew rapidly in

the last three quarters shown. In 1Q97, these devices accounted for 57 percent of total DRAM

unit shipments.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

Dollars (Millions) Percent Change

Year

Source: ICE, "Memory 1997" 18857E

Total Market ($M)

Percent Change

Total Market

Percent Change

Figure 2-4. DRAM Market Growth

With low pricing, designers employed these devices in great numbers in their systems.

Consumers, who long awaited to upgrade the memory in their PCs also took advantage of the

tremendously lower prices for 4Mbit DRAMs. As a result, unit shipments at this density remained

well over one billion pieces during 1996.

A big jump in 16Mbit shipments is forecast for 1997. Nearly all the major Japanese and Korean

vendors ramped their output of this density to supply the world’s needs.

Figure 2-9 provides a look at the typical lifecycle curve for DRAM unit shipments. The 1Mbit den-

sity took a long, slow decline on its way out of the market spotlight after peaking in 1991. 4Mbit

shipments peaked in 1995, more than doubling the highest yearly 1Mbit output. Perhaps more

than any other generation to date, 4Mbit DRAMs enjoyed more time in the “spotlight,” which is

the mature/saturation phase of the product lifecyle.

16Mbit devices ramped up in 1996 and will be followed by the 64Mbit generation in 1997/1998.

ICE forecasts that shipments of 16Mbit DRAMs will peak in 1998 and that 64Mbit devices will top

out early in the next century. Whether by a few hundred million or several hundred million units,

each successive DRAM generation ships more than its predecessor.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

1Q94 2Q94 3Q94 4Q94 1Q95 2Q95 3Q95 4Q95 1Q96 2Q96 3Q96 4Q96 1Q

Quarter/Year

≤256Kbit

1Mbit

4Mbit

≥4Mbit

Total Units (M)

Units (Millions)

Source: ICE, "Memory 1997" 20885A

Figure 2-6. Quarterly DRAM Shipments by Density

Unit Shipments by Architecture

Until recently, all DRAMs were made using the same fast-page mode (FPM) architecture.

However, FPM devices can no longer keep pace with faster microprocessors, and, consequently,

hamper overall system performance.

As a result of FPM DRAM’s inability to keep pace with high-speed microprocessors, and since

almost three-fourths of all DRAMs wind up in PC systems with high-speed microprocessors,

DRAM architectures have changed. Though there are numerous revolutionary and evolutionary

alternatives (reviewed in Section 7), three main architectures emerged that appear likely to con-

tend for the largest share of 1997 and 1998 DRAM shipments. Figure 2-10 shows the three—

extended data out (EDO) DRAM, synchronous DRAM (SDRAM), and Rambus DRAM—and how

ICE believes the market will be divided among these different architectures in the coming years.

2-8^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Total Units (M)

Percent Change

Year

Units (Millions) Percent Change

Source: ICE, "Memory 1997" 20006C

Total Units (M)

Percent Change

Figure 2-7. DRAM Unit Shipments

2-10^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Year

Total Units (Millions)

Source: ICE, "Memory 1997" 20887B

1Gbit 512Mbit 256Mbit 128Mbit 64Mbit 16Mbit 4Mbit 1Mbit 256Kbit 64Kbit

Figure 2-9. DRAM Unit Shipments by Density

Figure 2-10. DRAM Shipments by Architecture (Percent)

Fast Page Mode EDO Synchronous Rambus and Other

Percent

Year

Source: ICE, "Memory 1997" 20888C

The transition from EDO to SDRAMs may be a bumpy one for suppliers and buyers alike. For

suppliers, the process of converting today’s DRAM fabs to manufacture SDRAMs has been some-

what difficult, which may delay the supply of parts just as demand is heating up. Meanwhile,

some memory IC buyers indicated that initial qualification of an SDRAM vendor was difficult,

apparently since SDRAM specifications varied from vendor to vendor. These are problems that

will undoubtedly be resolved with time, but which initially made for a less-than-ideal transition

to SDRAMs.

Toshiba’s schedule to increase SDRAM production is shown in Figure 2-11. The company, in

2Q97, introduced a 64Mbit synchronous DRAM family that featured three organizations and

speeds to 125MHz. The Hitachi DRAM product roadmap is displayed in Figure 2-12. Hitachi will

ship 50 percent of its DRAMs in the form of synchronous DRAMs by the end of 1997. Both Fujitsu

and NEC expect that 70 percent of all their DRAMs will be synchronous by the close of the fiscal

year (ending March 31, 1998).

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

Rambus

Synchronous

20% EDO

Source: ICE, "Memory 1997" 20889

Rambus

Synchronous

EDO

Figure 2-11. Toshiba’s DRAM Shipments by Architecture

Figure 2-12. Hitachi’s Main Memory Solutions Shift to SDRAM

Year

Percent

Source: Hitachi/ICE, "Memory 1997" 20920

Fast Page – 70ns

EDO – 60ns SDRAM

Beyond SDRAMs, Samsung is promoting double data rate (DDR) SDRAM, which doubles the

transfer rate of information compared to a standard SDRAM (which transfers almost twice as much

data as an EDO DRAM device, Figure 2-15). Samsung believes the DDR SDRAM technology will

extend the life of synchronous memory into the 300MHz range, thus directly competing with the

Rambus DRAM and perhaps delaying the day when vendors have to embrace a new architecture.

In 1996, it became obvious that standard SDRAMs would not be able to perform to the 1.5Gbit to

3.0Gbit/second system bandwidth necessary to provide realistic 3D graphics and DVD process-

ing. The Rambus DRAM (RDRAM) provides that solution. This technology provides a wide path

for fast data transfer between the memory and the processing segments of a system.

Rambus licensed the top five DRAM manufacturers (and several others) to use its technology. The

company charges a flat “engineering fee” to customize its interface to a memory vendor’s exist-

ing product. Vendors then pay royalties based upon the actual selling price of the Rambus DRAM.

Rambus scored a major win when it announced in 1Q97 that Intel would adopt the Rambus

DRAM architecture as its next-generation main-memory technology for PCs. If all goes according

to Intel’s plan, Rambus DRAMs will begin to appear in high-end PCs in 1999 (Figure 2-16).

DRAM AVERAGE SELLING PRICES

The DRAM average selling price (ASP) from 1992 through 2002 is shown in Figure 2-17. Limited

production capacity and strong demand kept ASPs rising quickly during the first part of the

decade. To the contrary, added worldwide production capacity (i.e., greater supply) led to a crash

in the DRAM ASP in 1996. ICE forecasts that an overcapacity condition will continue through

1997, which will lead to further erosion of average selling prices. Demand should begin to match

supply in 1998 and then gradually out-grow supply through the year 2002. Accordingly, DRAM

ASPs are forecast to climb during this time.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

Source: Samsung/ICE, "Memory 1997" 22679

Bus Clock Speed (MHz)

Fast Page

(300Mbits/s)

EDO

(500Mbits/s)

SDRAM

(>500-800Mbits/s)

DDR SDRAM II

(1.0-2.4Gbits/s)

Figure 2-15. Samsung Promotes DDR SDRAM to Match Bus Clock

2-14^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

�����

�����

�����

�����

�����

�����

�����

����

����

����

����

����

High End

Desktop

Volume

Desktop

Low Cost

Desktop

FP EDO^

66MHz

SDRAM

100MHz

SDRAM

Direct

RDRAM

Source: Intel/Rambus/ICE, "Memory 1997" 22680

Figure 2-16. Intel’s Outlook for PC Platform Memory

Figure 2-17. DRAM Average Selling Price

Year

Source: ICE, "Memory 1997" 20022D

Total ASP ($)

Percent Change

ASP ($)

Percent Change

Total ASP (S)

Percent Change

2-16^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Dollars

Nov '95 Dec '95 1Q96 2Q96 3Q96 4Q96 1Q

High

Low

Average

Source: ICE, "Memory 1997" 20895A

Average Price

Figure 2-19. 4Mbit DRAM Price Trends

Dollars

Nov '95 Dec '95 1Q96 2Q96 3Q96 4Q96 1Q

High

Low

Average

Source: ICE, "Memory 1997" 20896A

Average Price

Figure 2-20. 16Mbit DRAM Price Trends

64Mbit DRAM ASPs followed the same path as 4Mbit and 16Mbit generations before them. At the

beginning of 1996, 64Mbit DRAMs sold for $250. By the end of the year, they sold for $90. In

1Q97, the devices were offered for $60, and in 2Q97, the prices had dropped to less than $40. As

of 2Q97, there was more 64Mbit product than the niche application of high-performance work-

stations could absorb.

ICE believes the DRAM buyers’ market will continue throughout 1997. Plenty of fab capacity will

keep prices flat or slightly down on all densities of DRAM during the upcoming year.

DRAM BIT VOLUME

DRAM bit volume is provided in Figure 2-21. The DRAM bit volume forecast provides a clear indi-

cation that the DRAM market will remain vibrant through the year 2002. There will be demand for

more bits. Annual bit volume growth from 1997 through the year 2002 is forecast to average 69 per-

cent, with 64Mbit and 256Mbit devices serving as the backbone for that growth (Figure 2-22).

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

Bits x 10

12

Percent Change

Year

Total Bit Volume

Percent Change

Source: ICE, "Memory 1997" 20894C

Bit Volume

Percent Change

Figure 2-21. DRAM Bit Volume

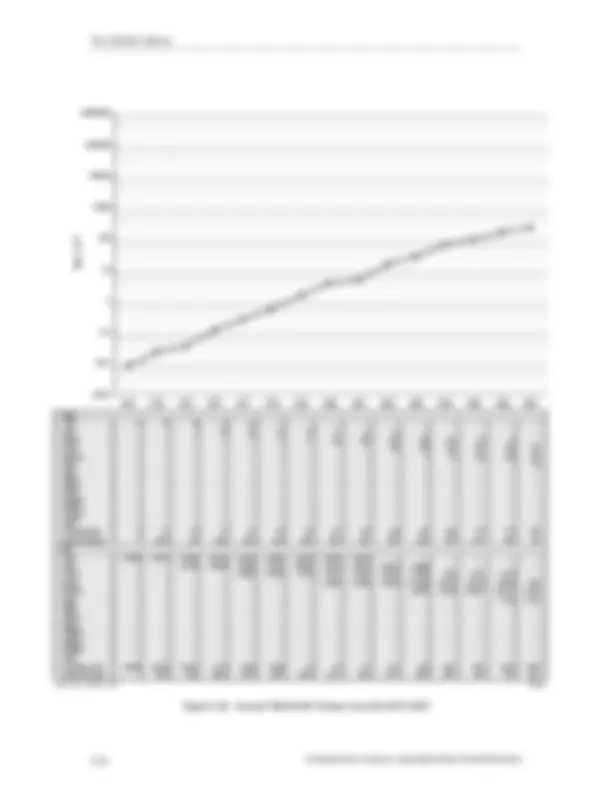

A line representing total yearly bit volume for the DRAM market dating from 1973 is shown and

plotted in Figure 2-24. With two exceptions (1975 and 1981) DRAM bit volume grew by triple-

digit digit amounts from 1973 through 1984. Double-digit increases, averaging 67 percent per

year, are shown as the norm from 1985 through the year 2002.

DRAM PRICE PER MEGABIT

DRAM price per megabit values for several densities are plotted in Figure 2-25 for the 1992-

time period. 1991 was the crossover year for the 4Mbit generation. It became the lowest-priced

device and held that distinction through 1994. In a rare case, the 1Mbit density replaced 4Mbit

devices as the low-price leader in 1995. In this case, demand, coupled with limited capacity, for

4Mbit devices kept the ASP (and price per megabit value) high, while that of 1Mbit devices con-

tinued to move downward.

The price per megabit of 4Mbit and 16Mbit devices dropped significantly in 1996. In fact, the

16Mbit generation became the new cost-effective DRAM during the year. ICE expects the 16Mbit

and 64Mbit DRAMs to have equal price per megabit values in 1998, with the 4X cross-over point

occurring in mid-1998. Then, in 1999, the 64Mbit generation is forecast to take over as the price

per megabit leader.

INTEGRATED CIRCUIT ENGINEERING CORPORATION 2-

Year

PC Growth (Percent)

DRAM Content (Mbytes)

PC Growth

DRAM Content

Source: Texas Instruments/ICE, "Memory 1997" 22682

Figure 2-23. DRAM Content Growing Rapidly

2-20^ INTEGRATED CIRCUIT ENGINEERING CORPORATION

Source: ICE, "Memory 1997" 20898A

Bits x 10

12

8 — — — — — — — — — — — — 8 —

— — — — — — — — — — — —

—

21 — — — — — — — — — — — —

21 163%

— — — — — — — — — — — —

163%

19 3 — — — — — — — — — — —

22 5%

— — — — — — — — — — —

48%

13 24 — — — — — — — — — — —

37 68%

— — — — — — — — — — —

252%

10 50 2 — — — — — — — — — —

62 68%

— — — — — — — — — —

122%

5 67 17 — — — — — — — — — —

89 44%

— — — — — — — — — —

125%

1 70 71 — — — — — — — — — —

142 60%

— — — — — — — — — —

160%

1 31 184 1 — — — — — — — — —

217 53%

— — — — — — — — —

121%

1 15 230 11 — — — — — — — — —

257 18%

— — — — — — — — —

42%

— 10 240 100 — — — — — — — — —

350 36% —

— — — — — — — — —

131%

— 5 220 330 2 — — — — — — — —

557 59% —

— — — — — — — —

145%

— — 120 820 40 — — — — — — — —

980 76% — —

— — — — — — — —

157%

— — 35 500 240 — — — — — — — —

775 -21% — —

— — — — — — — —

45%

— — 10 380 520 4 — — — — — — —

914 18% — —

— — — — — — —

72%

— — — 150 680 45 — — — — — — —

875 -4% — — —

— — — — — — —

42%

Units 1Kbit 4Kbit 16Kbit 64Kbit 256Kbit 1Mbit 4Mbit 16Mbit 64Mbit 128Mbit 256Mbit 512Mbit 1Gbit Total Units (M) Percent Change Bits 1Kbit 4Kbit 16Kbit 64Kbit 256Kbit 1Mbit 4Mbit 16Mbit 64Mbit 128Mbit 256Mbit 512Mbit 1Gbit Total Bits (10^12 ) Percent Change

Figure 2-24. Annual DRAM Bit Volume Growth (1973-1987)